This is a guest contribution by Josh Arnold with Sure Dividend.

Investors in dividend stocks are interested not only in the safety of the payout and growth potential, but current yield as well. This is particularly important for investors that rely upon the income generated from their dividend stocks for living expenses. To that end, high-yield dividend stocks are favorites among income investors for obvious reasons.

However, not all high-yield dividend stocks are created equal. There are varying levels of dividend safety, growth potential, and current yield that paint a very different picture for some stocks compared to others.

In this article, we’ll take a look at three of our favorite high-yield stocks.

Source: Pixabay

#3: WestRock Co. (WRK)

WestRock is a leading provider of paper and packaging solutions to a wide and deep base of customers globally. It was formed in 2015 when Rock-Tenn and Mead-Westvaco merged, creating a company with a nearly $10 market capitalization that has performed well in what is a boring, but profitable, industry.

Today, the company gets just over half of its revenue from the corrugated packaging segment and the balance from consumer packaging business. However, most of its profits come from the corrugated segment.

The company’s late April Q2 results showed strong revenue growth, adding 15% year-over-year. This growth was primarily attributable to the acquisition of KapStone that occurred late last year. In addition, price increases helped boost the top line. However, cost inflation crimped margins, causing adjusted earnings-per-share to fall 3.6%, declining from 83 cents to 80 cents year-over-year.

We see forward growth at 4% annually as over supply in the containerboard market is more than offset by pricing increases and the global push to rid the world of one-time use plastic containers.

Source: Investor presentation, page 6

WestRock is well-positioned to capitalize on this long-term trend as it has been pushing paper containers for a variety of containers, and we see this as a long-term tailwind for earnings growth.

The current payout of $1.82 annually is good for a 4.9% current yield. The dividend has increased at high single digit rates since 2016, but we expect that growth rate will slow slightly in the coming years. Still, WestRock’s current yield at nearly 5% is quite attractive, and even if the dividend growth rate slows, WestRock will be an attractive dividend stock for a long time to come.

In addition to a strong yield, WestRock offers a compelling valuation. The stock trades for just over 9 times our estimate for earnings-per-share this year, which compares very favorably to our estimate of fair value at 12.5 times earnings. That should provide a very nice mid-single digit tailwind to investors from a rising price-to-earnings ratio in the coming years.

In total, we expect 15%+ annual returns for WestRock from the combination of earnings growth, the very high current yield, and a rising valuation.

#2: AT&T (T)

AT&T traces its roots to Alexander Graham Bell in the 1870s, and the current form of the company is the result of the former SBC acquiring AT&T in 2005, and changing its name. Today, the company is the largest communications company in the world, operating a diversified model that includes wireless service, WarnerMedia, advertising, broadband, video, and other services globally. The stock boasts a $246 billion market capitalization.

The company’s Q1 results from late April showed a 17.8% gain in revenue year-over-year, primarily driven by the company’s WarnerMedia segment. However, wireless service revenue was offset by declines in other segments, so without the growth from WarnerMedia, revenue would have fallen fractionally.

Adjusted earnings-per-share rose slightly, adding a penny from 85 cents to 86 cents against the year-ago period. We expect AT&T to produce $3.60 in earnings-per-share this year, which would represent a low single digit gain against last year.

AT&T has struggled to grow earnings-per-share in the past, the combination of a rising share count and slowing growth in its legacy businesses. The company’s additions in the past few years of DirecTV, Time Warner, and others has helped build the pipeline for future growth, but thus far, declines in the legacy businesses are partially offsetting that growth. To that end, we see ~3% annual growth from AT&T in the coming years as its wireless business is performing relatively well, but broadband and hardline phone service struggle.

AT&T’s most attractive trait as an investment, however, is not its growth potential, but its yield. The current $2.04 payout is good for a 6% yield on the stock, which is enormous compared to most common stocks, and three times that of the US 10-year Treasury. AT&T has always boasted a strong yield but the current low valuation of the stock has the yield in a much better spot than it normally is. Growth in the payout will be in the low single digits for the foreseeable future, so AT&T is not a dividend growth story. However, if offers a REIT-like yield with some upside potential.

In addition, AT&T is cheap. The stock trades for just over 9 times this year’s earnings against our estimate of fair value at 12 times earnings. That should provide a nice tailwind to investors in the coming years as the valuation reverts back towards its historical norms.

Putting this together means AT&T offers investors ~15% total annual returns in the coming years, with nearly half of that coming from the outstanding current yield. We like AT&T very much for its high yield and long-term dividend prospects.

#1 – Tanger Factory Outlet Centers (SKT)

Tanger Factory Outlet Centers is one of the largest owners and operators of outlet centers in the US and Canada. It owns or has an interest in 40 upscale outlet shopping centers in North America totaling more than 14 million square feet. The trust’s market capitalization is $1.5 billion today.

Tanger released Q1 results in early May and funds-from-operations, or FFO, fell from $0.66 to $0.57 year-over-year. Funds available for distribution came to $0.54 per share during the quarter, meaning the quarter’s dividend payout ratio was just 65%, which is quite low for a REIT.

Portfolio occupancy declined fractionally to 95.4%, which is still a robust level of occupancy. Portfolio net operating income declined 0.8% but same-center NOI was down slightly less, falling 0.5%. The trust completed the sale of four non-core outlet centers during the quarter, generating $130 million in proceeds, which was used to repay outstanding line of credit balances.

We see 4% annual growth in the coming years for Tanger as rent adjustments and new leasing activity should drive low single digit long-term gains. In addition, Tanger can continue to build its portfolio of properties over time.

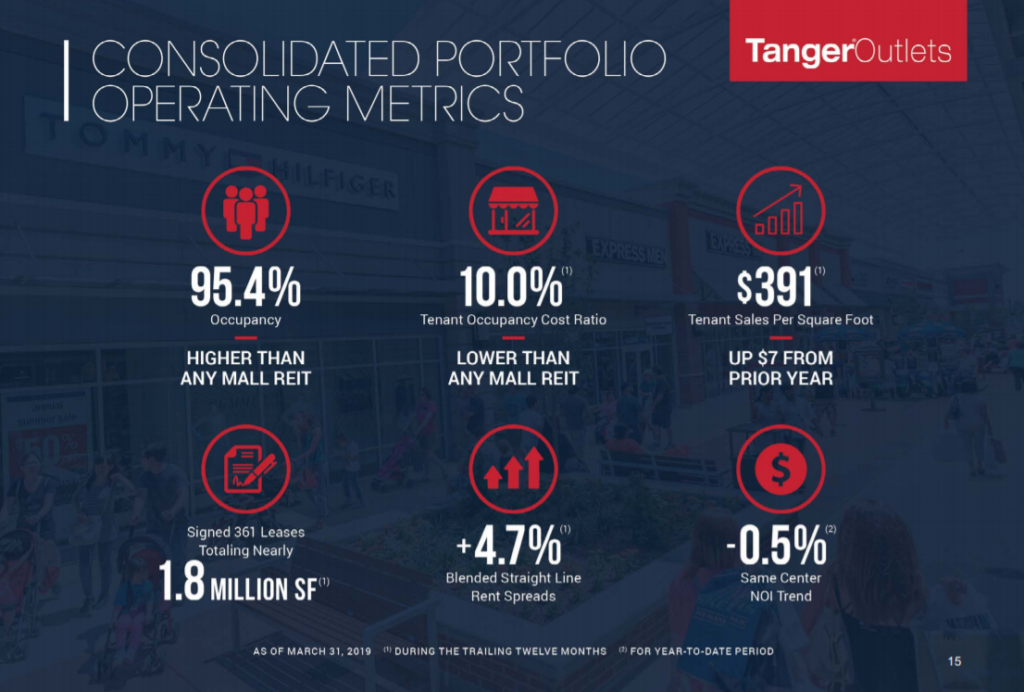

Source: Investor presentation, page 15

Indeed, this slide shows Tanger’s operating metrics, which are quite favorable. The trust’s blended straight-line rent spreads have grown nearly 5% in the past year, while tenant sales per square foot are performing well, which should help drive strong occupancy. In addition, Tanger’s occupancy cost ratio is quite low at 10%. We think this paints a favorable long-term picture for Tanger’s fundamentals.

The current payout of $1.42 is good for a whopping 8.8% dividend yield, which is quite high in absolute terms, but is also very high against Tanger’s prior yields. That means the stock is offering an extremely attractive proposition for income investors today. The dividend is well-covered, so we don’t necessarily see any safety issues either; Tanger therefore looks compelling from an income perspective.

The valuation is attractive as well, trading for just over 7 times this year’s FFO, against our fair value estimate of 12 times FFO. In total, we see 23%+ annual returns for Tanger moving forward thanks to the huge yield, low valuation, and decent growth prospects.

Final Thoughts

We like these three stocks because they all have decent growth prospects, strong fundamentals, and high yields. For income investors, these stocks represent excellent choices when searching for strong current yields, and we rate them all a buy.

The post 3 Of Our Top High Dividend Stock Selections Now appeared first on The Dividend Guy Blog.