I’m receiving a lot of questions about REITs lately. On one side, interest rates are low and investors are concerned about what will happen to the loan structure once the rates go up. On the other, with such low interest rate environment, many REITs look very appealing with their high yield.

I’m also a bit concerned about the future of brick & mortar stores. Many of them are closing as they can’t keep up with online stores. It’s not like a new chain will occupy those empty spaces…. Most stores find their growth online!

To answer as many questions as possible, I’ve done a 4 parts series about REITs. They will be published within the next 2 weeks on this blog. We start today with an introduction to one of the retired most favorite dividend payer.

What are REITs How Do They Work?

First things first, there are 2 types of beasts in this industry:

- Mortgage REIT (which makes money out of buying mortgage debts and mortgage-based securities);

- Equity REIT (which makes money from operating, developing, selling, renting, real estate).

As the market shows, only 10% of Mortgage REIT and all those securities backed mortgage environment are cloudy (remember 2008 anyone?), I’ll keep my money away from this segment. On the other hand, equity REITs can be very appealing if you are looking for a steady income.

A REIT is a type of tax structure enabling the company to not pay taxes in exchange for distributing a high percentage of its profit to shareholders. To be precise, a REIT must distribute 90% of its profit to shareholders to be considered as such. Therefore, REITs are literally passing their rents to shareholders after keeping a small portion for management and maintenance fees (including interest!).

REITs have basically 3 ways to increase benefits to their shareholders: They can raise their rents, manage the property more efficiently, or buy the right property in order to maximize the growth value of each building. As you can see, these 3 ways are directly dependent on interest rates and the general housing economy. If the rates are low, the cost of borrowing is cheap for REITs and they can easily generate income.

The REIT yield has been outperforming bonds while their stock underperforming stocks. You can say that REITs are riskier than most bonds but less volatile (while less performant) than other stock on the market. If you are looking to build a 100% stock portfolio, REITs can be a great addition as it won’t lower your payouts while providing an additional hedge against volatility. It is also not as correlated to the stock market. This is why I say it’s a good match for retirees!

REITs are being traded on the stock market as any other stocks. It allows the “small” investors to participate in the real estate market without having to disburse an important amount, contract a mortgage or spend time managing his asset.

Equity REITs can be active in several markets:

- Apartments;

- Commercial centers;

- Healthcare centers;

- Office complexes;

- Industrial facilities.

Some REITs are heavily concentrated in a specific sector, while others make the bet on diversification. The same applies with respect to geographic locations.

Why should you care about having REITs in your portfolio?

There are several good reasons why investors are interested in REITs. The most popular reason is probably the high yield, REITs are more than simply the sole income trust survivors in Canada. Let’s take a deeper look at all their benefits:

You get exposure to Real Estate without being a landlord. Instead of taking care of your own tenants and answering their demands, you benefit from the joys associated with being the landlord (e.g. reaping rents and growth equity in your property) without suffering from the downside (so you don’t have to wake-up at 2am for a leaking toilet bowl!). Many people consider that bricks are more solid than anything. Investing in REITs is a new way to access this asset class without having to include “property management time” in your schedule.

Real Estate brings a great diversification to your portfolio. Research has proved that REITs are not directly correlated to stock market movements. Canadian REITs are known to be diversified and receiving steady income. Therefore, when the stock market dips, REITs won’t suffer the same amplitude of loss. One of the biggest reasons is that most investors will keep their shares in order to continue receiving their payouts!

REITs trade like stocks, therefore, it’s easy to buy this asset class. There are privately held REITs but they show too many restraint aspects when you can directly trade bigger REITs on the stock market. In a span of a few minutes, you can buy units of any REITs. This is faster than any Real Estate transaction (especially if you need to sell your shares fast for liquidity purposes!).

REITs offer predictable income stream. Prior to 2006, several retirees had over 50% of their nest egg invested in income trust. REITs are now the only asset class offering a steady monthly distribution to its unit shareholder. For someone who’s looking to build a pension plan like portfolio, REITs are definitely a great tool to create an interesting income base.

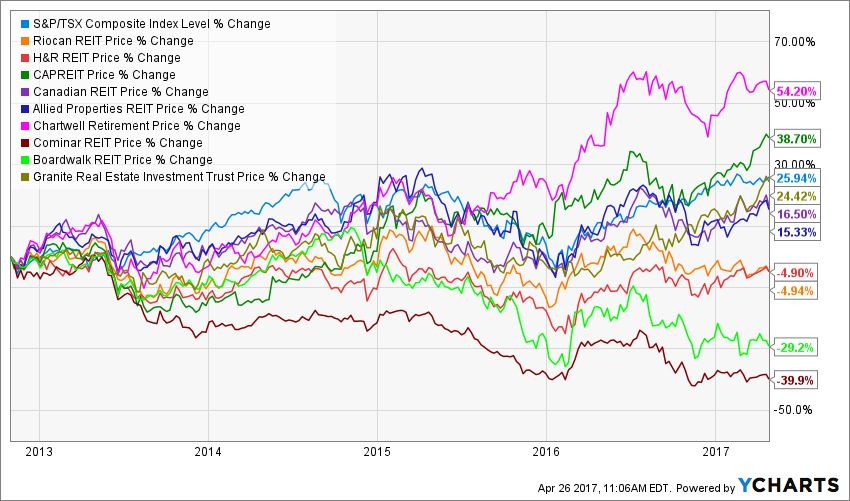

You can benefit from Real Estate growth. In a healthy real estate market, the value of buildings will rise and so will the unit price. Unit holders since 2000 are probably laughing pretty hard as Canadian Real Estate never stopped growing. So on top of receiving rents, you also benefit from the growth value through the price of your units. However, over the past five years, Canadian REITs have provided a wide range of returns:

Source: Ycharts

I’ve selected the top 9 Canadian REITs in term of market cap (I had to exclude Smart REIT (SRU.UN). As you can see, it’s not because you invest in a REIT that your portfolio value will not fluctuate. In fact, make no mistake; REITs are like ordinary stock, their value will fluctuate.

Source: Ycharts

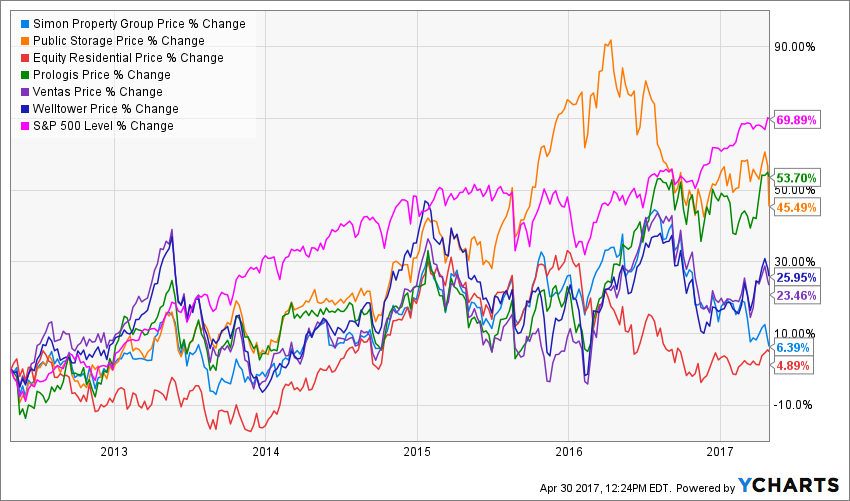

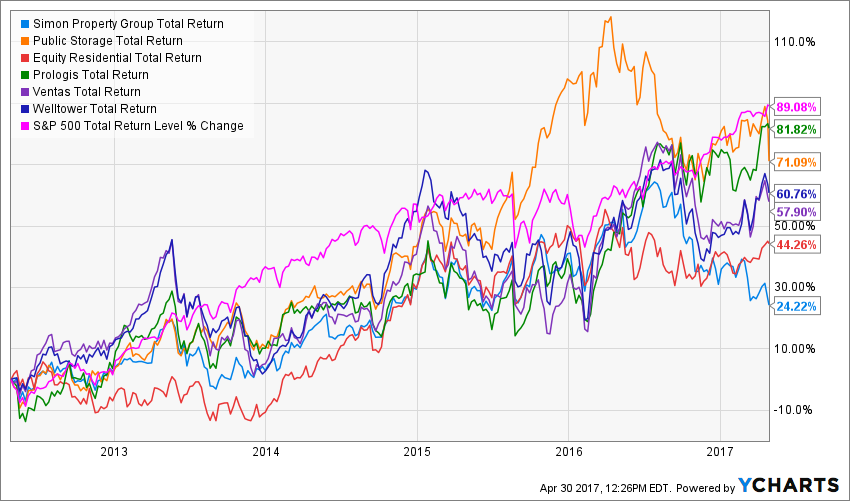

The U.S. portrait is a little bit better in term of returns as no REITs show negative results after 5 years. However, please note that all largest U.S. REITs underperformed the S&P 500 over the past 5 years. We also get the same results if we use the total price return which includes dividend payment:

Source: Ycharts

Distribution rates are usually higher than most dividend stocks or bonds. Since REITs have to distribute 90% of their revenue, the payout is definitely higher than Government bonds but they can also match (and beat!) and corporate bonds for the same level of risk.

It’s the perfect definition of passive income! The REIT environment is more stable than many other business. Most commercial, healthcare and large apartment complexes offer a pretty solid and stable income source without any great surprises. In other words, we are pretty far away from a techno oriented environment! This is how you can enjoy your payout distribution by keeping a sleeping eye on those stocks.

Offers a better diversification option than buying your own real estate (and owning 1 or 2 properties only). If you were to buy your own duplex or triplex, chances are that you would have to inject all your liquidity into a single investment. If you were unlucky enough to pick the wrong investment (tenants from hell, building structure issues, environment changes, etc), your concentration in a single asset would put you at risk.

It’s a great inflation hedge. If you are scared about inflation rising in the upcoming years, REITs can offer a great protection against it. Since rent tends to follow inflation, chances are that your distribution will increase accordingly. This is another great advantage for retirees, as they are often a victim of rising inflation throughout the year. If you retire at 60 and receive $45,000 per year with no inflation hedge, the very same $45K might not be sufficient to support your lifestyle at 80 (just think of healthcare costs!).

ROC leads to capital gain. I’ve mentioned earlier that it would be preferable to hold REITs units in a tax-sheltered account such as a RRSP, TFSA or RESP. However, if you can find Canadian REITs providing a high level of ROC (return of capital), there is some tax optimization to be done in a non-registered account. The ROC distribution is not taxable in hand but will affect your adjusted cost base of the units. Therefore, it will trigger capital gains upon the sale. This is another great way to use a different investment tool to differ taxes over time. So if you have more than one REIT in your portfolio, the strategy is to keep the high interest distribution units in a registered account and find a high ROC distribution REIT for your non-registered account.

Final Thoughts

As you can see, REITs represent a very interesting asset class for income seeking investors. They are usually more stable than regular stocks while they pay higher yield than bonds and CD’s. Unfortunately, the perfect investment doesn’t exist. I guess it would be too easy if we could find an asset class paying 8% yield with annual increase and small stock value appreciation, right? In our next part, we will explore the dark side of REITs…

Disclaimer: We hold REI.UN.TO and BEI.UN.TO in our DSR Portfolios