As the television industry is going through a major evolution thanks to Netflix (NFLX), Shaw Communications (SJR.B.TO) made some important changes in their business model. In 2016, they acquired Wind Mobile and sold Shaw Media to Corus Entertainments (CJR.B.TO) a month later. While 85% of the wireless Canadian industry is controlled by three players (Telus, BCE, and Rogers Communications), Shaw has become a small player, but one with deep pockets. Is it too late for Shaw? Let’s dig deeper into this Canadian telecom.

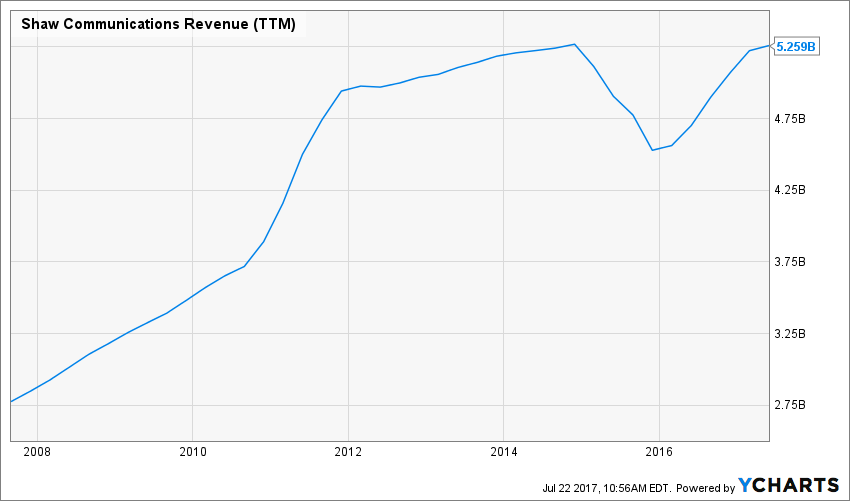

Revenue

Revenue Graph from Ycharts

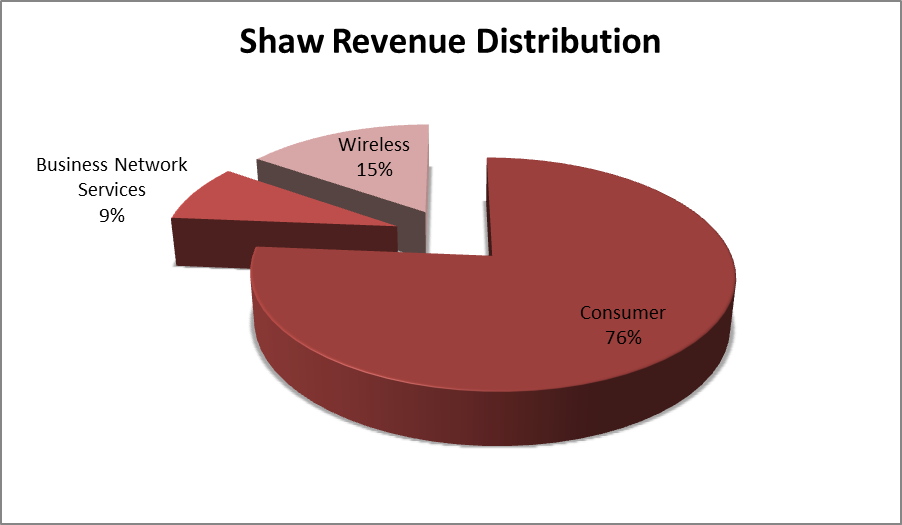

SJR is first and foremost a television company. As you can see, it focuses widely on consumers to make money:

Source: Author’s chart, data from SJR 2016 annual report

The consumer division includes cable & satellite TV (36% of total revenue), internet (26% of total revenue) and wireline phones (14% of total revenue). As Telus was going after Shaw’s cable and internet clients, management fought back with a move in the wireless segment. Unfortunately, this is more like a long term game as SJR disappointed many with only 20,000 new wireless subscribers in their latest quarterly update.

How SJR fares vs My 7 Principles of Investing

We all have our methods for analyzing a company. Over the years of trading, I’ve been through several stock research methodologies from various sources. This is how I came up with my 7 investing principles of dividend investing. Let’s take a closer look at them.

Source: Data from Ycharts

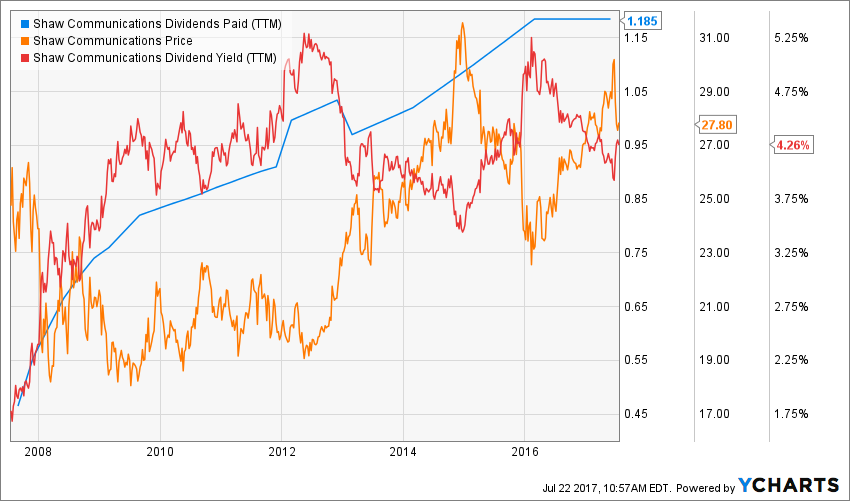

Principle #1: High Dividend Yield Doesn’t Equal High Returns

My first investment principle goes against many income seeking investors’ rules: I try to avoid most companies with a dividend yield over 5%. Very few investments like this will be made in my case (you can read my case against high dividend yield here). The reason is simple; when a company pays a high dividend, it’s because the market thinks it’s a risky investment… or that the company has nothing else but a constant cash flow to offer its investors. However, high yield hardly comes with dividend growth and this is what I am seeking most.

Source: Data from Ycharts

After 2008, SJR yield started to show on my radar. The stock has maintained a 3%-5% dividend yield over the past decade. At a current dividend yield of 4.26%, the stock shows an attractive yield for income seeking investors.

SJR meets my 1st investing principles.

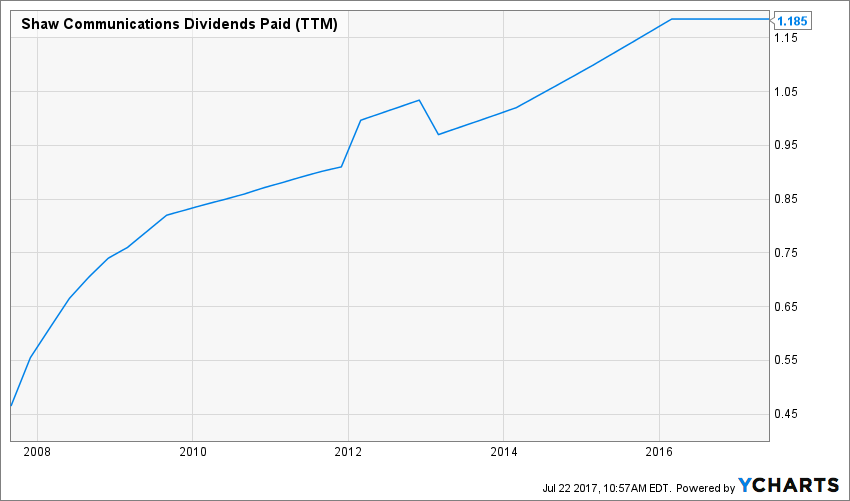

Principle#2: Focus on Dividend Growth

Speaking of which, my second investing principle relates to dividend growth as being the most important metric of all. It proves management’s trust in the company’s future and is also a good sign of a sound business model. Over time, a dividend payment cannot be increased if the company is unable to increase its earnings. Steady earnings can’t be derived from anything else but increasing revenue. Who doesn’t want to own a company that shows rising revenues and earnings?

Source: Data from Ycharts

SJR is part of the Canadian dividend aristocrats and has rewarded shareholders with several dividend increases over the past ten years. While the uptrend is not perfect, we can put SJR in the dividend growth company bag.

SJR meets my 2nd investing principle.

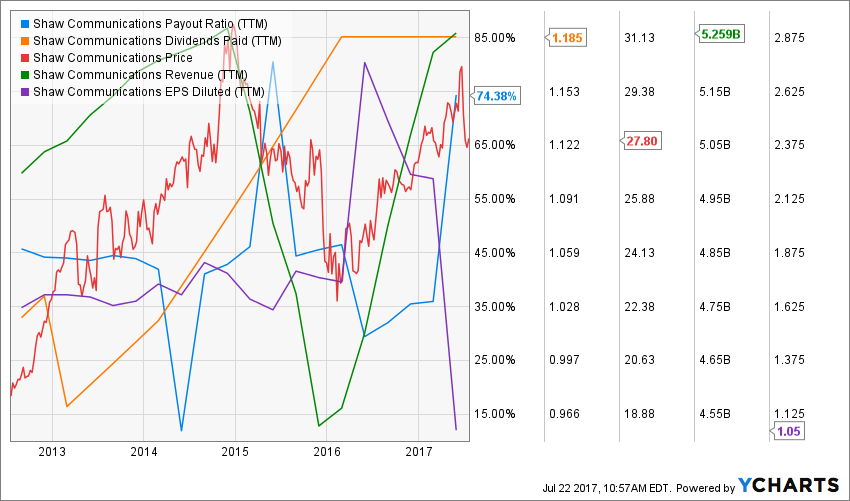

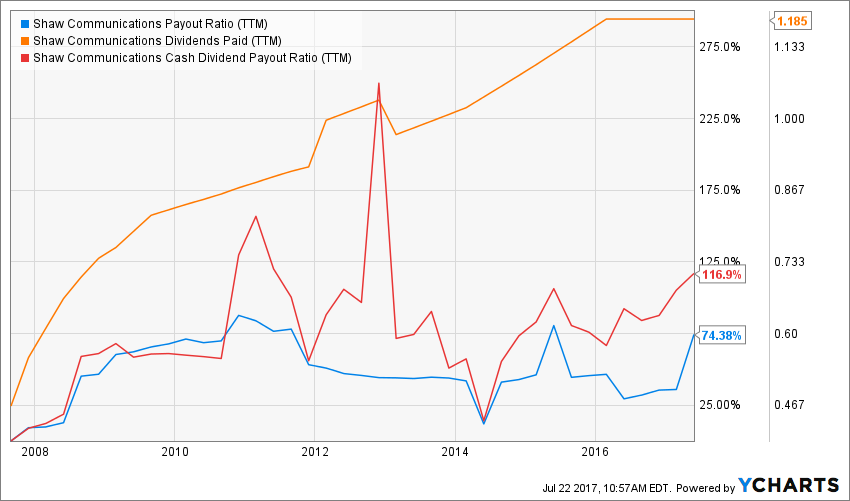

Principle #3: Find Sustainable Dividend Growth Stocks

Past dividend growth history is always interesting and tells you a lot about what happened with a company. As investors, we are more concerned about the future than the past. This is why it is important to find companies that will be able to sustain their dividend growth.

Source: Data from Ycharts

The recent earnings dip in their latest quarter pushed the payout ratio over the “comfortable” zone at 116.9%. However, since the cash payout ratio is still under control at 74.38%, management still has room to increase its payment in the future.

SJR meets my 3rd investing principle.

Principle #4: The Business Model Ensure Future Growth

SJR is lucky enough to evolve in an oligopoly. There aren’t many companies in Canada offering either television services, internet or wireless. In fact, they are pretty much always the same big guys (BCE. T, RCI, and SJR) in each field.

I appreciate management efforts to diversify their business, but it may be a little late to enter in the wireless business. While the company will have to fight to keep its television clients, it will also declare war to the BIG 3 in their own playground. However, there is definitely room for an innovative player in this industry. It will be interesting to see how Shaw will develop their wireless business in the upcoming years.

SJR still shows a good business model and meets my 4th investing principle.

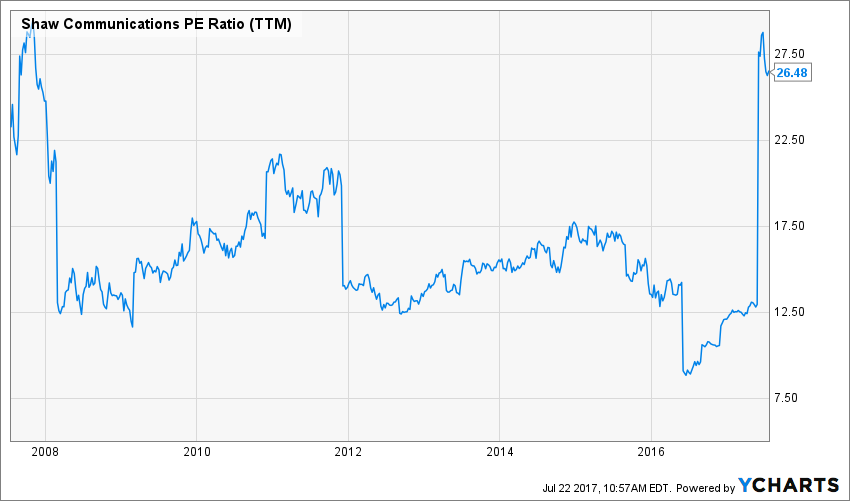

Principle #5: Buy When You Have Money in Hand – At The Right Valuation

I think the perfect time to buy stocks is when you have money. Sleeping money is always a bad investment. However, it doesn’t mean that you should buy everything you see because you have some savings aside. There is valuation work to be done. In order to achieve this task, I will start by looking at how the stock market valued the stock over the past 10 years by looking at its PE ratio:

Source: Data from Ycharts

SJR reported an important drop in earnings mainly due to restructuring cost and amortization (adjusted EPS decreased by only 0.5% in the most recent quarters). Therefore, let’s keep the previous PE ratio of 12.50-13 for comparison. The company seems to trade under its usual multiplier. This could be explained by the fact it goes through an important modification in their business model and investors are waiting to see the outcome.

Digging deeper into this stock valuation, I will use a double stage dividend discount model. As a dividend growth investor, I’d rather see companies like big money-making machines and assess their value as such.

Here are the details of my calculations:

| Input Descriptions for 15-Cell Matrix | INPUTS | ||

| Enter Recent Annual Dividend Payment: | $1.19 | ||

| Enter Expected Dividend Growth Rate Years 1-10: | 5.00% | ||

| Enter Expected Terminal Dividend Growth Rate: | 6.00% | ||

| Enter Discount Rate: | 10.00% | ||

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $46.21 | $34.77 | $27.90 |

| 10% Premium | $42.36 | $31.88 | $25.58 |

| Intrinsic Value | $38.51 | $28.98 | $23.25 |

| 10% Discount | $34.66 | $26.08 | $20.93 |

| 20% Discount | $30.81 | $23.18 | $18.60 |

Source: How to use the Dividend Discount Model

SJR seems to be trading at fair value according to the DDM model. As you can see, the company is really at a turning point and valuation will be easier in 2 years as we will see how Shaw can penetrate the wireless industry while growing the rest of its business.

SJR meets my 5th investing principle with a potential upside of 4%.

Principle #6: The Rationale Used to Buy is Also Used to Sell

I’ve found that one of the biggest investor struggles is to know when to buy and sell his holdings. I use a very simple, but very effective rule to overcome my emotions when it is the time to pull the trigger. My investment decisions are motivated by whether or not the company confirms my investment thesis. Once the reasons (my investment thesis) why I purchase shares of a company are not valid anymore, I sell and never look back.

Investment thesis

Investing in a company that is part of an oligopoly always brings additional security to your portfolio. These companies don’t move as fast as they evolve in a controlled environment. If you are ready to take the bet that Shaw can grow its wireless business up to 30% of their revenues, I think you have a serious pick here.

While I can see the investment thesis, I’m not a 100% sure Shaw can make it and beat the BIG 3. If it fails in this highly competitive business segment, I don’t know where Shaw will find additional growth.

SJR doesn’t show enough growth vector and therefore doesn’t meet my 6th investing principle.

Principle #7: Think Core, Think Growth

My investing strategy is divided into two segments: the core portfolio built with strong & stable stocks meeting all our requirements. The second part is called the “dividend growth stock addition” where I may ignore one of the metrics mentioned in principles #1 to #5 for a greater upside potential (e.g. riskier pick as well).

SJR is not the kind of stock that will push your portfolio into a double-digit return. However, it is a steady dividend payer that will bring some stability.

SJR is a core holding.

Final Thoughts on SJR – Buy, Hold or Sell?

I would have been ready to take a bet on SJR if the stock value would have been around $23. At that price, it’s worth taking the chance. As it seems fairly valued at the moment, I don’t really see why it would generate much interest for investors. In the following articles, I’ll be reviewing the other 3 telecoms and I think you will find better options.

Disclaimer: I do not hold SJR in my DividendStocksRock portfolios.