Three Things I Regret About My Portfolio

I often find that many investors sound like a bunch of guys coming back from a fishing trip. When you ask them if fishing was good, they only remember their best catch. They will discuss this single catch with as many details as possible, they will tell you how good they were and how they knew it was going to happen this way. If they don’t catch a big one, they will quickly summarize their trip finding some kind of excuse why it didn’t work out.

When you discuss investing with people around you, they will most likely tell you about their best trade and forget about the rest. However, we rarely learn from our best moves in life, we usually learn from our mistakes. This is why I think it’s important to look back at our past moves and look at what went wrong to make sure it doesn’t happen again. I’ve highlighted three things I regret about my portfolio today.

#1 Having chased returns for too long

When I started investing, I was young and thought of making money, lots of money with my investments. I didn’t realize it takes years to make real money and that I’m not the next Warren Buffett. This is how I wasted a good seven years chasing returns before building a real investing process based on a serious strategy.

Interesting enough, I’ve made more money during those 7 years than I’m making now with my dividend growth strategy. Several reasons explain this:

- I started investing at a perfect moment (my first 3 years were 2003 to 2006);

- I withdrew most of my money to buy a house in 2007, therefore I didn’t lose much in dollars in 2008;

- I used to spend about 2 hours per day on my portfolio to be successful.

However, if I had started a dividend growth portfolio back in 2003, I would be generating more than double what I do now in dividend payments. Those are great years I didn’t use to benefit from the power of compounding interest rates.

#2 Ignoring boring stocks at first sight

When I first started investing in dividend stocks, I systematically ignored any company with yield under 2.5%. In fact, I was even reluctant to pick companies with a yield under 3%. The only exceptions I made back then was Coca-Cola (KO) and Chevron (CVX) which were paying something around 2.75%. I thought I needed strong yield at first (3%+) to build a dividend portfolio. I also thought that low dividend yielding stocks would take forever to pay something that was worth considering. I was terribly wrong.

I’ve made a case about how low dividend yield stocks outperform high yielding stocks.

I first bought a company yielding under 2% when I considered Apple (AAPL) as I was seduced by its amazing growth potential. At that time, the stock was trading low (under $400 before the split) and AAPL just started paying a dividend not too long ago. I thought that worse comes to worse, AAPL would become another Microsoft (MSFT); a techno giant full of cash finally distributing its unused wealth with shareholders. It turned out to be a better investment while the stock price almost doubled and the dividend payout is strongly increasing each year.

After this “success”, I bought other companies with lower yields such as Disney (DIS), Canadian National Railway (CNR.TO / CNI) and 3M Co (MMM). The key is to find companies with low yield, but also a low payout ratio and a strong ability to generate strong cash flow. These companies are then able to aggressively increase their payout year after year. When the dividend increases, their stock price usually follows accordingly.

#3 Not saving enough to invest

While I would have a stronger portfolio if I had realized the first 2 things earlier in my investing life, the third thing I regret the most is also the most important. No matter what you read about investing, there are two metrics that will determine what your portfolio will look like in the future: the time invested in the market (how many years you stay invested) and the amount of capital you invest. I started investing at a very young age (23), but I didn’t save very much money so far.

A few years ago, I was able to put between $5,000 and $10,000 per year in my retirement fund. Those were the good years. Over the past 3 years, I barely saved $1,000 per year. We ran into many budgeting challenges such as a third child, a bigger house and other bad habits worsening our lifestyle inflation. I didn’t worry too much because I still have a pension fund at work and I was working hard on making more revenue.

However, if I had started saving $10,000 per year back in 2003, I would be sitting on a 6 figure portfolio on top of having a house and my pension fund. Even better, this 6 figure portfolio would only grow bigger and faster as the compounding dividend growth rate would also grow accordingly.

Once I come back from my trip, I will have to work on a whole different budget and prioritize savings. The sooner you save money; the sooner you achieve financial independence. There is no trick, no magic to reach FIRE, it’s only a matter of working hard and saving hard!

What about you, what are the things you regret the most about your portfolio?

Promising Canadian Aristocrats Companies

It is quite interesting to see how the Canadian stock market has recovered a very good part of its latest drop:

Source: ycharts

Source: ycharts

We keep reading pessimistic news, but the reality is otherwise. While the stock market plummeted by more than 20% compared to its previous peak, the “big hole” left by the oil price drop is now just a bump in the road.

To be honest, I don’t really mind if the market is up or down by 20% for the past 12 months. In fact, I rather like focusing on what is coming month after month in my cash account: dividend income.

If you are looking to start your Canadian dividend growth portfolio, you should know that there is a special list of “elite” companies that have proved to their shareholders that they will reward them on a consistent basis. As the US stock market has its aristocrat companies, so do Canadians!

Canadian do have aristocrats, but they are just not as impressive

Considering the US stock market, a company must successfully increase its dividend payout for 25 years consecutively. As it is not enough to distribute their cash flow, they must increase it year after year and show an impressive consistency.

If we would apply the same rule in Canada, I’m not even sure we would have a single company on the aristocrats list. This is why the stock market came up with another set of rules :

- The company’s security is a common stock or income trust listed on the Toronto Stock Exchange and a constituent of the S&P Canada BMI. .2. The security has increased ordinary cash dividends every year for five years, but can maintain the same dividend for a maximum of two consecutive years within that five year period.

3. The float-adjusted market capitalization of the security, at the time of the review, must be at least C$ 300 million.

4. For index additions, the company must have increased dividend in the first year of the prior five years of review for dividend growth. This rule does not apply for current index constituents.

Without being the model of constant dividend increases as we have in the States, these rules help determine the most dividend friendly stocks in the Canadian market. I’ve handpicked a list of my favorite companies from this list (note, I’ve left the Canadian Banks off of the list, you all know them anyway  ).

).

Those companies were picked based on the 7 principles of dividend growth investing.

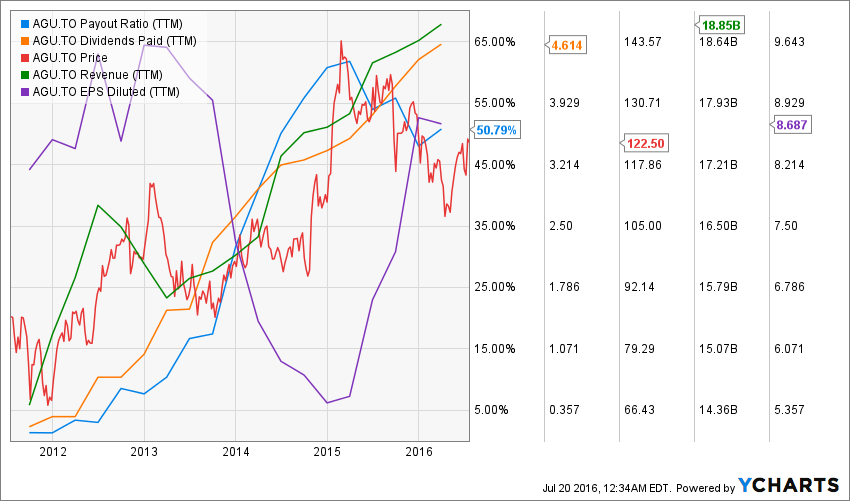

Agrium (AGU.TO)

Source: ycharts

Source: ycharts

The company’s business model is not solely limited to potash production. While being the third largest potash producer in North America, Agrium is also the largest agricultural retail operator in the USA with more than 750 farm stores across the country. In addition to potash, the company sells other fertilizers such as nitrogen and offers farms a wide variety of solutions to improve their crops (chemicals, seeds plus weather, soil and pest information).

Agrium also benefits from a highly fragmented market to make acquisitions and grow from both internal and external sources. Agrium continues to increase its dividend payout since 2012. In fact, I guess management decided to start paying dividends back in 2012 to keep investors interested in their stocks as the market for potash was collapsing. While the company’s cash payout ratio is over 100%, AGU is posting solid earnings and the fact that Uralkali & Belaruskali have made amends is helping to restore the potash oligopoly market. This should eventually help AGU’s cash flow.

BCE (BCE.TO)

Source: ycharts

Source: ycharts

BCE is part of the ever high yield payers in the Canadian dividend landscape. As opposed to REITs and oil industry dividend paying stocks, BCE seems to be alone with a very low volatility profile. While the TSX went up and down over the past 18 months, BCE hasn’t touched negative return territory if you include its generous dividend (while the TSX almost hit -20% at one point).

BCE is a diversified media company that is not afraid to use its cash flow to invest in other businesses. They recently acquired Manitoba Telecom (MBT) for the sum of $3.9 billion paid in cash and stock. This goes well with BCE’s strategy of improving its presence in the wireless business in Manitoba. On the other hand, I’m not sure it’s a super deal since MBT hasn’t been a skyrocketing business over the past few years. Not to mention that BCE will most likely have to sell a part of MBT’s postpaid wireless customers to Telus in order to gain regulatory approval.

Canadian National Railway (CNR.TO)

Source: ycharts

Source: ycharts

I’ve written a lot about CNR recently as I can’t stress enough about the quality of this company. In my introduction, I wrote that industrials follow cyclical trends creating buying opportunities. I believe this is the case right now for railroads companies. The stock lost about 7% since it has reported its latest earnings. While the company deserves various businesses segments, most of them are greatly affected by a global slowdown.

However, the company continues to aggressively increase its dividend payout supported by the best operating ratio of its industry. Management has been doing an amazing job in generating higher margins than its competitors and they have decided to share their success mainly with shareholders.

An investment in CNR today is definitely for the long haul. Don’t expect the clouds to go away this year, but if you buy now, you will be enjoying a fast increasing dividend before seeing the stock price going back up once the cycle starts again.

Emera (EMA.TO)

The future looks bright for EMA as it shows several projects for the next decade. Both revenues and EPS have grown steadily over the past five years and the dividends have followed accordingly. EMA is definitely a strong utility to hold. EMA reported clockwork results on November 13th for its Q3. Earnings are up $0.04 EPS compared to last year. Management expects the TECO acquisition should boost EPS by 5% in 2017 and growing to more than 10% by the third full year of operation (2019). EMA restated its dividend growth target of 8% through 2019 and expects to keep this pace past 2019. EMA continues to be a strong holding for any Canadian dividend growth investor.

An investment in EMA is also an investment in a relatively high dividend yielding stock. At the moment, there are a few very interesting high yield (over 4%) stocks on the Canadian market. It is also a gauge of stability. While the Canadian stock market was dropping faster than the 20 inches of snow that fell on our heads last night, EMA posted a solid and steady return coming from both its dividend payment and stock value appreciation.

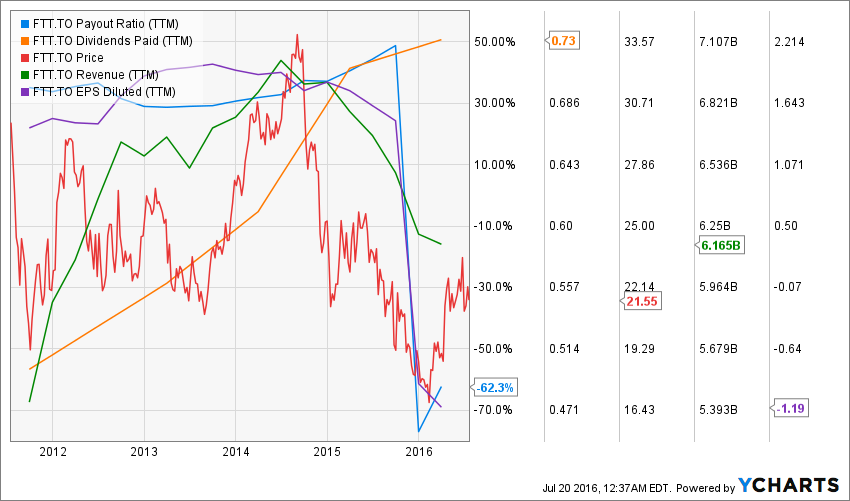

Finning International (FTT.TO)

Source: ycharts

Source: ycharts

Finning had a terrible year in 2015. Being the official Caterpillar (CAT) product reseller in Canada has its advantages as you offer a world class product to your client, but it’s another story when both the mining and the oil industry is collapsing at the same time. FTT had it rough in 2015 and provided a great buying opportunity back then. Since the beginning of the year, this is a complete new story as the stock price is already up by 22% since January.

Unfortunately, the window for buying FTT at a cheap price seems over already. The company will continue to drag behind with virtually no growth vector to work with. The mining industry is not getting any better while oil is simply “better than it was”. Think about it, can the oil industry could get any worse?

The company is strong and sells a great product, this is not the problem. However, you can sell the best car in town, if nobody needs it, it will stay in your garage.

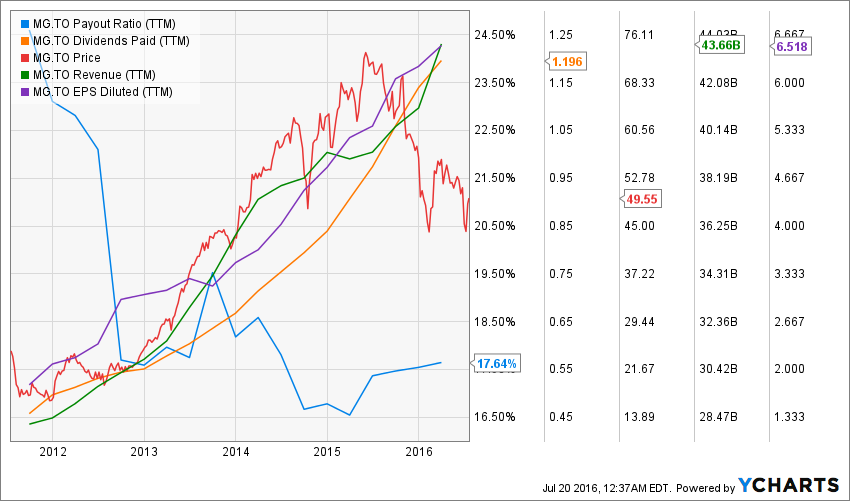

Magna International (MG.TO)

Source: ycharts

Source: ycharts

Magna is not only an international automobile part supplier, it also designs, develops, manufactures, assembles and engineers automobile parts. Magna sells to OEMs (original equipment manufacturers) across 26 countries. It offers a wide variety of 86 products that go from seating to roofing systems. MG is a leader in the auto parts industry and this serves it well as many manufacturers now tend to concentrate their processes with fewer suppliers with wider product offering. This is exactly where Magna stands in the market. While MG relies on Detroit automakers for about 50% of its sales, the overall automobile business is looking brighter in the near future. Low oil prices have helped new cars sales which leads to more sales for Magna. Finally, there is a high switching cost for automakers to change manufacturers such as Magna. This makes their niche a highly repetitive and stable market. The stock price dropped by 17% over the past 12 months and this makes MG highly interesting.

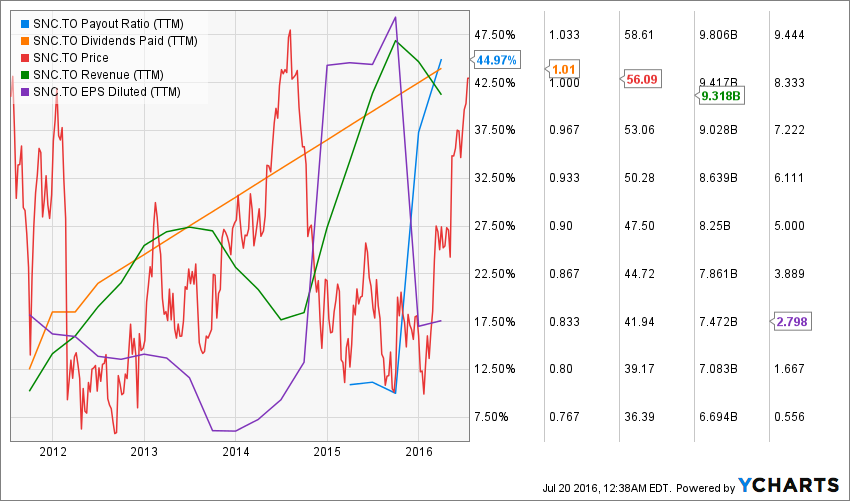

SNC Lavalin (SNC.TO)

Source: ycharts

Source: ycharts

Not too long ago, this engineering firm was treated like the ugly duckling by financial analysts. I must admit SNC looked for all the hate it received as the company is under review by the Canadian Government for corruption allegations. If the company was to be found guilty, they would be kicked-out for any Government related project for 10 years. For an engineering firm, this is possibly the greatest penalty.

However, the clouds seem to be fading away as it has become less likely there will be a trial and eventually a judgement in this case. I have a feeling there will be an out of court ruling. In the meantime, the company has restructured itself, got rid of the bad element in the company and shown some strong potential. This is how the stock price rose 30% since the beginning of the year. At the moment, many analysts now see the stock over $60 and now it is trading around $53. Better oil perspectives are also helping the company who bought important stakes in oil related businesses right before the oil crash in 2014.

Many readers were surprised when I announced this purchase back in 2014, now, this holding is over +35% in my portfolio.

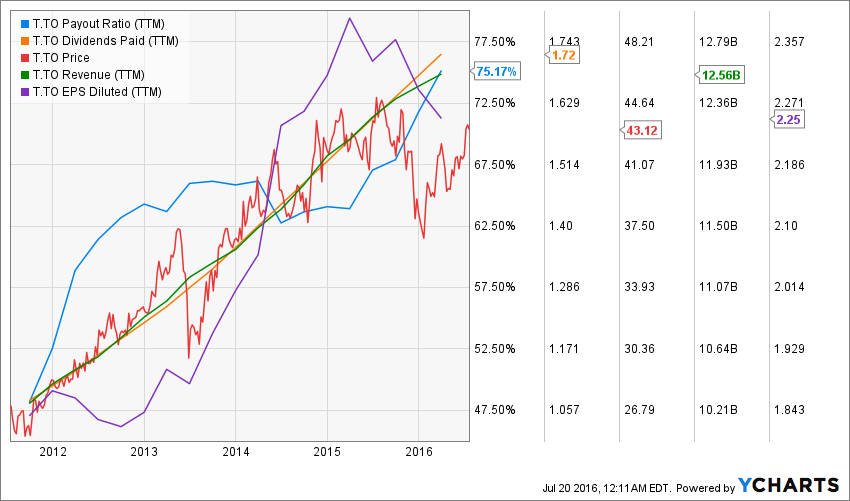

Telus (T.TO)

Source: ycharts

Source: ycharts

Telus is one of my favorite Canadian dividend paying stocks. The company is known for its solid customer service and a wide network offering. The company had announced several investments to continue improving its communication infrastructure. The bread and butter of this company comes from a solid network and great customer service. This is why they announced investments of $4.5 billion through 2019 in BC, $1 billion through 2019 in Ontario and a $500M investment to bring wireless service to highway 37A and the community of Stewart.

At the beginning of May, Telus announced another 10% dividend increase. It wasn’t a surprise, and it surely was good news. What is even better is that management expects to keep raising its payout by 7% to 10% per year from 2017 to 2019. There aren’t many companies this transparent with investors when it comes to discussing dividend distributions. While BCE and Rogers invested in Broadcasting, Telus is stealing Shaw Communications cable clients and investing in the highly profitable mobile industry

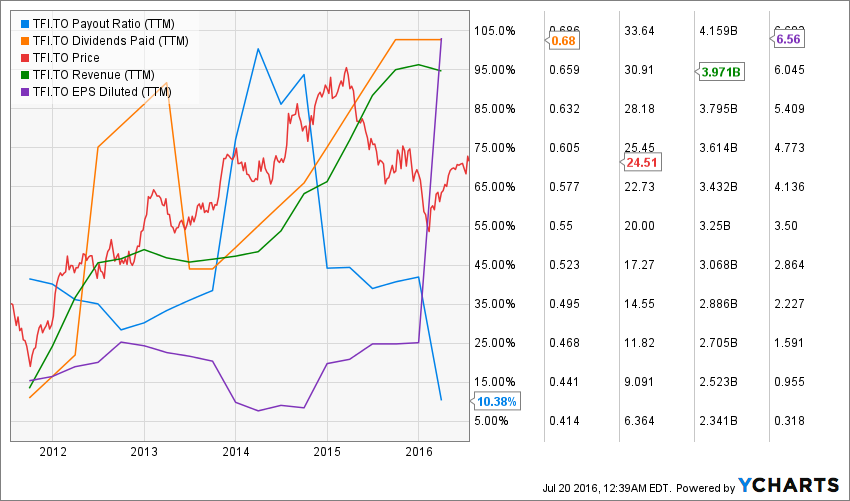

Transforce (TFI.TO)

Source: Ycharts

Source: Ycharts

Transforce is Canadian largest trucking company and the 9th largest for-hire trucking company in North America. While its stock is getting beaten down by the Street due to the weak Canadian economic outlook, TFI is generating serious cash flow and is ready to capitalize on this situation. The company’s payout ratio stands at 10.38% while its cash payout ratio is at 27.94%. These are amazing numbers that will lead to one thing; more dividend payout increases in the future.

While there are concerns around the Canadian economy, TFI benefits from a stronger market through its US division. The rise of ecommerce brought another growth vector in Canada as more and more people are ordering online that require trucks for the goods to be transported.

With lots of cash in its hand and a weaker economic outlook, many analysts anticipate a merger or acquisitions from TFI to make it even stronger when the economy bounces back. The stock is down 9% for the past 12 months and keeps dragging behind the TSX since the beginning of the year, this could represent a great buying opportunity.

There is more to the list, what is your favorite Canadian Aristocrats?

I didn’t want to pull out the whole list and this is why I stop here. I’m curious to know which dividend aristocrats you have in your portfolio?

Disclaimer: I own shares of AGU, BCE, SNC, T, CNR, FTT, EMA in my Dividend Stocks Rock Portfolios.

Why Dividend Investing is so Popular?

Have you ever wondered why investing in boring companies, offering boring returns is so successful?

Let’s face it, dividend growth investing is far from being sexy. I’m pretty sure you have encountered plenty of investors or traders offering better options. Some will trade penny stocks and transform $100 into $10,000 within a week. Some others will use technical analysis to determine when is the perfect moment to enter a new position and always get out before the market crashes. Then, you wonder why a bunch of geeks would waste precious hours to go through financial statements and look at many ratios and metrics in order to find a strong dividend paying company. This article is for those who don’t understand why we prefer boring stocks with boring returns over other strategies.

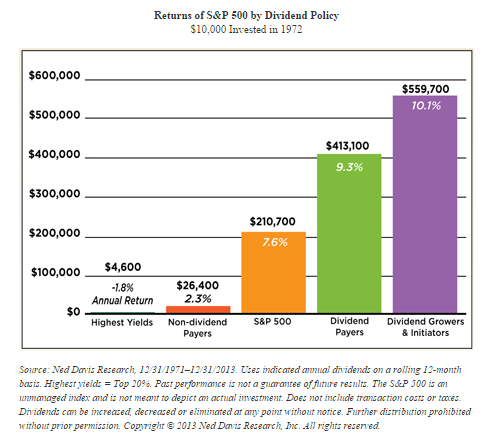

Dividend Investing Effectiveness has Been Proven Many Times

While many gurus are trying to convince you that they have found a new way to make money with investments, dividend investing tenants have proven its effectiveness many times. The strongest dividend growing stocks are also offering the best returns:

You can also look back at the past 30+ years and get the same results:

In other words; dividend growth stocks outperform the market. This is not an opinion, it’s a fact. By choosing dividend investing, you choose an investment strategy that works. The key is to select dividend growing companies and not simply dividend payers. As you can see, dividend paying stocks do well, but companies who are able to increase their payouts year after year are doing a lot better. This makes sense as a company that is able to increase its dividend payments has to be a company that increases its revenues and earnings. Then, it’s a company showing a stock going up!

Dividend Investing Doesn’t Require Some Magical Methods

What I dislike about many other investing strategies is the fact they require either a program or special methods that identify some kind of loophole in the stock market. Do you really think these methods work? I mean, there is a guy whose methods work very well and has decided to share with the world. To this day, you can still participate in his “magical way of making profits” and his name is Warren Buffett. I’m wondering if I ever crossed the name of another successful investor using a technique coming from momentum or penny stocks trading. While Warren Buffett is not solely a dividend investor, he still shows a preference for companies sharing several qualities with dividend growers.

It’s not that the other strategies don’t work. It’s just that they are often very complicated or requires you use programs and techniques based on complex calculations (that don’t always work anyways). On the opposite hand, if you have a set of simple investing rules, you can build a solid portfolio with dividend stocks.

Dividend Investing is the Only Strategy Paying You No Matter What

I guess this is similar to many dividend investors, but the thing I like the most about dividend investing is getting paid each month no matter what is happening in the market. During the first 6 months of 2016, the market was up and down, my portfolio was sometimes showing positive, sometimes negatives results, but my cash balance kept increasing month after month. I didn’t have to worry about the quality of my holdings as each company I own shares of made sure to remind me why I picked them in the first place: my companies kept increasing the payouts during the up and down times of the market. I didn’t have to do anything special to receive this income. I simply used an academically proven investing method and have stuck to it.

Dividend Investing Provides Some Astonishing Results Over Time

At the beginning of this article, I wrote that most dividend companies give the impression of being boring while delivering boring returns. This is actually a false perception. It is true that none of my holdings have come close to a skyrocketing Facebook (FB), Netflix (NFLX) or Tesla (TSLA). However, when you look over the long haul, these companies are showing amazing results. Here are a few examples of a few of my holdings showing their returns (excluding dividend!) over the past 10 years:

source : ycharts

While I hold all these companies in my portfolio today, I didn’t purchase them 10 years ago. But I truly wish I had! Imagine what my portfolio would look like now!

I’ve taken the past 10 years as you can clearly see what happens if you buy dividend growing stocks right before a market catastrophe. 10 years later, they have almost all doubled in price. If you are expecting another market crash tomorrow, they would all still show a +50% at the end of the drop. And no matter if the crash happens or not, they will all continue to pay you bigger and bigger cheques each month.

Now, do you understand why dividend investing is so popular?

On The Road #4

Each week, I’ll update you on my one year trip. I’ve decided to leave everything behind and spend real time with the people that matter the most in my life: my wife and three children. This is my story, I hope it will inspire you to create yours.

Date: from July 3rd to July 11th

Miles on the road so far: 4,154

States/Province traveled through: Alberta

I’m writing this article while I’m finishing up my visit in Jasper and heading toward Banff. For the first time, we decided to stay 4 nights at the same place. We heard lots of good things about Jasper and this is one of the reasons we decided to do this. But you will only read about the marvels we found in Jasper at the end of this chronicle ;-).

Day #24 1st meeting with a reader!

Leaving the Indian campsite wasn’t too hard. The dump was flooding before we could even use it and I just wanted to leave this place after 3 days. The good thing is that I was able to work properly, get some important stuff done and get back to my writing schedule. To be honest, I thought working on the road was going to be easier. We haven’t stopped much since the beginning of our trip and it’s starting to weigh on everyone. I feel somewhat we all need a break, but I’m not sure how we can make this happen.

My wife and I have talked about this issue for the past few days. The fact that we had to “rush our way” towards Yellowstone got everyone trying to catch their breath. The other thing we find difficult is how late the sun goes down. On one hand, it’s amazing as you can do things until 10pm and the sun is still shining. The bad side is that our children rarely go to sleep before 10pm leaving us little time to achieve tasks such as working or finding out where we will be sleeping next. Now we are heading back to Alberta and it almost feels like home!

Today was a special day as I was going to meet my first reader on the road. His name is Michael. He was kind enough to suggest a stop at the Waterton Park (the Canadian portion of the Glacier State Park). While we couldn’t hike the Glacier, the small hike in Waterton was great. We could admire a very nice view from there:

On our way back, we decided to stop by the small village and work a little. We enjoyed having easy WiFi access in a lovely village:

Honestly, I would have stayed 3 days here instead of the Glacier if I had known! Hahaha! Later on, we hit the road to Lethbridge in order to meet Michael and his wife. I was a bit nervous to meet with a “stranger” that knows more about me than I know of him! It was a very smooth encounter while my wife had to practice her English a little bit more :-). It was nice to enjoy a beer and chat for a while. It felt like a pause during a big day! We slept in front of his house and left the next morning for the Dinosaur Park.

Day #25-26-27 Feeling Like Home in… Wainwright !?!

We got to the Dinosaur National Park a little bit before noon. I was surprised to see how Alberta’s badlands were similar to South Dakota’s. It was very nice to be able to walk through them on small trails. We could climb small mountains and it felt like we were on the top of the world in our pictures:

I was really looking forward to seeing the fossils found in the Dinosaur park and so were my two boys. Imagine our disappointment when we found out there were only 2 little cages of glass showing a few pieces of dinosaurs.. That’s it! They call it the Dinosaur Park because there were dozens and dozens of fossils, but they are all gone! All that is left are small trails you walk in the hopes of finding more… which doesn’t happen! It’s a good thing it was free and it was on our way to Wainwright because there was really nothing to see there! I’ll save you the trip and give you the fossils right here:

There you go! You will not have to go to Alberta’s badlands (I could only imagine how people camping there were disappointed, I couldn’t picture myself spending a one week of vacation hardly earned and wasted it with 2 fossils hahaha!!!).

Then, we hit the road to get to Wainwright. Why the heck would we waste our precious gasoline (that we are now paying double the price than in the U.S.!) to go to Wainwright? Be honest, how many of you knew where this city was before reading my blog? I drove for 300 km, mostly in secondary roads (one was in construction and I felt like doing trails again with my RV!) to get to this small city in the middle of nowhere, 2 hours east of Edmonton. The reason why we wanted to go there is that my sister-in-law has a friend who lives there and she was kind enough to welcome us on her land. Just look at where we stayed for 3 days:

It’s funny that I really enjoyed these 3 days as we didn’t do much. We simply lived a normal life, mostly chilling by the valley. Catherine, our host, was super sweet and was coming by our RV each evening after her day of work. We thanked her with a good dinner with beef ribs and sausages and ended the evening with marshmallows on the fire.

The kids enjoyed feeding horses and even shoveling their poop (let me tell you that 3 horses make a lot of work for my 3 cowboys!). It was fun to connect with Catherine and enjoy this marvelous place.

Day #28 West Edmonton Mall

When I published my itinerary, some of you had doubts about us visiting Edmonton. Why would we visit this city anyway? The answer is quite simple: to buy peace ;-). We are asking our children to follow us in this crazy adventure and we also ask them to go on lots of hikes visiting landscapes through National Parks. For children of their ages, a mountain doesn’t always look as fun as going to the park. Spending a day at the WEM Waterpark sounded like a very good idea to keep them interested in our trip. And you can tell it worked:

After this great day in Edmonton, we were super happy to stay at a Walmart in Spruce Grove, not too far from Edmonton. Bummer! They don’t accept campers anymore. Some brilliant overnight campers thought it was a good idea to drop off their trash in the parking to thank Walmart for the hospitality. After a series of unfortunate events, the Walmart is not welcoming campers anymore… Nice! I’m now down for a 3 hours drive before we hit the next Walmart. The good news is that we will be closer to Jasper the next morning ;-).

Day #29-30-31-32

We started our day with lots of amazement! Jasper National Park is phenomenal! I enjoyed simply driving across emerald lakes wrapped by gigantic mountains. The more you drive into the park, the more you feel like you are entering another world where the king is not human. Nature is surrounding us with its beauty and by its strength. Since we had the chance to get to Jasper early, we did many things. The first one was to take the Jasper Sky Tram. Honestly, while the view was great on top of the mountain, I would have skipped that (especially for the price of $105 for 5 tickets!). But I have to live & learn and this is a mistake I will not make again. The thing is that to get on the top of this mountain, it was a hike of 7km (one way). There is no way I could have done it with my 3 kids! At least, we were able to do the last 1,5km on the top of the mountain for a short hike!

Later on, we decided to explore the small village of Jasper:

It is quite a feeling to have the Rockies hiding behind each building, each house. I have never felt this small!

For the first two nights, we had to sleep in a parking lot since all the campgrounds were full. This led us to explore a nice place to cook our pasta and we finally had dinner on Beauvert lake:

The next morning, we went for a great hike on the Sulpher Skyline. It was the highest hike we had done so far in terms of elevation. You can see the view from the summit:

It was astounding to admire the Rockies all around us. We felt like we were on the top of the world! We had lunch (always be cautious of chipmunks, they are eager to share your lunch!) on the top and to take a moment to hear the silence. We were among the first hikers of the day to reach the summit, it was calm and the mountain offered some kind of comfort. The best part about this hike is that there are natural sources of hot water. They made pools that look like a small spa and it is open to families :-). We then relaxed in waters at 40 degrees celsius and admire the mountain we just hiked.

Then, we had ran into a small surprise. You know, the things you don’t expect during traveling but bring you special images in your mind. While we were going back to our campground, we noticed several people walking on a river. It was a large, majestic river going through 2 mountains. But the level of water was minimal. Therefore, we could walk right in the middle of the river and not even have water up to our knees:

It was a nice break on an already successful day!

We spent our third day exploring Lac Maligne and its canyon. To be honest, I wasn’t much impressed by the lake (pictures of this lake are amazing but they are all taken while it’s bright and sunny). We currently have nice weather but the sun is hidden behind clouds most of the time. However, the Canyon was amazing! We learned about all factors contributing to digging the canyon. We even learned that the Maligne Canyon was once an underground river that crumbled and created a canyon. The view on the river was just amazing:

The rest of the day was quite relaxing while we had to do the “travelers boring stuff”. This includes the following items:

- Fill the fuel tank

- Fill the propane tank

- Empty the other tanks

- Do your laundry (and walk across Jasper village with two huge bags full of clothes)

- Forget your fuel cap at the gas station and realize that someone really took it and left (now I have duck tape over my fuel entry… love it!)

We spent our last full day in Jasper in our RV. For the first time since we left, it is a 100% rainy day. We all agreed to skip the bike ride we had planned and do school and work instead. I obviously wouldn’t take several days like this in a row, but since it’s our first day in the RV since we left, I actually enjoyed it! For once, I can work all I want and nobody is waiting for me ;-).

Later on today, I will go to Jasper to buy another fuel cap… hopefully it will work out!

Cheers,

Mike

Methodology I Use to Build Outperforming Portfolios

When I started investing, I was young and reckless. I enjoyed the opportunity to start my investing journey at a relatively young age (23) and make my mistakes with smaller numbers. My first three years in the investing world was crowned by success. I rapidly built a $50,000 cash down payment to buy my first house. However, the risk I was taking and the lack of diligence in my investment methods finally hurt me in 2006-2007. Then, 2008 arrived and it wasn’t the time to change anything since everything was falling apart. However, I realized that losing money on trades was the red flag that told me I was doing something wrong.

At this time, I started to do more research and decided to change my investing strategy. In 2010, I decided to select dividend growth investing as the basis of my holdings. Between 2010 and 2012, I worked on building a complete investing process that will guide me during good and bad times. An investing process that will guide my buying, selling and holding decisions when the horizon gets darker. I wish I could tell you that I started this investing strategy in 2003 and give you 13 years worth of results (and I eventually will), but in the meantime, I still wanted to share my methodology with you as it has been proven successful so far. Here’s what I’ve done so far.

#1 Identify your investing goal

It may sound stupid and simplistic, but the very first thing I did was to establish my investing goal. Some people just invest with the hopes of making money. I don’t think this kind of goal is well defined. As investors, we obviously want to make more money. What can we hope for if we invest $100,000 and withdraw $74,000 from it?

If you want to reach the $1,000,000-million-dollar bar before turning 55, you already have a better goal. This goal definition implies that you will have to investing X per year at a rate of Y during Z number of years. Then, you start by having something tangible.

Since I knew my savings capacity was going to be hectic in my 30s (notably because I have stopped working for 12 months in order to travel the world), I couldn’t reach such a defined investing goal. So far, my investing goal is to be able to build a portfolio that will generate an ever increasing dividend income while beating my benchmarks (a Canadian and a US dividend ETF). The reason why I aim to beat my benchmarks is simple; if I don’t beat them, I should rather simply invest in those 2 ETFs and never spend more than 30 minutes per year on my portfolio! I would save lots of time and could use it to make more money working on something else ;-).

#2 Build an investing process

The biggest advantage of building an investing process is that you will avoid doubting your decisions all the time. I’ve discussed this with many investors since I started running this blog and the same questions come up often:

When should I buy?

When should I sell?

When should I enter the market?

When should I exit the market?

Is there a bull market coming or another bubble crash?

I’ve personally found the answers to all these questions by defining my own investing process. Based on academic studies and tested on my own portfolios, I’ve built 7 investing principles:

Principle #1: High Dividend Yield Doesn’t Equal High Returns

Principle #2: Focus on Dividend Growth

Principle #3: Find Sustainable Dividend Growth Stocks

Principle #4: The Business Model Ensures Future Growth

Principle #5: Buy When You Have Money in Hand – At The Right Valuation

Principle #6: The Rationale Used to Buy is Also Used to Sell

Principle #7: Think Core, Think Growth

The rationale and financial research used to build these principles can be found here. These rules have helped me to shape a long horizon dividend growth portfolio that has been performing very well. In addition to my own portfolios, I’ve also built 12 real-life portfolio models applying the same rules. These 12 portfolios are doing very well compared their benchmarks. You can get my portfolio return details here if you are curious ;-).

By the simple fact of applying these 7 principles to my investing decisions, I skip emotional mistakes and doubt. I never have more than 2-3% of my portfolio sitting in a cash account as I can always find a good opportunity. At the beginning of this year, I even decided to build my children tuition fund portfolio based on the same principles and I’ve never been worried even if the US economic numbers weren’t as good as expected or if the Brexit shook the market not so long ago. This portfolio has been built on solid ground and I will not change my mind since I know I’m doing the right thing. Without having solid background checks and a real set of rules, I would be less confident in my investing decision.

#3 Build a solid asset allocation

It is very possible to find several interesting companies in the same sector while pulling stock filters. It is without surprise that all the oil & gas and railroads companies are showing numbers that are slowing down at the moment. Does this mean that all of them shouldn’t be on your buy list? Nope, it simple means that these specific sectors are going through a tough time. The same thing happens the other way. Not so long ago, dividend paying stocks in the consumer sector were showing very strong numbers before 2013. If you pick all of them thinking you have built a solid portfolio, you will be left with a bitter taste in your mouth later on. We saw exactly the same thing happening in the financial industry between 2003 and 2008.

This is why it is important to make sure you don’t own too many stocks from the same sector. I always try to have less than 20% of my money invested in the same sector. The more sectors you have, the better your asset allocation will be. This will greatly help you to even out your investment performance year after year.

#4 Review holdings quarterly

During each earnings’ season, I take a pause to read about my holdings’ results and what the future looks like. The point is not to trade any of my holdings based on a bad quarter or a bad series of quarters. Unfortunately, it impossible to hold companies that show growth each quarter. Currency headwinds (I’m sure you read that one a lot!), challenging economic news or new factors are coming into play each year for each type of business. What is interesting is to see from one quarter to another is how management reacts in front of a changing environment. What do they do to ensure the future of the company? How they will modify their course of action in order to pursue stronger dividend payments. This is the type of information I’m looking for.

If, for many quarters in a row, the company shows its inability to reverse an obvious trend or it simply doesn’t meet my reasons to buy shares in the first place, this is when I sell.

Final Thoughts

I don’t think all the specifics of my methodology are unique. I think I’ve done an honest job in finding key metrics and ratios to follow. However, I think the real success of this methodology, as with any other successful one, is that I never twist or replace my investing principles for others. I follow my strategy no matter if the market goes up or goes down. I think to be successful and achieve your investing goal; one must stick to their investing rules and never change them.

© Copyright 2013 Adividend