Since I received the commuted value of my pension plan last year, I’ve given lots of thoughts about building a retirement portfolio. In that optic, lots of retirees ask me to write a more detailed approach about a higher yielding portfolio. Since I’ve received lots of demands coming from my Dividend Stocks Rock members to build a “retiree ready” portfolio, I will be launching such portfolio models this month. I thought of detailing my process on this blog to help you understand the difference between my current portfolio showing strong dividend growth and how I would build an income portfolio. But before we start picking stocks, there are three factors to keep in mind at all time. Like the three stooges, they could really crash your retirement party and this won’t be funny.

01 Have you thought of inflation?

When I read about all those amazing 8% yielders on the market ensuring a comfortable and safe retirement to several investors, I always smirk. The first thing I do is looking at the past 5 and 10 years dividend growth rate of those retirees’ best friends. Most of the time, the number I see is ZERO.

Then, many investors tell me: “Mike, I don’t mind if the company “Old Retiree’s Buddy (ticker ORB)” doesn’t increase its payment; the 8% covers the inflation”. Wrong. I know, many of you know exactly what I’m going to explain, but because I’ve received some questions and similar comments, I must take a moment to draw a line in the sand and tell you to cross it.

There is a big difference between the dividend yield and inflation. Imagine you invest $1,000,000 in “ORB” at 8% with no dividend increases. Therefore, year after year, you receive a solid pension of $80,000 per year. Let’s assume you are 60 today and you will live until 85. Your portfolio will pay you $80K/year for the next 25 years.

Now, imagine your $80K budget is subject to a 2% inflation. This means that each year, your budget (utility bills, food, gasoline, household maintenance, health and personal care, restaurants, travel, etc) cost a little bit more. 2% is nothing, right? You won’t even feel it, huh? Let’s see what will happen in your next 25 years:

| Year | Retirement payment | Budget with Inflation | Difference |

| 1 | $80,000.00 | $80,000.00 | $0.00 |

| 2 | $80,000.00 | $81,600.00 | $1,600.00 |

| 3 | $80,000.00 | $83,232.00 | $3,232.00 |

| 4 | $80,000.00 | $84,896.64 | $4,896.64 |

| 5 | $80,000.00 | $86,594.57 | $6,594.57 |

| 6 | $80,000.00 | $88,326.46 | $8,326.46 |

| 7 | $80,000.00 | $90,092.99 | $10,092.99 |

| 8 | $80,000.00 | $91,894.85 | $11,894.85 |

| 9 | $80,000.00 | $93,732.75 | $13,732.75 |

| 10 | $80,000.00 | $95,607.41 | $15,607.41 |

| 11 | $80,000.00 | $97,519.55 | $17,519.55 |

| 12 | $80,000.00 | $99,469.94 | $19,469.94 |

| 13 | $80,000.00 | $101,459.34 | $21,459.34 |

| 14 | $80,000.00 | $103,488.53 | $23,488.53 |

| 15 | $80,000.00 | $105,558.30 | $25,558.30 |

| 16 | $80,000.00 | $107,669.47 | $27,669.47 |

| 17 | $80,000.00 | $109,822.86 | $29,822.86 |

| 18 | $80,000.00 | $112,019.31 | $32,019.31 |

| 19 | $80,000.00 | $114,259.70 | $34,259.70 |

| 20 | $80,000.00 | $116,544.89 | $36,544.89 |

| 21 | $80,000.00 | $118,875.79 | $38,875.79 |

| 22 | $80,000.00 | $121,253.31 | $41,253.31 |

| 23 | $80,000.00 | $123,678.37 | $43,678.37 |

| 24 | $80,000.00 | $126,151.94 | $46,151.94 |

| 25 | $80,000.00 | $128,674.98 | $48,674.98 |

| Total | $562,423.98 |

As you can see, your retiree’s budget starts at $80,000, but ends at $128,674! The last column refers to the amount you must find each year to compensate for the lack of dividend growth. Your portfolio generates $80K, but you spend more year after year. After 25 years, you had to find over half a million just to pay inflation on your lifestyle!

You can replace the budget numbers and the yield by anything, if companies in your portfolio don’t increase their dividend by at least 2% per year, you will be digging your own hole. In fact, spending $80,000 in 25 years from now is like spending $48,762 today. And this is only considering a 2% inflation!

But Mike, the inflation rate has been lower than 2% for the past 10 years

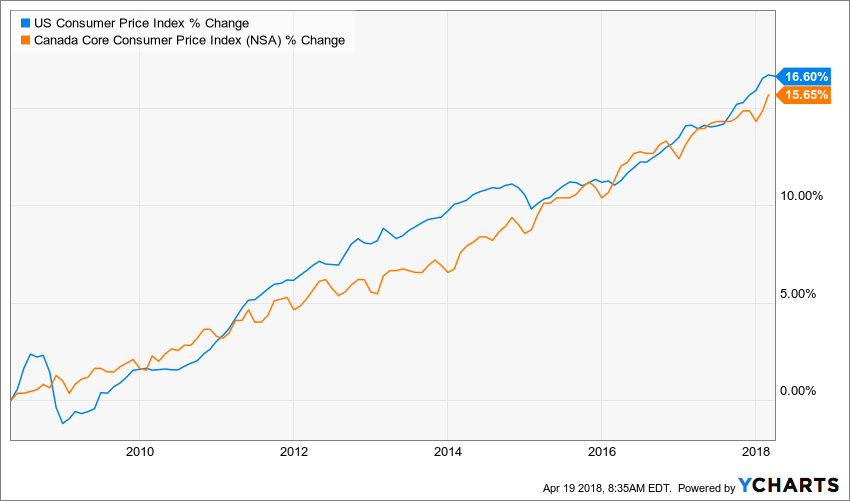

You may argue with me that the inflation rate is a lot lower since the 2008 crash, but we have entered into a low interest rate environment and things have started to magically cost cheaper than ever. You can see that both the US and Canada show a very low inflation rate over the past 10 years:

Source: Ycharts

Then why not use a 1.5% inflation rate as demonstrated in the above graph? The problem with the inflation number is that it’s just a statistic. Your personal inflation rate is probably a lot higher than the one calculated by your country.

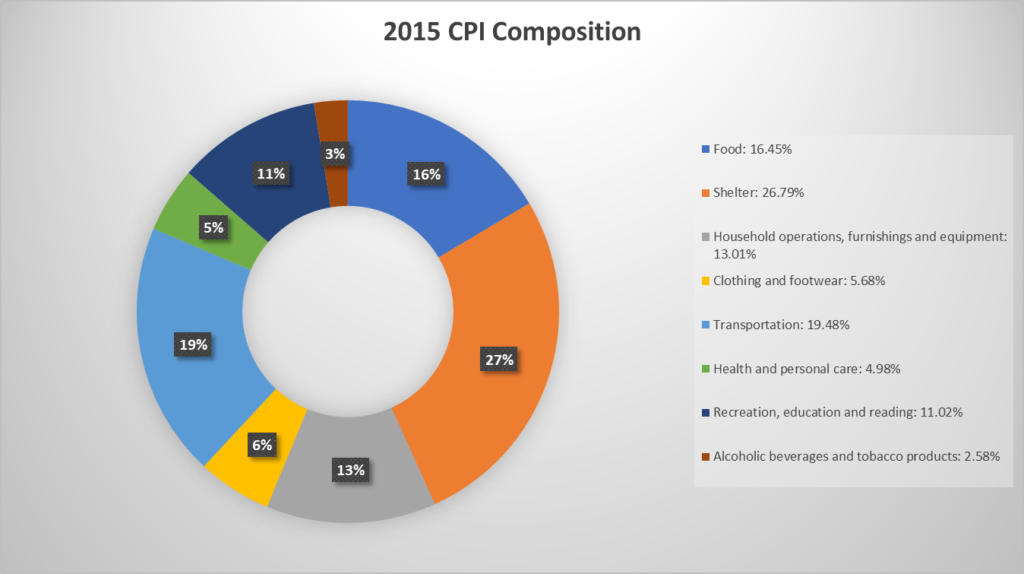

If you have some time, I’d suggest you read the CPI definition of your country to understand. Mine (Canada), can be found here. Here’s how the basket of good was composed in 2015:

Source: Statcan

- Food: 16.45%

- Shelter: 26.79%

- Household operations, furnishings and equipment: 13.01%

- Clothing and footwear: 5.68%

- Transportation: 19.48%

- Health and personal care: 4.98%

- Recreation, education and reading: 11.02%

- Alcoholic beverages and tobacco products: 2.58%

If you compare this pie chart to your budget, I’m sure you will not have 2 similar pie charts. As a retiree, you will most likely spend a lot more money on healthcare than 5% of your budget for example. Therefore, if your healthcare costs rises faster than inflation (hint; this will happen), your own inflation rate will grow faster than 2%. I wasn’t able to find statistic value on how much food inflation increases year after year, but I’m pretty sure it rises a lot faster than 2% according to my grocery bill!

Another problem I see with the CPI is the way some items are calculated. For example, shelter cost calculation could lead to several misunderstandings. Does it take into consideration mortgage payments in a super low interest rate environment? Does it include how housing prices have skyrocketed in major cities such as Toronto over the past decade? While municipal and school taxes may have risen following a small yield, if housing prices jumped, you’d end-up paying a lot more.

Since I’m not a stats guy, I can’t give you answers to those questions. But one thing is certain; the shelter cost calculation is complex and will not likely consider all factors.

In other words; do not take the 1.5%-2% inflation number for granted. If companies in your portfolio don’t increase their dividend year after year, living off your dividend will mean spending less and less year after year. For all those Split Corp fans, I’d suggest you do your calculations.

Final thoughts

Inflation is a retirement serious killer. It lurks inside your budget and hide for a very long time until you realize it’s too late. When you select a high yielding stock, make sure the company has enough room to increase its payout and at least match the inflation. If you are wondering where to start, you can check how I built my “retirement ready” stocks list here.

The post Things That Could Ruin Your Retirement Portfolio Part I appeared first on The Dividend Guy Blog.