Nope, this is not some kind of fake post to push my service down your throat. It is a real article discussing why you should or should not pay for investment services. You already know that I have a membership service and that I might be biased about this topic. But I don’t think I am. I’ve worked in the financial industry for 13 years and advised clients as a financial planner for 8 years. During all those years, I’ve had an ongoing discussion with my best friend about investment fees. His thesis was quite simple:

Mike, why on earth should you pay someone else to manage your money? You can easily open an online brokerage account within minutes. Then, you buy a bunch of ETFs and you rebalance each year. That’s called the coach potato strategy. You pay minimal fees (below 0.50%) and you get the market’s return each year. What else there is to tell?

The Mechanic Analogy

When you explain it the way my friend did, it makes little sense to pay 2% fees on a mutual fund. I agree on that part. However, the problem is that we look at this situation from the inside. We both graduated with a bachelor degree in finance and we both work in this industry. It’s like a mechanic telling you that you should change your oil yourself. After all, all you need is new oil, a filter, and a jack. Within minutes, your oil is changed and you just saved $50+. Do you think I change my own oil? Hell no! I pay someone else to do it because I know nothing about cars and I have no interest in learning. If I start playing around with my car’s mechanics, chances are I will do more damage than good. Do you think my friend does his own oil changes? Nah!

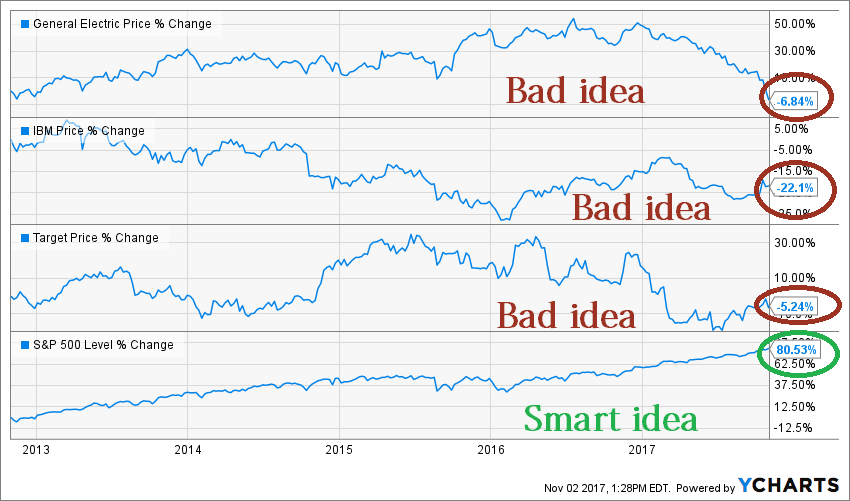

The very first reason why you should pay for investment services is when you know very little about investing and have little to no interest in learning. What is best? Paying $2,000 in fees on your $100K that will be invested in a balanced mutual fund or investing most of your money in “blue chips” like IBM, GE and Target?

Source: Ycharts

As you can see, investing is a little bit more than picking companies that “are too big to fail”… the Blue Chips don’t exist anymore.

But What About ETFs Investing?

It is true that any newbie could have read one or two ETF investing books and built a portfolio with 4-5 ETFs including Canadian and U.S. markets, emerging markets, and bonds. In fact, this strategy works for many DIY investors. After all, they balance their portfolio in a good way, they avoid paying high fees and this kind of strategy requires minimum follow-up (besides rebalancing your portfolio every 6 or 12 months).

If you are a disciplined investor and you do not wish to pick stocks, the coach potato approach could work very well and you won’t have to pay for investment services. The problem is that most people are NOT disciplined investors. They tend to panic when the market is volatile and they want to find the next Facebook (FB) when the market is very bullish. There are lots of events that could lead an investor to get out of his strategy to “explore other opportunities”. Unfortunately, the best way to fail at investing is to not follow your core strategy. Some investors should pay services simply to keep them in line with their strategy…

But Mike, there is so many free resources on the internet, why would one pay for such investment services?

Most readers of this blog aren’t subscribers to my service. When I combine both readers from The Dividend Guy Blog and the Dividend Monk, I have close to 13,000 subscribers to my free newsletter. This can tell you about the potential of investors interested in reading about this topic. However, they are not willing to pay a dime to get that information. I can’t blame you as I think you don’t have enough time in 24 hours to read, digest, and act on all investing articles that are published on the internet each day.

Or maybe you should pay for a service because there is too much free information. Last morning for example, I think I lost a good 2 hours reading about Shopify (SHOP). After Citron Research published a bearish (to be polite) thesis in October, I was wondering about the company. Then, instead of following my own investing process, I jumped from one article to another video to end-up reading and watching a dozen of them. Each article had a good point making a bullish or bearish (or simply hammering another’s investor thesis case. What’s the result of my 2 hours research? Nothing. Instead of spending this 2 hours using my own methodology and getting a real idea about SHOP, I was just entertained by various authors. The reason why I didn’t use my process is mainly because SHOP is a pure techno (no dividend paying) stock.

On the other side, if I had been a member of a techno investing site, I would have start my investment research reading the investment thesis of someone I know and I trust from previous experiences. Then, I would have known where to look next to validate this thesis and finally take action. In this case, it would have been worth it to pay for such information service.

You should not pay for services, you should invest in them

In the end, the reason why someone should pay for an investment service is when it becomes an investment. Paying $1,000 annually in investing newsletters that you read and archive isn’t worth it. What makes sense is investing your money into an actionable investment service where you will make trades and benefit from someone else’s knowledge and experience. Try to look for a service that matches your investing strategy and beliefs. Then, you will benefit from a second opinion on your thesis that will worth a lot more than the price you are paying.