As is the case each year, I make a few transactions in my portfolio. As you may already know, I do very little tracking of my investing performance throughout the year. I’ve already discussed why I see little interest in reporting my dividend income and I prefer to measure my performance against the stock market in general or dividend focused ETFs such as VIG and XDV. However, I still look at my portfolio recap provided by my broker at the end of each year. Surprisingly, I found that my portfolio did well, but shows a very low yield. Is it a good thing?

To answer this question, I must look under the hood, right?

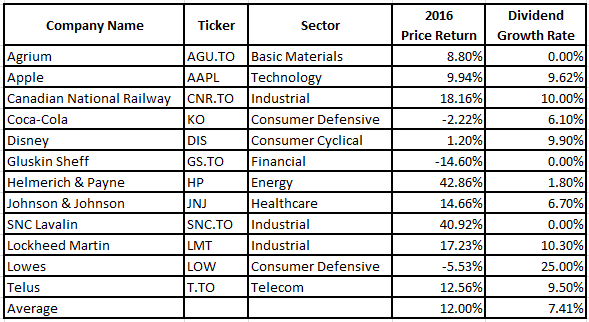

Retirement Account +11.20% – Yield: 2.67%

My retirement portfolio is a mix of roughly 65% U.S. and 35% Canadian holdings. In order to build my portfolio, I religiously follow the 7 dividend growth investing principles. Last year, I got rid of Wal-Mart (here’s why) and bought Lowe’s. Here’s a recap of my performance from 2016:

Source: Ycharts and Street insiders or annual stock return and dividend growth rate

As you can see, my dividend yield will not make any of you jealous. At 2.67%, we can’t say that I can live on my dividend income… unless I hold $4million ;-). However, when you look closely, you will realize that my portfolio jumped by 11.20% this year (and I’ve been showing a 5 year CAGR in the double digit as well) and that my dividend growth rate for 2016 was 7.41% on average.

I have three companies that didn’t issue a dividend raise in 2016. I must tell you upfront they have been added to my “potential sell watch list” for 2017. However, when you look closely, there are good explanations:

Agrium: the company has entered into a merger of equals agreement with Potash (POT) that will completed in 2017. There is no reason to increase a dividend that will be changed in the upcoming months anyway. We’ll see how the merger goes and I’ll make my decision afterwards.

Gluskin Sheff: this has been a disappointing holding in my portfolio (one of two showing a negative return along with Helmerich & Payne (HP)). The company is having problems increasing its assets under management as competition and volatile markets haven’t helped wealth management firms lately. I keep the hope of a seeing a competitor acquire GS.TO as it is currently trading at a very interesting price.

SNC Lavalin: I did not purchase shares of SNC for its dividend growth potential but rather because it was put in the penalty box for a good reason. The company was sued by the Federal Government. Now that this threat has faded away, the stock has regained momentum. I intend to keep SNC this year and see how the stock goes. However, I might sell it if see that there is not much potential for additional gain. In the meantime, the stock has done very well in 2016.

After reviewing this portfolio, I also realized that Coca-Cola hasn’t been performing much this year. The company struggles to generate growth and the stock has stagnated for the past 3 years. At least, the dividend growth is strong and steady! I have no intentions of selling ;-).

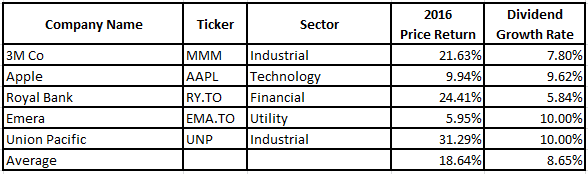

Kid’s Account +20.70% – Yield: 2.55%

At the beginning of 2016, I made an important decision to take over my kid’s account and manage it. For the first 3 years, I had left the responsibility of increasing my children’s tuition fund to a combination of index mutual funds. After three years, I’ve realized that my retirement account was doing a better job than my index funds. This is why I decided to move all my money into my brokerage account.

I was blessed to enter all my money in the stock market while it was at its lowest point of the year (between January and February 2016). You can see that with a +20% return, I did a good job!

Source: Ycharts and Street insiders or annual stock return and dividend growth rate

While the account grew fast, I’m actually more proud of my average dividend growth showing 8.65% for 2016. Each company held in this portfolio shows a strong dividend growth potential for the upcoming years.

I don’t expect any transactions in this account for 2017. In fact, I just can’t wait until I return home so I can start investing more money in this account again! The money is invested in a RESP, a tax-sheltered account created by the Canadian Government giving me an additional 30% in subsidies for the first $2,500 invested per year per child. This means I can put up to $7,500 per year and receive an additional $2,250 to boost my children’s account. I know I will not reach the limit this year, but adding more money to it is one of my 2017 goals.

As you can see, a low dividend yield portfolio isn’t a bad thing in the end. What really matters to me now is to show growth in both portfolio value and dividend income. I hope 2017 will be as good as 2016.

What about you, how was 2016 in your portfolio?