Back in August, I wrote an article about why I think we are entering a new bull market. One of my premises was the fact that the US economy is holding steady and will continue to grow. The unemployment rate remains low, gasoline prices remain relatively low encouraging consumers to buy more and companies are benefiting from very low interest rates. The American Consumer is the key to the U.S. economy and also the key for global growth at the moment. If people have jobs, money in their bank accounts and easy access to additional credit, one sector that will benefit from this combination of factors is the consumer cyclical industry. I’ve pulled out 4 companies from this sector (2 U.S. and 2 Canadian) that should continue to reward investors through higher dividend payments and considerable stock appreciation in the upcoming years.

HASBRO (HAS)

Source: Ycharts

Hasbro is one of my best find of 2013 when I built my DSR portfolios. The company is rarely often mentioned by dividend investors as it is far from being a “classic holding”. However, the company has built a strong business model and is set to reap the benefit from various forms.

Like Mattel, Hasbro has known lots of success with its “classic” toys such as Playskool, Tonka, Milton Bradley and Parker Brothers board games. While the classic toys industry is slowing down as kids are definitely more interested in playing with their tablets than playing with “real” toys, Hasbro has been able to show sustainable growth. The company benefits from a strong cash flow base from its classics and has also developed a unique expertise in another toy sub-sectors.

Over the past decade or so, many blockbuster movies have come from the Super Hero industry. This type of movie are perfect for selling toys. They show several figurines and other derivative possibilities and they are usually produced with sequels. Hasbro has positioned itself as the most effective franchise toy manufacturer. Strong from their success with Marvel Superheroes and Transformers movies, HAS has signed lucrative licencing products with Disney for Frozen and Star Wars movies. There is a strong interest in these movies and many children will want their Olaf and BB8 for Christmas.

With the impressive list of Super Heroes, Star Wars and other Disney movies coming out over the next three years, I wouldn’t be surprise to see HAS stock soaring again in the near future.

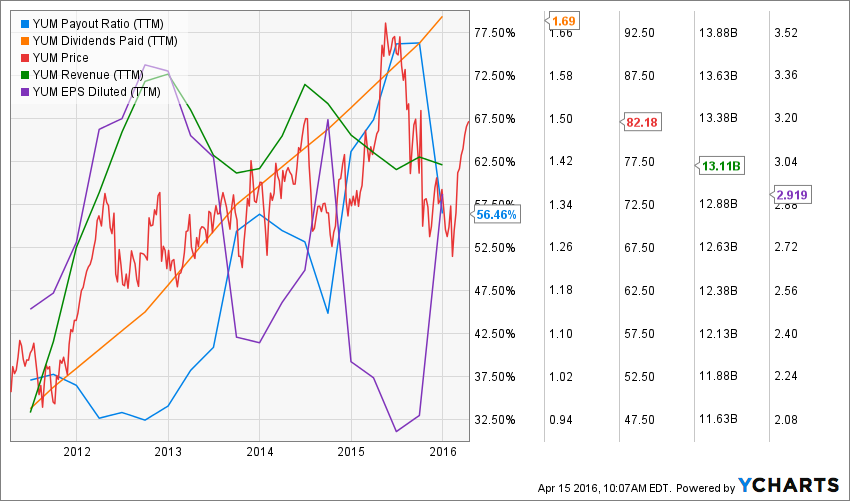

YUM BRANDS (YUM)

Source: Ycharts

YUM! Shows an impressive number of restaurants spread among three distinct brands. The business is the global leader in chicken, pizza and Mexican style restaurants in terms of number of restaurants. This gives it a unique economic moat that is very hard to cross. The new YUM! Business model will be solely based on a franchise model which enables predictable and continuously increasing cash flow generation.

After spinning off their Chinese restaurants, YUM will continue to earn royalties from a fast growing segment of its business without having to face several risks. In other words, YUM has successfully created a cash flow making machine in China is it is about to reap the benefits for several years to come. The Chinese market is poised for a strong growth in the upcoming years as many more people will go to restaurants.

At the same time, YUM continues to operate their stable and predictable side of business in the U.S. As consumers have more money in their pockets, they are more likely to go eat at restaurants. The restaurant chain companies must remain cautious about the recent healthy trend we have noticed in North America. It is very possible its long term growth will slow down due to more health conscious clients. However, they have plenty of time and cash flow to adapt their menu to this new reality.

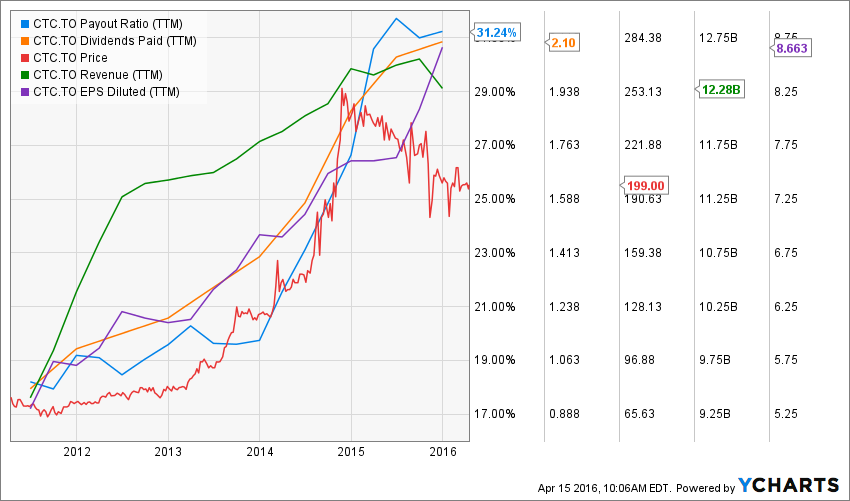

CANADIAN TIRE (CTC.TO)

Source: Ycharts

Canadian Tire is not your classic dividend holding either. With a very low yield, it will fly under the radar of many investors. However, this company shows very interesting characteristics that should not be ignored. CTC is one of the largest retailers in Canada. Canadian Tire’s primary retail business categories include: Automotive, Living, Home improvement, Sports, Playing and Apparel. The company also has a Financial Services division, which offers products and services such as credit cards, retail deposits, and insurance.

CTC has decided to concentrate on their strong business model by spinning off their real-estate segment into CTR and selling half of their financial services to ScotiaBank (BNS). Management can now focus on continuing to build its strong brand and attracting clients with their aggressive marketing campaigns. Canadians are emotionally attached to Canadian Tire and their weekly strong rebates on specific articles keep customers coming in on a regular basis.

The recent oil price drop has hurt CTC perspectives and its stock price has taken a hit. However, the Canadian economy has proven more resilient than anticipated and as the oil industry is recovering, CTC seems to be in a very good position to open its doors to its returning customers. There seems to be a very interesting entry point at the moment and the dividend payment will continue to increase in the upcoming years.

MAGNA INTERNATIONAL (MG.TO)

Source: Ycharts

The last consumer cyclical chosen for this short list is Magna International (MG.TO). Once again, this is a low yield company but showing impressive numbers. Considering their very low payout ratio and strong earnings growth trend, you can expect some generous dividend increases in the future.

Magna is not only an international automobile part supplier, it also designs, develops, manufactures, assembles and engineers automobile parts. Magna sells to OEMs (original equipment manufacturers) across 26 countries. It offers a wide variety of 86 products that go from seating to roofing systems.

Being a leader in their industry, MG has built a very strong and reliable relationships with car automakers. GM, Ford and other car giants are more inclined to deal with well established companies when it’s time to order parts. MG offer them a wide variety of products and a proven quality. Many competitors can’t reach MG’s product offering at the moment opening doors for additional growth.

Consider 50% of MG’s revenues come from Detroit automakers and the fact that many car owners are due to change their car in the upcoming years, Magna is sitting in a very comfortable seat.

Other Consumer Cyclical Dividend Stocks?

All right, it’s now your time to tell me about your favorite consumer cyclical stocks. I’ll be happy to add your suggestion to my short list ;-).

Disclaimer: I hold HAS in my Dividend Stocks Rock Portfolios.