The financial sector is both exciting and scary for investors. On the one hand, you have solid banks which are the heart of our capitalist system. They are a sign of trust, stability and growth. On the other hand, you think about all the exotic financial strategies like mortgage-backed securities, options and swaps. You realize that even those who manufactured those products don’t always understand the complex monster they created.

To simplify things a little, you can divide financials into three distinct sub-sectors:

Asset managers: companies that are managing/investing money for others. Mutual funds, hedge funds, real asset managers, and ETF managers are part of this group. Asset managers usually perform consistently with the overall market. It is very rare to see an asset manager’s stock price increase during a bear market.

Banks: you can sub-divide this group into global and regional banks. You can also look at investment banking, commercial banking, or the credit side as individual industries. In the end, it all comes down to deposits and loans. This group benefits from higher interest rates as the spread between loan rates and deposit rates will often play to their advantage.

Insurance: this last financial segment includes life, property & casualty, reinsurance, specialty, and brokers. Insurance companies require strong asset management skills to align their revenues with potential claims costs. It is also easier for them to manage their assets during higher interest rate periods.

Sub-Sectors (Industries)

Greatest Strengths

Financials represent a true investing opportunity for dividend investors. There are many strong banks, financial firms and insurance companies sharing the wealth with their shareholders. Just remember not to fall for a strategy you don’t fully understand.

Assets managers will do very well during bull market. There is also an interesting shift from mutual funds toward ETF products. Leaders in ETFs or financial advisory services will lead this industry going forward.

Second, I must admit Canadian banks are unique. The Big Six operate an oligopoly that is not only highly regulated but also is protected by the Canadian Government. In other words, they can use their core business in Canada to generate significant cash flows and use this money to grow outside those boundaries. This is how they can pay a yield around 4% and still show a 5% to 8% annualized dividend growth rate over decades. Dividends growth policies are paused due to the pandemic but will resume shortly after once this is under control.

Finally, I’m not a big fan of the insurance industries. I find them too dependant on external factors (catastrophes, interest rates, etc.). This is an industry I would rather ignore in my portfolio and focus on my strength which is strong knowledge of the banking industry having been a private banker in my past.

Greatest Weaknesses

I think 2008 showed us how financial services could go from “too big to fail” to “the largest bankruptcy in history”. Most companies in this sector will seek to inspire trust. Unfortunately, trust sometimes turns into blind faith. Be a better investor and research each company thoroughly.

In general, interest rates and the equity markets will dictate if this sector will do well or not. When interest rates are low, regional banks will see their interest rate spread (the difference between what they pay in interest for deposit and how much they make on loans) shrink. In other words, their margin gets thinner. Insurance companies also have a similar problem. Since they must invest premium payments in a way to make more money to cover future claims and generate a profit, having an entire asset class (bonds) offering mediocre returns isn’t helping.

When the market goes sideways, we’ll see many asset managers having a hard time. If you wonder why the market is so volatile for the past 15 years, this is partially because of hedge funds and options and other “wild” trading strategies. As institutional investors can short positions or enter in massive positions through options, they could also get into big problems. Margin calls happen when the market drops suddenly, and fund managers don’t have enough liquidity to cover the minimum value. They are then forced to sell, pushing the market toward new bottoms.

How to Get the Best of It

First, understand your investment. Financial businesses often generate revenues from complex strategies. If you don’t understand how a life insurance company makes money (and how it must protect its premiums), then move along and look for another sector where you understand the business.

When there is a market panic, Canadian banks are likely going to get hit and will offer you the most reliable dividends in this industry. Going after leaders that have a diversified business model is better than a one-trick pony. Most leaders will enjoy unrivaled economies of scale that is almost impossible to compete with. BlackRock (ETFs) and Visa & Mastercard (payment networks) show such competitive advantages. You can also select among special dividend payers such as Lazard (LAZ) and the CME Group (CME).

Favorite Picks

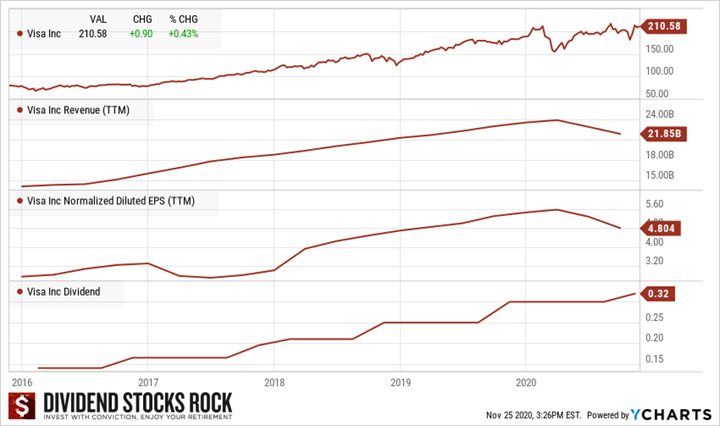

Visa (V)

- Market cap: 460B

- Yield: 0.60%

Business Model

Visa isn’t a financial company, it’s a tech stock. V is the most efficient networker in the most important network there is: money. As explained to a 12-year-old, Visa’s job is to make sure money is going from your wallet to someone else without you picking a single penny from your wallet. Visa dominates the electronic payment market with about half of the total market. The company has over 3 billion cards being used across the world with over 44 million merchants. Its systems are capable of processing over 65,000 transactions per second.

Investment Thesis

The Visa IPO was just prior to the 2008 market crash. V offered a unique opportunity to investors as its stock traded around $11 in the middle of that financial storm. Today, the stock’s price is around $200/share and it will continue to rise for at least another decade. The magic behind V is all about building the widest and most secure network to transfer money from one place to another. The company is a crucial partner with major financial institutions across the world. Everybody pays a commission for each transaction. As there is a clear trend toward electronic payments, Visa has already built its network to enjoy this strong tailwind. Visa is the largest player in an industry where size matters. Its ability to follow (and create) trends in money transfer will be crucial going forward.

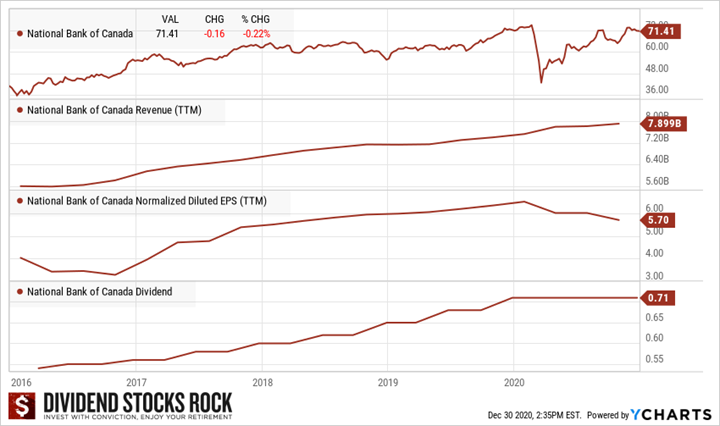

National Bank of Canada (NA.TO) (NTIOF)

- Market cap: 28B

- Yield: 3.40%

Business Model

National Bank of Canada is the sixth-largest Canadian bank. The bank offers integrated financial services, primarily in the province of Quebec as well as the city of Toronto. Operational segments include personal and commercial banking, wealth management, and a financial markets group. NA’s smaller size is currently paying off as the bank was quicker to develop a strong brand in Wealth Management with Private Banking 1859 and they built a highly profitable Financial Markets division.

Investment Thesis

NA has aimed at capital markets and wealth management to support its growth. Private Banking 1859 has become a serious player in that area. The bank even opened private banking branches only in Western Canada to capture additional growth in that market. Since NA is heavily concentrated in Quebec, it concluded deals to do credit for investing and insurance firms under the Power Corp. (POW). Branches are currently going through a major transformation with new concepts and enhanced technology to serve customers. While waiting for the results, it seems wise to invest in digital features to reach out to the millennials and improve efficiency. The stock has outperformed the Big 5 for the past decade as it showed strong results. Recently, NA is seeking additional growth vectors by investing in emerging markets such as Cambodia (ABA bank) and in the U.S. through Credigy. Can it have more success than BNS on international grounds?

I recently reviewed Canadian banks’ last quarter on my YouTube channel. You can watch the review about National Bank below.

Disclaimer: I am long V and NA.TO.

The post Financial Services Sector: Both Exciting and Scary for Investors appeared first on The Dividend Guy Blog.