I’ve decided to discuss Brookfield Property Partners today, mostly because I have received a bunch of questions in regards to their tender share buyback offer. On top of that, they released their quarterly earnings not so long ago.

As the offer expires in a couple days (August 28th), let’s dig into the company!

Business Model

Brookfield Property Partners LP (BPY/BPYU/BPY.UN.TO) owns, operates, and invests in commercial properties in North America, Europe, Australia, and Brazil. The company focuses on being a leading global owner and operator of real estate, providing investors with diversified exposure to some of the most iconic properties. The company also acquires high-quality assets at a discount to replacement cost or intrinsic value. Its operating segment includes Core Office, Core Retail, LP Investments, and Corporate Segments. The company operates in various sectors such as the office sector, retail sector, industrial, multifamily, hospitality, triple net lease, and the corporate sector.

Investment Thesis

The company is backed by one of the world’s largest alternative asset managers (Brookfield Assets Management BAM) and has proven its ability to generate growth. BAM has recently jumped in to reassure investors and announce a $1B share buyback program. On March 20th, BPY issued a letter to shareholders with the following comments: BPY’s Core Office portfolio is 93% leased on a long-term basis (average remaining time of 9 years) with high-quality tenants. It also explained that it has no short-term liquidity problems with $6B in an unused line of credit available for their use. BPY will keep its prime locations and quality buildings as it remains a key element for current and future tenants.

Potential Risks

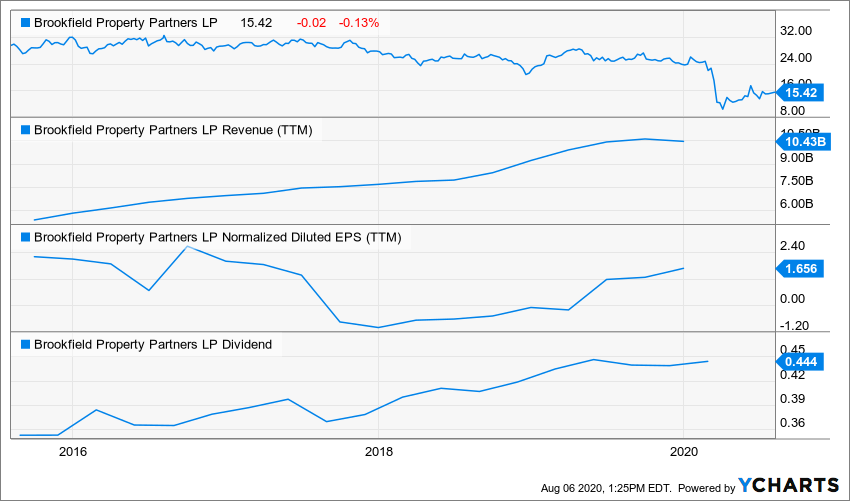

BPY excels in finding undervalued assets and integrating them in its portfolio. The problem is that, to ensure future growth, BPY’s debt is rising year after year. Between 2014 and mid-2018, its long-term debt doubled from $20B to $40B. This one is tricky as the market clearly prices BPY for a dividend cut. While the office portfolio remains solid, retail tenants are already causing problems. The company had to manage several bankruptcies in 2019 and we can expect even more in 2020. The company recently completed the purchase of Forever 21 which declared bankruptcy not too long ago. Future projects may have to be put on hold and growth may be limited for a while.

Dividend Growth Perspective

The company has built a great business model based on both growth by acquisitions and organic growth (2-3%). This ensures FFO grows fasters than dividends. Considering the impact of COVID-19 on the economy (especially on offices occupation and retail sales), the dividend safety is unsure (rated as a 2 on Dividend Stocks Rock). BPY remains a risky play, but their high-quality assets will remain. Please consider dividend payments are paid in USD.

What’s the Story?

If you are looking for a bumpy ride, hop on this train! Once again, I can’t stress enough the speculative aspect of this play. I expect Brookfield Property to cut its dividend at some point. If you hold shares of BPY already, you already received an offer from Brookfield to sell it at $12US or ~$15CAD this month. In fact, Brookfield is buying back almost $1B worth of its shares.

BPY is offering you 12 bucks US or roughly 15 bucks Canadian to buy back your shares. Should you say yes? Or should you keep your shares and ride it all along?

Actually, this is a strong move showing confidence in their future, but it also reduces dividend payments going forward.

So, let’s review the latest quarter.

Last Quarter: -32.9% ytd.

Company FFO (CFFO) was $178M for the quarter ended June 30, 2020, compared to $335M in the prior-year period. The CFFO decrease was mainly due to widespread closures of its hospitality and retail assets due to lockdowns put in place to slow the spread of COVID-19. Rent collections went well for the office portfolio but was at 34% for the retail portfolio. BPY maintained its dividend and ended the quarter with $6B of group-wide liquidity, including $1.5B of cash on hand, $2.8B of corporate and subsidiary credit facilities and $1.7B of undrawn construction facilities. The company bought 2,641,196 of BPY units at an average price of $8.45(USD) per unit during the quarter.

(You can watch more of my videos on YouTube)

Why I Keep My Shares!

You have a company that has assets all across the world. Mostly in the US, but still 14 billion in Asia Pacific, 31 in Europe, 9 billion in Canada. Funny fact, this is a Canadian-based company, parent from Brook Hill Asset Management. They manage almost $200 billion of assets across 30 offices, so we’re talking about some major business.

BPY dropped in value greatly a few months ago with the COVID-19, which is when I bought my shares. As you can imagine, there’s a lot of risk involved because a big portion of their assets are retail. When you think about the brick and mortar, it’s not doing super good: we have lots of bankruptcies in the past few years, and it gets even worse when they are forced to close down.

However, the company is backed by Brookfield Asset Management, they have over 40 billions in liquidity, and they have made clear that they’re gonna keep generating some. Also, most of the dividend paid by Brookfield Property Partner is actually paid to Brookfield Asset Management, so in the end, when you’re buying shares of BPY, you’re pretty much getting in line with Brookfield Asset Management at the same time.

What I really like about BPY is that they own premium assets. Retailers will come and go. The economy is going to go up and down, but one thing that will stay is premium location. There’s nothing else more important than location in REITs.

For new projects, they’re literrally building small villages. You have offices, the office towers, multi-family and then retail… all around the same blocks! It creates a small ecosystem. Everybody is working there, living there, and at the same time buying stuff from retailers nearby.

It is obviously a speculative play, the stock is priced, and no dividend cut happened yet.

So I’m holding my shares as I’m convinced the play will pay off eventually.

What’s your take on this one?

The post Brookfield Property Partners (BPY): Should Your Shares Be Running This Bumpy Ride? appeared first on The Dividend Guy Blog.