Four steps to reduce risk in your portfolio ahead of whatever happens next, and to keep investing confidently even with the current high market. Yes, the market is high, almost the highest in the last 34 years except during the tech bubble in 2000.

The Shiller CAPE ratio compares market earnings over time. It shows that the overall market is trading at nearly 31 times earnings. In other words, the entire market’s P/E ratio is 31. That’s expensive, and rattles a lot of investors.

Never miss anything! Subscribe to our weekly newsletter here.

What do we fear?

We fear what could happen next. A market correction around 10% isn’t that bad; it doesn’t take too long to bounce back. Market crashes, sharp drops of 20% or more, are more serious.

Retirees and those near retirement worry about suffering a big loss. Those still investing money are afraid of investing just before a crash happens, and often wait on the sidelines.

Retirees and those near retirement worry about suffering a big loss. Those still investing money are afraid of investing just before a crash happens, and often wait on the sidelines.

Recognize yourself? Luckily, there are things you can do to ensure your portfolio is ready to weather the storm and to keep investing with confidence. After all, none of us know if, when, or by how much the market will crash; holding on to your money rather than investing it could cost you. Here are four steps to reduce risk and anxiety.

1 – Beyond the stock price…

You might be wondering whether some of your holdings are overpriced and at risk of crashing along with the market. You might also hesitate to invest more and paying too much. While some stocks are overpriced, others aren’t despite their high prices. If a company increases its earnings year-over-year, it’s normal that its stock price increases also.

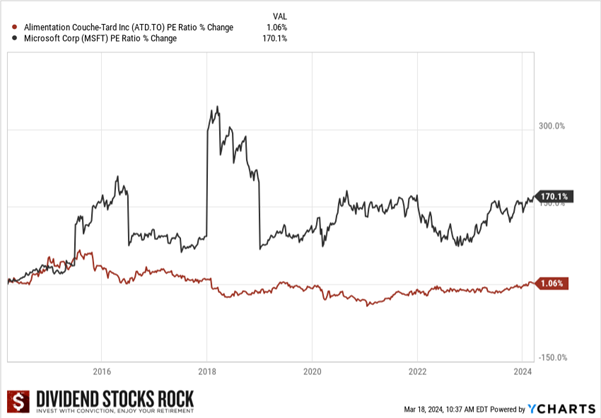

The graph below shows the variation in the price-to-earning (P/E) ratio for Alimentation Couche-Tard (ATD.TO) and Microsoft (MSFT) over the last 10 years.

Over that period, ATD.TO’s price has gone from $14 to $80, but its P/E ratio has been pretty stable. In short, as the share price was rising, so were the earnings. To buy shares today, we’d pay almost the same multiple of ATD’s earnings as ten years ago. We can’t just look at the price to determine if a stock is overvalued.

Clarify valuation with these comparisons

What I do is compare the 5-year average P/E ratio against the Fwd P/E ratio, and the 5-year average dividend yield against the Fwd yield. For ATD.TO:

Average P/E ratio = 16.7 slightly below Fwd P/E = 18.15.

We’re paying a bit more now than the 5-year average, but not much when considering the stock’s 22.4% annualized dividend growth over five years, low payout ratio, etc.

Average yield = 0.9% slightly higher Fwd yield = 0.7%,

This also indicates a small premium on the current stock price, but again, not much.

In the graph, we see that Microsoft’s P/E ratio grew 170% over 10 years. Overpriced? Not so fast. Due to cloud computing and AI, the market expects MSFT’s growth to continue and is willing to pay a premium for the stock. Of course, the market could be wrong. If MSFT fails to continue growing at its current pace, its stock price could easily drop 10%.

Comparing MSFT’s Fwd P/E ratio and Fwd yield with their respective 5-yr average shows results similar to ATD’s—a slight increase in valuation vs. five years ago. The bulk of the 170% P/E ratio increase was driven by a high valuation in the five years of that period when MSFT wasn’t yet benefiting from cloud computing and AI.

A Fwd P/E ratio much higher than the 5-year average, and a Fwd yield much lower than the 5-year average, can indicate an overpriced stock, or not. In such a scenario, I’d try to find out why the market is valuing the stock so high.

Never miss anything! Subscribe to our weekly newsletter here.

2 – Measure your exposure to risk

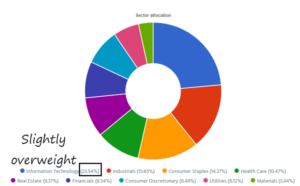

Having a suitable exposure to risk is essential to protect your nest egg. That means diversifying across sectors and having appropriate weight for individual stocks.

Sector allocation

Ensure you have holdings in several sectors and not too much of your portfolio in a single sector. Having 45% invested in a single sector overexposes you to the risks the sector faces. If that sector crashes, 45% of your portfolio will drop.

I usually limit my exposure to a single sector to 20% for my favorite sectors and up to 10% for other sectors. Retired or nearly retired investors might tailor their sector allocation to favor stable and income-producing sectors while keeping a smaller portion of their money in growth sectors.

I usually limit my exposure to a single sector to 20% for my favorite sectors and up to 10% for other sectors. Retired or nearly retired investors might tailor their sector allocation to favor stable and income-producing sectors while keeping a smaller portion of their money in growth sectors.

See How Sectors and Industries Guide Investors.

Stock weight

How much are you willing to lose on a single stock in your portfolio…2%, 3%, 5% of your portfolio’s value?

Once you’ve answered that, look at your largest positions and their weight in your portfolio. During the worst market crashes in the last 40+ years, the market lost roughly 50% of its value before stabilizing and beginning to recover.

For example, let’s say you can tolerate a loss of 5% of your portfolio. If you have a $1M portfolio, you’re okay with losing $50,000 on a single stock. If that loss is from a 50% crash, the maximum amount for this position is $100,000.

If you have a holding worth over $100,000, it’s time to trim that holding. Sell some shares to decrease your exposure and reallocate the funds elsewhere to spread your risk.

3 – Focus on quality

Ensure your holdings are quality stocks. It’s alright to hold on to quality stocks even if a market crash drags them down tomorrow. They’ll bounce back faster than poor-quality holdings and reward you.

A quality holding shows:

A very strong dividend triangle, with a consistent growth trend for revenues, earnings, and dividends.

A very strong dividend triangle, with a consistent growth trend for revenues, earnings, and dividends.- An investment thesis that explains how the company will be able to keep increasing its revenue and earnings over the next 5, 10, or 20 years, e.g., growth vectors, sticky business models, predictable cash flow, etc.

When you’re worried about a crash, it’s not the time to take wild guesses on holdings you’re unsure of. If you’re keeping stocks hoping that they’ll bounce back, but you don’t have a clear investment thesis for them, consider getting rid of them, or at least some of them.

4 – Dividend safety first

In a market crisis, many companies cut their dividend. Assess the dividend safety of your holdings and ensure your dividend income is diversified.

To assess dividend safety:

To assess dividend safety:

- Look for low to moderate payout ratios that indicate the companies make more profit than what they pay out in dividends. See Using Payout Ratios Wisely.

- Look for a trend of dividend growth over several years.

When you see a high yield, no dividend growth or slowing dividend growth, a high payout ratio, and a weak dividend triangle, you can expect a dividend cut.

Diversification of your dividend income across several holdings makes it less painful if one of your holdings cuts its dividend. Ensure you don’t depend on one or two companies for 25% of your dividend income, especially if you’re retired or near retirement.

Make sure your dividend income comes from companies in different sectors or industries. In other words, don’t invest in 10 REITs, or 6 Canadian banks; throw in some utilities, consumer staples, telcos, etc.

Using these four steps to reduce risk will help you sleep well at night, whatever happens on the market.

Waiting on the sidelines?

You have money to invest but you’re waiting for the “imminent” market crash?

We never know when a market crash will happen and when it does happen, we don’t know when we’ve hit rock bottom. You could end up waiting a long time, all the while missing out on dividend payments.

If you’re worried about investing at peak prices the day before the worst crash in a decade, plan to invest at intervals, e.g., monthly, quarterly, to minimize that risk. Learn more about this in How to invest lump sum. Using these four steps to reduce risk and also to invest new money wisely, at any time!

The post 4 Steps to Reduce Risk in a Near All-Time-High Market appeared first on The Dividend Guy Blog.