On The Road #11

As soon as I can, I’ll update you on my one year trip. I’ve decided to leave everything behind and spend real time with the people that matter the most in my life: my wife and three children. This is my story, I hope it will inspire you to create yours.

You can read my previous “On The Road” articles:

- On the road #1

- On the road #2

- On the road #3

- On the road #4

- On the road #5

- On the road #6

- On the road #7

- On the road #8

- On the road #9

- On the road #10

Date: from September 5th to September 25th

States/Province traveled through: Baja Norte & Baja Sur

I think it’s fair to write that it took us a full week in Mexico to adapt. Adapt to a new language, a new way of living and a complete new reality. As I’m writing this on the road, I’m comfortably seated on a balcony in front of the ocean in Cabo San Lucas. How did I ended-up in a cozy hotel room? Did I sell Freefall to travel from one hotel to another? Ah! You have to read my story to find out!

Baja Norte Days #85 to #90

Crossing the borders… this is where I left you the last time. I’ve heard so much and read so much about Mexico that I can’t even make myself an opinion. Funny enough, most people telling me it’s the dumbest thing to do (read the most dangerous) are the one who never set one foot in this country. They might have flown to those fancy 5 stars hotel, but they certainly never visited any “real” Mexican villages. Then, I’ve receive a whole different opinion from people who actually been to Mexico several time. This opinion is unanimous: it’s one of the greatest place to visit in the world.

Unfortunately, the mind is set to give a lot more priority to fear than positive sentiments. So it is with a heart crisped by fear that I drive Freefall through the Mexican gates. I’m not in panic mode, but I’m not the most relaxed guy on earth either. I can feel sweat dripping under my arm as I make my last turn before I get to the famous light. For those who don’t know, when you cross the Mexican borders, there is a light pole showing either a green light (meaning you can go without going through an inspection) and a red light (meaning you have to pull out your car and have a chat with the agent… standing with his big gun). They say the light goes random… but for some reason, the gringos with the big RV got the red light… go figure why! Hahaha!

The agent border is in fact a military that is quite pleasant. He discussed with us to know where we come from and where we are going. When we tell him about our project, he tells us how Guatemala is dangerous but Mexico is super safe (how ironic! Hahaha!). We quickly enter Mexico on our way to our first place to stay. Once again, we will use Harvest Host as the Baja has its own ruto del vino. Quite a pleasant start after all…

It’s a beautiful Sunday afternoon and there are lots of Mexican coming to this vineyard (L.A. Cetto).

The pressure cools down and we enjoy spending time here. It’s a weird feeling though as everybody is well dressed and we wear our “road trip clothing” which is pretty much just t-shirts and shirts. The feeling of not understanding a word that is spoken is also hard for me. Since the beginning of the trip, I go forward to meet new people and discuss with them. This time, I can’t really do that. I will definitely have to work on my Spanish during this trip!

On our second day, it’s time to fill up our RV with foods at Ensenada. I rapidly realise that moving my RV in a bigger city is quite a challenge. We completed our day without any problems, I now have a new iPhone with a Mexican cel package. Now that I have wifi, I’m a happy camper! Speaking of which, we discover our first Mexican camping. I’ve read that camping in Mexico isn’t exactly as clean as the one we have in North America. It’s too bad, because they have beautiful settings to establish nice campgrounds:

But they lack of maintenance…

Believe it or not, we did take our shower there ;-).

The next days were quite amazing. We had our first experience in eating in what I call a “boui-boui”:

It was delicious and Zabdi (the girl in the picture) is teaching us a few Spanish words while we discover their great tacos. Then, we found a little paradise right on the beach:

We will stay there for 2 days, camping right on the beach and I even caught a small sun burn while working on the beach:

Interesting enough, this beach is amazing but the water is very cold. We were told it was very hot in the Baja… I’m a little confused! We decide to continue further south and end-up in Bahia Los Angeles. It’s crazy how a day on the road and we are now getting incredibly warm weather. It’s now hitting 36-38 Celsius and it will be like that for the rest of our trip on the Baja. Needless to say that I had a hard time to deal with such weather… Once again, the camping is situated in an amazing, but all the junks left aside the beach leaves me less enthusiast about my first impression of Mexico.

We will spend a few days going down slightly everyday in order to find a great place to boondock. I find this period of the trip a little bit harder as we need to constantly lookout for resources. One day is doing our grocery in a small mercado with birds, dogs and flies all over the place, another day is stopping at the agua purrificada to fill my RV with fresh water and then, we look out for propane or more foods. There aren’t any cities on the road, but most likely small villages with dirt roads. This is a period of adaptation and I’m slowly trying to figure out how it works here. In fact, it’s pretty simple; you can pretty much do whatever you want and chill all along the way. You should never worry about anything and just let it go when it doesn’t go the way you want. It’s true that Mexicans are very helpful and smiling. We should simply adapt to their culture and follow their way!

Before going to Baja Sur, we will spend a few days in a perfect boondocking place:

This is where I’ve celebrated my 35th birthday. When I was 30, my goal was to become millionaire at the age of 35. I was on my way to a great career and my online business was soaring. 5 years later, I’m far from being millionaire, but I can say that I will live my 35th year on earth like one. Taking this pause, enjoying life and spending time with my family make me feel like I’ve won the lottery. We don’t get much sleep due to the warm weather, we can’t speak with locals because we don’t understand much, we don’t have access to clean shower most of the time, we eat what we can find and it becomes to be repetitive, but this is not the important part. The important part is that we are living. Each morning, I wake up in an amazing place, my kids are around me and I can discuss with my wife while relaxing by the beach. There is no rush, there are no expectations, there are no performance. There is only us, going forward and discovering this country. At first, I was scared. But fear is something happening solely in your mind, nowhere else. After this first 10 days or so on the Baja, I realize that there is nothing to fear here. It’s only different and we only have to manage those differences and embrace them.

Baja Sur Days #91 to #105

Crossing to Baja Sur was somewhat fun. We had to get the RV fumigated by some kind of white liquid. I’m asked to pay a donation and I give the guy 20 pesos. Our friends behind us are ask for 20 pesos as well but received a receipt… go figure!

To be honest, I wasn’t impressed that much by the first part of the Baja. The junks on their beautiful beaches and the difficulty of having access to basic resources kind make this part of the trip “ordinary”. However, after spending my birthday in Bahia Concepcion, things started to turn around the other way. We ran into our first “small colonial city” named Lorretto. I was excited to walk around the city and enter the small shops.

I now start to understand a little bit of Spanish and I can shoot a few words here and there. Enough to bargain our first purchases. I’m also getting better at negotiating our campground price. It seems the price asked for anything in Mexico is never the “real price”. I particularly like it and getting better at this game!

During our trip in the Baja Sur, Mexicans celebrated their Independence. We happened to arrive in a campground with a big fiesta going on. Kids rapidly integrated ours and William even showed that even Canadian can scores goals at soccer:

We spent our last week of the Baja between La Paz and Cabo San Lucas. This small peninsula is just amazing. La Paz is a great city with a lot of things going on. They have a beautiful boardwalk where we spent several hours. We were even able to boondock by the beach and enjoy a small breeze.

Tired of all that warm weather, I decided to call 3 days off in a hotel in Cabo San Lucas. This was quite far away from the way we lived for the past 3 months in our RV, but man it felt good to have space for everyone.

We took those 3 days to let the dust of the past 3 weeks settle down. It was quite an adaptation to a new culture, a new way of living, a new language, a suffocating weather and also traveling with another family. While it was a lot of fun at first, things aren’t going too well with the other family. It’s nothing related to us, but the woman has a hard time adapting to Mexico. It creates lots of tension between her and her husband and the ambiance is sometimes a bit tense. Taking a few days off within our family made us appreciate our couple and our family even more. My wife and I are on the same page and we want to keep going forward. It’s truly solidifying our bonds.

At the same time, I realized how I was shocked to see those tourists in Cabo San Lucas trying to get drunk by noon in the hotel pool. This small city is full of stores and it really looks like we are in USA again. A lot of consumption, a lot of flashy dresses and cars, a lot of superficial. I’ve truly enjoyed my time in the hotel room with a real bathroom and the A/C on all the time. But I now know I don’t want this life anymore. I don’t want to buy more stuff and burn my energy and money on meaningful things. When I come back, I know it will be different.

On September 25th, we joined the other family and we took the ferry to hit the main land. Will they continue with us? What happened on the mainland? This will happen in my next on the road. Note: I promise to be faster next time! Hehehe!

The Shocking Truth about Dividend Growth

A while ago, I wrote an article about the key metrics to find strong dividend growth stocks. This article opened a discussion with one of my readers, Ron, as he preferred higher dividend yield companies. He agreed to share with us the result of a very interesting calculation he made. He also wrote a quick article to explain what he found.

The Shocking Truth About Dividend Growth

Today, I was reading another dividend investing book and some statements by the author got me to thinking. What is the definition of investment “risk” and how should it enter into one’s thinking or decision making regarding dividend investing?

Many dividend investment consultants suggest or advise against relying too much on high current yields when selecting or constructing a dividend producing portfolio. I will not go into all the possible risks and reasons why a dividend may be “too high”, as I am certain you know them better than I do. You also know by now that I feel that settling on a low or average initial yield may be very costly for the investor, particularly if his investment time frame is less than 20 years.

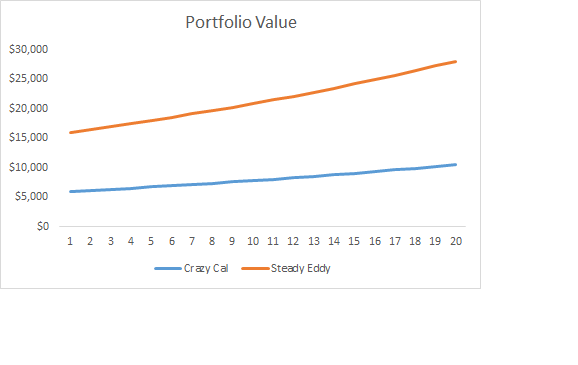

Most of us have a difficult time trying to quantify yields versus dividend growth rates (DWRs) versus number of investment years and comparing what it means in real dollars, etc. so I thought I would make a chart comparing a couple of fictitious dividend investor portfolios and their stories.

Two investors have $10,000 to build their dividend investment portfolio, and both know enough to split the total investment equally between 10 different securities in this situation. Both plan to reinvest all of their dividends for 20 years.

Steady Eddy is a guy who has read all the investment advice and carefully picks his securities. His portfolio ends up with an initial yield of 3% and DGR of 8%. All of his stocks are blue-chippers.

Crazy Cal is a guy who does not have the patience to read everything on investing, but has some gut feels and has even visited Las Vegas. But he is not dumb either, and builds his portfolio with an initial yield of 5% and DGR of 8%. He figures he needs to beat inflation and after all these were not penny stocks but pretty good stocks with a pretty good track record at least recently.

Steady Eddy tells Crazy Cal that he is being too risky and doesn’t he realize what can happen. Crazy Cal doesn’t pay attention and takes a vacation in Vegas.

Well… unfortunately for Crazy Cal the stuff hits the fan for some of his securities and within 1 month of purchase 4 of the 10 securities have their dividends cut and within the next months all 4 of these securities go belly up… as in zilch, nada, worth zero!! What bad luck. Well this is exactly the type of thing Steady Eddy warned him against. His original $10,000, 10 stock portfolio is now a $6,000, 6 stock portfolio. Crazy Cal goes into hiding wondering how stupid can he be.

A few years go by and Steady Eddy and Crazy Cal meet up again and Steady Eddy can’t help but remember the dividend investing catastrophe of his buddy and ribs him about his own last year’s dividends. “What?”… Responds Crazy Cal…”My dividends were exactly the same!” Sure enough after getting out their respective records it was clear that Crazy Cal’s yearly dividends on his $6,000 portfolio was exactly the same as Steady Eddy.

The moral of this story is that although risk is something to be aware of in investing, it should also be analyzed to determine its true or actual cost. Trying to reduce all risk by being too conservative can reduce investment returns by surprising amounts. In this case, having catastrophic results for 40% of the picks still works out better than being conservative. I do not think most people would anticipate this outcome with the above example.

-Ron-

Further Thoughts on Ron’s Article

I was quite surprised to see the outcome of Ron’s little story. But when I started thinking about it, I found out it made sense. After all, a 3% dividend yield is 60% of 5% and $6,000 is the same percentage (60%) of $10,000. On year 1, both portfolio would generate the same amount in dividend income, so $300. Then, both portfolio payments would grow at the same pace assuming the same dividend growth rate.

However, there is more thought to be added to such rationale. The first one is the end portfolio value. While both portfolios generate the same income, Steady Eddy ends up with over $7,000 more than Crazy Cal after 20 years:

This means that Steady Eddy could start withdrawing from its capital and boosts its yearly income for several years before getting back to Crazy Cal’s level. Even if Steady Eddy doesn’t touch its capital, then his heirs will still be happier to receive a bigger amount ;-).

The second point to consider is the dividend growth rate. It is unlikely to happen that a set of companies paying a 5% yield will increase at the same rate as a set of companies paying a 3% dividend yield. The rationale behind this statement is simple, but so true: higher yielding stocks always come with additional risk. This is one of the basics of finance 101: when an asset is riskier, the expected return by investors must be higher. This is also the case with the dividend payment. I’m not saying it’s impossible that you find a few companies that challenge my theory, but I’d be quite curious to see a portfolio of 10 companies showing a 5% dividend yield 10 years ago and posting an 8% dividend growth rate since then.

Overall, Ron’s rationale makes sense. However, I think that a short story is always more complicated when you factor everything in. There is rarely a black & white answer when you discuss investing strategies.

On The Road #10

As soon as I can, I’ll update you on my one year trip. I’ve decided to leave everything behind and spend real time with the people that matter the most in my life: my wife and three children. This is my story, I hope it will inspire you to create yours.

You can read my previous “on the road” articles:

On the road #1

On the road #2

On the road #3

On the road #4

On the road #5

On the road #6

On the road #7

On the road #8

On the road #9

Date: from August 25th to September 4th

Miles on the road so far:

States/Province traveled through: Arizona, California

As I’m writing this on the road, I’m already in Mexico. It seems that I’ve already taken a slower beat and getting a little bit behind! Honestly, there was a serious time of adaptation required and this is the reason I’ve focused on what I do best (write about dividend stuff) instead of continuing my journal for a while. But for now, let’s get back to where we were at the end of my latest on the road.

Days #74-75-76-77-78 The Beauty of Antelope, Grand Canyon & Arizona

We finally decided to stayed a lot longer than expected at Lone Rock Beach on the Lake Powell. As I previously mentioned, we were supposed to stayed 1 night. That night got into 4 and finally finished by 6 nights at the very same place. What is really nice when you stay for a while is that you get to know other people. We were lucky to chat almost everyday with an retired couple Nic & Judy. Nic is German, but spent most of his life in the Caribbean’s. He built a company there and made some good money. He is now traveling across the states and visit Judy’s daughter in Canada everyday and spend the rest of his time on an island (can life be any better?). I appreciated the long chat we had and tried to soak as much wisdom as I could from this well accomplished man. He told me the stories about how he was dyslectic, quit school at the age of 15 to go work on a farm and left Germany to Africa at the age of 18. He learned French and English while traveling and at the age of 21, he bought his first tuck boat. A few years later, we was building a tuck boat company in the Caribbean’s and started to build his business. I think the most important thing he told me was: everything leads to something. All experiences open opportunities and it is up to you to seize them. When there is a problem, there is also a gain to be made out of it. I’ll be sure to remember this!

During our last two days in Lake Powell, we took good care of Freefall. We wanted to make sure our RV was in good shape to keep going. I was relieved to learn I only had to change breaks! We also take the Antelope Canyon tour. This is one of the rare attraction we paid for during our trip. However, it was definitely worth the expense!

They take you in a pick-up and bring you directly in the Antelope Canyon. I’ve seen so many pictures of this Canyon that I thought I had seen it. But the beauty of carved stones dancing around you and climbing up to the sky is impossible to describe. We picked one of the earliest tour (as they sold out weeks in advance!) but it gave us the opportunity to have less people in the canyon at the same time. I recommend it to everybody!

After a very relaxing stop by the beach, left early in the morning to go see the Grand Canyon. Nic had recommended we go see the North Rim as it is less crowded while almost as spectacular than the South Rim (plus, I’ll show you picture you probably haven’t seen yet ;-). We made several stops on that day. One was to see the Horseshoe Bend:

And another one to see those gigantic boulder standing on smaller rocks:

And finally, we finished the day with the Grand Canyon Wow… this is quite impressive to see how wide and deep the canyon is!

As we were walking near the cliff, my adventurous side was continuously looking after a lonely rock where we could sit and admire the view all alone. After only a few minutes, I rapidly found the perfect spot. I could even climb there with my kids. They have climbed so many rocks so far I call them my mountain goats ;-). As we were two rocks away from reaching our objective, I contemplated the horizon with great excitement. But I had a weird feeling at the same time. I felt I was being looked at. In fact, I felt I was being stared at. I quickly turn around and I was ready to face any kind of wildlife in front of me… but that was just a ranger telling me I should go down and follow the path… darn! I got caught before I could enjoy the view! Nonetheless, we found many other ways to spend countless minutes staring at the immensity of the canyon… legally!

Thx to Nic, we also spent a really neat and calm night in the forest nearby for free. This was the perfect boondock!

We finished our trip in Arizona by going through Sonora. The road scenery was amazing. We had countless red rocks leading the way while we were driving through the mountains. We even found the perfect spot to stop and enjoy the afternoon nearby natural water slides in a State Park nearby:

We finally stopped our ride in a camping for 2 days, just enough time for me to work a little and play mini golf ;-).

Day #79-80 LA & Its 12 Lanes Highways

We woke up very early that day as we had to drive the whole day from Cottonwoods (where the camping is at) and Los Angeles. We found another amazing couple of Boondockers Welcome ready to host us for the night.

As I was approaching L.A., I remember how difficult it could become to drive with my big bertha in the middle of a fast highway. But L.A. is completely different; there are 10 times the number of highways and lanes! Fortunately, I was lucky enough to not get stuck into too much traffic and reach our host house before 5pm. I couldn’t hope for a better place to stop. This couple lives in Manathan Beach; a very nice neighborhood nearby L.A… and nearby the beach. We had enough time to take a walk and chill on the beach after this long day of driving. The place was incredibly calm and family friendly. We stayed there a good hour, just looking at the beach and enjoying the landscape.

After we ate our supper, our host knocked on our door and offered us to take a glass of wine and chat in their house. Once again, it was another great encounter. It was fascinating to learn that they bought their first house in Manathan Beach for $29,000 almost 45 years ago and it is now worth about 2,9M$! That’s inflation! Funny enough house pricing in Quebec was similar back 45 years go, but the $29,000 house only worth $200,000 today…. Not $2M…

The next morning, we finally meet with the family we encountered during the very first day of our trip. They rushed their way to L.A. so we can meet before crossing the borders. At this point, I can tell you how I was happy to find another family doing the same trip. Crossing the border toward Mexico is not just a step in our itinerary anymore, it’s a reality! Going right in the mouth of the unknown will be another challenge.

We spent the day at Venice Beach. This wasn’t really my choice and I really had the feeling that I lost my day there. Venice Beach is full of cheap stores offering cheap stuff and there are also a bunch of weirdos. It’s an interesting mix, but after working 5 years downtown, I’ve seen enough weirdos that I don’t look at them with interest anymore. We finished the day in a Walmart not too far away from LA. It was a quick trip of 48 hrs in this megapole. I don’t think I will come back though. Not really my type of city, it’s just too big for me.

Day #81-82-83-84 One Last Glass of Wine Before We Go

The next few days are days of preparation. We Needed to buy a few things before hitting the road again. While we were getting fully prepared, we decided to stay at one of the coolest Harvest Host there is: The Bernardo Winery.

This Vineyard has been built with a small village around it. Each door is a small store. You can buy chocolate, olive oil, there is a small coffee shop with amazing lattes, etc. Kids were playing around the village with our new walkie-talkie (that are definitely a must if you travel with another family!) while we were trying different type of wines. We spent 2 days there as we really enjoyed this place.

We did two lasts stops before going to Tecate. One was a campground do to our laundry and the second one was the closest campground to Tecate. It is situated in Portrero, about 5 miles away from the border. The day we crossed the border, we got there to buy our tourist card (which they call a visa) and got fooled by our very first Mexican ;-). The officer at the immigration office asked us $25 per tourist card. Once we paid, we got a receipt showing the price in pesos. I don’t recall exactly, but it was the equivalent to $20 USD. Welcome to Mexico my friend!

In my next on the road, I’ll tell you about my journey through the Baja!

13 Companies to build a Dividend Growth Portfolio with 10 years to go

October 04, 2016

In my latest article, I’ve discussed the metrics I would use to make a selection of dividend paying companies if I had only 10 years to build my portfolio. The idea of using a shorter time horizon was to show how limited you could be if you only select companies that are currently paying an interesting dividend now. When I wrote my first article about metrics to be used, I didn’t pull the stock filter yet. I just did in order to write this post. I’m not surprised, but the choice is very limited even considering a set of wide and generous metrics.

Choosing among companies with growth revenues and EPS that pays dividend over 3% and that still show payout ratios making sense seems to be a tough mission at the moment. There are lots of ADR’s that make it harder to evaluate. I tried to clean some of them (I mostly taken off Chinese companies) and the list shows a little bit over 100 companies including both U.S. and Canadian market. Due to the current market, we see several financial institutions. You can download the excel file here:

Click here to download

You will notice that there isn’t much choice. Still, I was able to pull out an interesting portfolio by combining both Canadian and U.S. stocks. I’ve built the following portfolio based on my 7 investing principles.

4 Canadian Companies

I would start building this portfolio with 3 Canadian Banks. In fact, several financial Canadian companies could have been included to build this strong portfolio. Unfortunately, picking all of them would lead you to a heavily concentrated portfolio in one sector, which is never good. For this reason, I’ve selected Royal Bank (RY.TO), TD Bank (TD.TO) and ScotiaBank (BNS.TO). The last Canadian companies I have selected is Rogers Communications (RCI.B.TO) as it also performs in an oligopoly.

Royal Banks (RY.TO) 4.08% Dividend Yield

Royal Bank provides various financial services to individuals as well as commercial and institutional clients. Their services range from regular banking, investments, insurance, brokerage, mortgages, loans, etc. RY recently purchased City National, a private & commercial bank for wealthy clients based in Los Angeles.

I consider RY as very interesting play as its capital market and wealth management sectors provide a strong and consistent revenue stream aside from traditional banking. They do an awesome job generating strong profits from capital markets and their wealth management division generates revenues from over 15 million clients. Their recent purchase in LA is already increasing RY total revenue as per their latest report.

TD Bank (TD.TO) 3.76% Dividend Yield

On top of being a leader in Canada, TD is also the most productive Canadian Bank (e.g., more earnings relative to its risk-weighted assets). Its earnings volatility is lower than its peers due to less exposure to capital markets. Finally, TD has deployed a very lean structure into its branches which benefit greatly from their expansion in Quebec and the US. TD Bank is now known as “America’s Most Convenient Bank.” TD has recently beat analysts’ estimates once again. Their lean structure gives them one of the best customer service scores across Canada.

I’ve picked TD for its great presence in the US as compared to other Canadian banks. This is a market that will continue to grow and compensate for a slow Canadian economy growth. While Royal Bank and National Bank are performing on the capital market, TD has opted for stability with a more classic banking model. For a dividend investor; this means a stable business model providing predictable dividend increase. Two things we like! Finally, TD is successfully gaining market share in Quebec, a long time ignored market from the big 5.

ScotiaBank (BNS.TO) 4.19% Dividend Yield

ScotiaBank, is the third-largest bank in Canada in terms of asset base. It provides various financial services to individuals as well as commercial and institutional clients. Their services range from regular banking, investments, insurance, brokerage, mortgages, loans, etc. BNS is the most “international” Canadian bank serving a total of 21 million clients spread across 55 countries.

BNS is also highly invested in commodities, which hasn’t been a plus in 2015 but has been a good thing for 2016. The stock is up by 26% since the beginning of the year as the oil market is recuperating. sIts total loan exposure in the oil & gas industry is up to $15.5 billion (source Scotiabank investor presentation). Now that the situation of the barrel of oil has stabilized, we will see which companies may default on their loans in this new environment.

Rogers Communications (RCI.B) 3.45% Dividend Yield

Rogers (RCI.B) is a diversified communications and media company. The company is divided into three divisions: wireless, cable and media. While the Rogers business is similar to Telus when we compare wireless and cable services, RCI.B has an extra division called media. Rogers broadcasting has increased, notably through the acquisition of the Toronto Maple Leafs and the ownership of the Blue Jays that will certainly feed Rogers Sportsnet.

Rogers is well established in various markets and it has recently made another interesting play: they secured the rights to NHL broadcasting exclusivity for 10 years. The deal by itself should not add huge profits to the table but if RCI is able to leverage its broadcasting to promote their other brands (such as mobile services), this contract will be worth every penny.

9 U.S. Companies

The U.S. stock market shows some interesting pick as well. I think we can build a solid portfolio paying over 3.50% dividend yield at the very beginning through this list. Once again, those selections have been made based on my 7 Investing Principles.

Cal-Maine (CALM) 5.57% Dividend Yield

Cal-Maine Foods is a leading producer and supplier of consistently, high quality fresh eggs and egg products in the United States. The company, founded in 1957, is known for growing rapidly through acquisitions. Since 1989, the company has successfully acquired 18 existing egg production and processing facilities. It is a fully integrated egg producer. Cal-Maine sells 90% of its eggs to retail buyers such as Wal-Mart, Costco, Food Lion, etc.

It issues special dividends according to their revenues and profits. Don’t be shocked when you check their dividend payout trends, it goes up and down, but always pays a strong dividend for the year.

Cummins (CMI) 3.13% Dividend Yield

CMI has been more than generous with its shareholders over the past 5 years. In fact, the company shows a dividend growth rate of 32.03% CAGR. The company will not be able to maintain such a strong trend, but it is definitely in a good position to keep increasing its payment year after year considering both payout and cash payout ratios around 50%.

An investment in CMI is based on its ability to protect its know-how in designing more eco-friendly engines. New markets are slowly but surely opening up to Cummins due to this specific expertise. Europe in the upcoming years and later China & India will also improve their environmental rules with regards to emissions. They will then open the doors to company such as Cummins to benefit from their expertise. CMI has already created partnerships with important clients such as TATA in India. It is very difficult for its competitors to catch up on 10 years of massive R&D investments to develop such technology. This is how Cummins should keep its competitive advantage for a while.

Emerson Electric (EMR) 3.59% Dividend Yield

Emerson Electric is part of the 18 Dividend Kings. EMR specialises in high tech products and services for its customers. The company shows two divisions which are commercial & residential solutions and automation solutions. Automation solutions is the biggest segment with roughly 2/3 of the company sales in 2015. Its most recent growth vector has been found in China and India as they participate in building important cold-chain infrastructure to keep food fresh. Both countries lose billions due to wasted food. EMR’s performance is also highly linked to providing techno solutions to the oil & gas industry.

EMR could show stronger numbers a few years from now once the oil industry is back on its feet. In the meantime, climate control technology should be EMR’s focus to bring additional growth within its business model.

Eaton (ETN) 3.35% Dividend Yield

Eaton is part of the elite group of dividend aristocrats due to its 32 consecutive years of dividend increase. Still I have the feeling we don’t see this name often in the financial news. On top of this, Eaton is working in the trendy environment of “energy efficient solutions”. The company offers solutions to help customers manage electrical, hydraulic and mechanical power in an efficient way. The company works in two different sectors, each split into the following segments:

The Electric sector:

- Products (32% of total sales)

- Systems & Services (29% of total sales)

- The industrial sector:

- Hydraulics (13% of sales)

- Aerospace (8% of sales)

- Vehicle (18% of sales)

The company currently sits on a solid business model, but evolves in a cyclical environment. Patient investors will see a great opportunity to invest in a solid dividend growth stock while enjoying a 3%+ dividend yield.

GAP (GAP) 3.85% Dividend Yield

GAP owns several well known brand in the clothing across the world. Among their portfolio brand, they have Gap, Banana Republic, Old Navy, Athleta and Intermix. Their business model is based on strong brand recognition and corporate operated stores. GAP has found ways to connect with their clients through mobile phone app and internet.

The company is carefully selecting their store location in order to insure the success of each store.

Maiden Holdings (MHLD) 4.02%

Maiden Holdings Ltd (MHLD) is organized to provide, through an insurance subsidiary, property and casualty insurance and reinsurance business solutions mainly to small insurance companies and program underwriting agents in the United States and Europe. The company is based in Bermuda.

MHLD is evolving in a relatively stable and predictable market. The company focuses on building strong partnerships with insurance companies that constantly require MHLD services to pursue their business. This is an unusual holding in a conservative portfolio, but it’s dividend growth perspective has made MHLD a very good pick for the past couple of years.

Qualcomm (QCOM) 3.19%

Qualcomm Inc develops digital communication technology called CDMA (Code Division Multiple Access), & owns intellectual property applicable to products that implement any version of CDMA including patents, patent applications & trade secrets. The company derives most of its income from the smartphone business selling chips for power and network connectivity. Essentially, phones are unable to connect to 3G networks without paying a royalty (about 3%-5% of the price of the handset) to the company.

Its leadership position in the 4G LTE chipset arena and strong relationships with major smartphone makers establish solid bases for an ever increasing cash flow. However, nothing is perfect in the mobile industry. QCOM is facing serious collection problems in China and it is currently losing market share among the biggest smartphone players such as Samsung and Apple. There are also regulation issues pointing ahead where some countries (like South Korea) are determining that the royalty should not be paid based on the smartphone full price.

For these reasons, QCOM’s stock price has seriously declined over the past 12 months. However, you may not want to ignore the fact that QCOM technology will become even more important in the future. Since all devices are getting connected (they call this the “internet of things”), the usage of smartphones (and the networks they require) will become even more important in the future. It’s definitely a company to have a look at!

Target (TGT) 3.22% Dividend Yield

It is hard to find a consumer stock paying over 3% right now. However, Target seems to fit well for our portfolio. Target Corp is engaged in operating general merchandise discount stores in the United States. Target benefits from a strong brand, great location and several signature products. The company emphasis more on retail products than food (compared to Wal-Mart, Costco, etc).

The fact that Target is leaving food aside to concentrate on retail products makes it a differentiation factor for them. Instead, TGT focuses in the superior in-store experience compare to its competitors. For this reason, Target generates higher margins than Wal-Mart, Costco and Kroger.

Verizon (VZ) 4.27% Dividend Yield

Verizon is the leader in the wireless industry in the USA with a 34% market share (followed by T with 30%). I believe its reputation, based on quality, TV protects VZ from many competitors over the long haul. The company understands its clients, who would rather pay a premium for a phone that will work everywhere than a cheaper package with occasional problems.

I also like the fact the company is evolving in an oligopoly. While growth perspectives are not incredible within the wireless segment, Verizon has other alternatives to explore with the purchase of AOL in 2015. If it can unlock the value of AOL’s internet advertising platform by merging it to its wireless services, we could be back to higher dividend increases for a while.

Verizon is more a conservative stock that will generate a solid cash flow. At the moment, it could also easily fit into a growth portfolio if you are one of the believers in the AOL acquisition. This could be definitely be a game changer for Verizon. Higher risk, higher reward.

Final Portfolio 3.82% Dividend Yield

Overall, I think this portfolio shows enough diversification while offering a good dividend yield. In 10 years I think it is safe to say that this portfolio will generate somewhere around 6% base on the cost of purchase. This is definitely a great start for someone who doesn’t have 30 years in front of them to build their portfolio. What do you think?

If I Had 10 Years to Build a Dividend Portfolio

September 29, 2016

When we think about dividend growth investing, we often think about a horizon of 20, 30 even 40 years in front of us. The true power of dividend growth investing can only be unleashed after such a long period of time. After all, owning shares of Coca-Cola (KO) with a 3% dividend yield is not that impressive. However, this company had maintained a dividend growth rate of 7% for over a decade now. This means that if you wait 7 years, your dividend yield based on your cost of purchase becomes 6%, if you wait 14 years, 12% and so on….

Unfortunately, we don’t all have 40 years in front of us. After discussing this matter with several older investors, they have expressed the sentiment most bloggers and financial advisors always presume we have 20-30 years in front of us to build a strong portfolio. If you decide to switch your investment strategy at the age of 50, it is getting a little bit late to build a dividend growth portfolio as you can’t virtually benefit from the power of compounding interest for a few decades. In this case, is it too late for you to build such portfolio? Should you quit and aim for another strategy? What kind of yield can you expect when you retire if you have only 10 years to build your portfolio?

These are the kinds of questions I had in mind while writing this article. What would I do if I had only 10 years to build my portfolio before retiring?

Main Concept; You don’t really have only 10 years…

One thing many investors forget about investing is that it doesn’t end when you retire. I agree with you; the best case scenario is when you can live off your dividends and never touch your capital. However, if you are 10 years from retirement and you decide to seriously invest, let’s face it; you are a little late for the parade. Nonetheless, it doesn’t mean that you should quit and give up on managing your money. Why? Because you have a lot more than 10 years to go…

Let’s assume you are 55 and you retire at 65. This leaves you with 10 years to build a retirement portfolio. However, on your 65th birthday, the money you have saved and invested doesn’t vanish overnight. Chances are you will live until the age of 85, then, it means you have 30 years of investing in front of you. Life is great, isn’t it?

I guess the main concept you have to give up is to live off your dividend and never touch the capital. Unless you are making lots of money or you have incredible saving abilities for your last ten years, I think it is inevitable that you will have to take a part of your retirement income from your capital. In fact, if you have built a solid dividend growth portfolio during your last 10 years, you will never outlive your capital if you withdraw around 4% of your capital each year (including dividends paid). This is a simple rule of thumb that has been proven over years.

Still, I would not go ahead and build the same portfolio that I’m building. Here’s what I would use as a filter to pull out a list of candidates.

#1 Dividend Yield over 3%

You already know my interest for low dividend yield paying stocks offering both strong dividends and capital appreciation growth potential. Companies like Disney (DIS), Apple (AAPL), 3m Co (MMM) are all amazing companies paying very low yield. Unfortunately, I would discard such companies with my first filter. Since we don’t have much time (10 years is very short) to build a strong dividend growth portfolio, we have to select companies that will at least beat inflation year after year.

When I pull out filters for my stock research, I usually put a maximum yield. This time, I will include higher dividend yield companies. Others metrics will clean-up the rotten fruit from the basket.

#2 Payout Ratio under 100%, Cash Payout ratio under 80%

I think the very first mistake I could make while building a higher yield portfolio is to not consider that higher yield paying companies might also be subject to cut their dividend. There is no point of selecting companies that will cut their dividend in the upcoming years. Companies with a payout ratio over 80% are playing with fire. They will eventually pause their dividend increase policy and might eventually stop it if the business is not doing well.

The payout ratio is less important for me compared to the cash payout ratio. This is the reason why I can accept a companies with a 100% payout ratio since it’s based on accounting principles. I would rather use the cash payout ratio as it is directly linked to the company’s bank account. If the cash payout ratio is over 100%, then the company has to borrow the money to distribute it to its shareholders.

#3 5 year Revenue & EPS Growth Positive

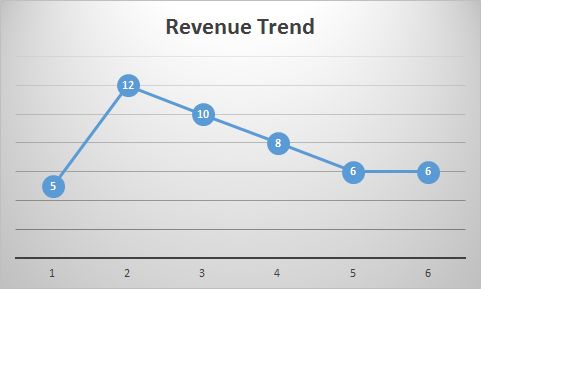

In an ideal world, I’d like to pull out a graph showing both revenue & EPS trends for the past 10 years. This is how I analyze companies. It looks like this:

Getting only the number for 5 years or 10 years can be misleading. Depending on when you pull out your metrics, the number could not tell the truth about the current situation. Imagine if you have a graph going like this:

The metric alone will post a small growth, but in reality, the company is struggling keeping up their sales up. However, while pulling out a filter, this is still a good start. You will have plenty of time to look into each companies when you shorten your lists.

#4 Positive 5 Year Dividend Growth

One key element of my strategy is to select companies with positive dividend growth perspectives. In an ideal world, I would require 5 consecutive years with a dividend increase as a minimum. Unfortunately, I don’t know of any stock filter giving me this information. This is why I take the 5 year dividend growth metric and will eventually look into each company. For me, there is no point of selecting companies with management that are not fully committed to increase their payouts year after year. The whole purpose of selecting dividend investing as my core strategy is to benefit from the power of compounding dividend growth over a long period of time. Remember, even if you have a time horizon of 10 years, chances are you will reap the benefit of your investments for another 20 years afterwards.

Is There Anything You Would Add?

I’m not a fan of pulling out 30 metrics with my filters. I already know I will have to look closely at each company individually before selecting them. This is why I rather pull out a larger list that will give me more options on how to shape my portfolio in the second test.

In the next article, I will start from the list generated by these metrics. But I’m curious to know if you would use any other metrics to build your retirement portfolio?

© Copyright 2013 Adividend