A little while ago, I wrote an article on the key metrics for a dividend growth investor. This lengthy article was about each metric I personally use to manage my portfolio and create successful portfolio models at Dividend Stocks Rocks. Following on this article, many readers commented with their thoughts. A topic that was recurrent was that I focus more on the growth aspect of my portfolio (both portfolio value increases and dividend payment increase). On the other side, I am also more open to invest in a low dividend yield stock (read 1-2%) and tend to ignore companies paying around 5% dividend yield.

Most investors agree with my strategy as long as they consider I’m relatively young and that I have plenty of time to let my portfolio yield grow over a long period of time. Retirees often argued that low dividend yield companies weren’t paying enough to support their retirement income needs. However, I respectfully disagree with their strategy of picking high dividend yield to support their income. As I’ve clearly demonstrated in this article about low yield vs high yield, there is a huge risk of seeing your high dividend yield stocks collapse during a recession. But one of my reader got me digging even further. Ron replied that we could find solid companies with higher dividend yield. I will disclose the result of my research in a further article. For now, I wanted to look at another interesting factor for retirees: how much they get in their pockets. This is how I got to run a few hypothesis and work on calculations.

My hypothesis

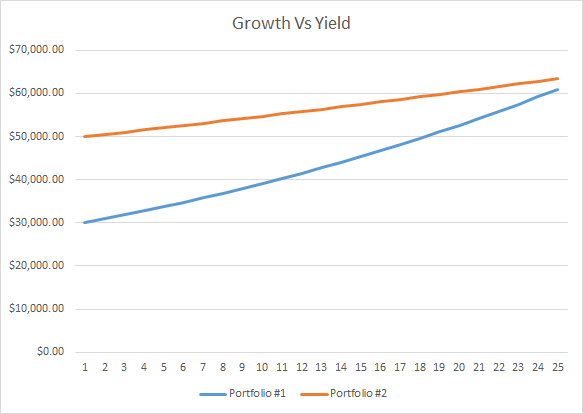

Let’s assume you retire at the age of 65. On average, you will live another 20 years. For the sake of calculation, you have cumulated $1,000,000 for your retirement. In scenario #1, you will invest this money in a dividend growth portfolio paying 3% on average with a dividend growth of 6%. In scenario #2, you will invest the money in a high dividend yield portfolio with an average yield of 5% and a dividend growth of 0%. On the first year, the portfolio #1 generates $30,000 in income and portfolio #2 generates $50,000. Interesting enough, portfolio #1 will need 19 years to generate the same income as portfolio #2:

Source: author’s graph

In the light of this graph, it seems retirees would be better off with a high dividend yield portfolio generating 5% than a dividend growth portfolio. Plus, I must admit I wasn’t very generous with my second portfolio by granting it a 0% dividend growth rate. In the real world, chances are this portfolio would still show some growth over a long period of time. If I only gave a 1% dividend growth rate to portfolio #2, the majority of high yield investors would never be beaten by portfolio #1.

Source: author’s graph

Further considerations

In the light of those calculations, it seems that income seeking investors that have less than 20 years in front of us are better off choosing high yielding stocks to build their portfolio. To be honest, I was a bit surprised by this conclusion. But if you stop your analysis with pure numbers geared toward to income generation, this is a correct assessment.

However, I think further consideration must be made. First, unless you wish to leave all your savings to your heirs, you can also withdraw money from your nest egg on top of cashing your dividend payment. The ideal scenario would be that you generate a lot more than what you need solely through dividend payment, but this is rarely the case. Second, when a company pays a higher yield, it is usually because it is seen that this investment involves additional risks. Therefore, your investment return might be mediocre. This is actually what I demonstrated previously with this article. Finally, inflation could play a very important factor for retirees. If you have built a high yielding portfolio with limited growth, chances are inflation will eat your buying power slowly but surely. A portfolio showing an average dividend growth of 6% will never actually generate a growing buying power over time.

Conclusion

What I like about investing is there is never one and single truth. While writing this article, I realized it wasn’t the end of the world to pick high dividend yield to finance one’s retirement income. I still prefer the dividend growth approach, but I can see how bigger dividend payments could appeal a specific categories of investors. However, as you will see in my next article about this topic, finding those strong high dividend yield companies is far from being easy!