Summary:

The stock is up 123% over the past 5 years, excluding a juicy dividend

Dividend is growing at a 18.60% annualized rate for the past 5 years

After recent earrings, the stock is down. Is there anything left?

Dividend Stocks Rock Quick Stats

Sector: Industrial, Aerospace & Defense

5 Year Revenue Growth: 0.78%

5 Year EPS Growth: 8.00%

5 Year Dividend Growth: 18.60%

Current Dividend Yield: 3.16%

What Makes Lockheed Martin a Good Business?

Lockheed Martin (LMT) is the world’s largest defense contractor earning 61% of its sales from the US Department of Defense, 21% from other US government agencies and 18% from international clients. Heavy regulation, years of symbiosis with the US Defense and their know-how are three key elements protecting most of LMT’s business. Let’s just say you can’t start building military aircraft and missiles in your basement to compete with this defense behemoth.

The company recently designed the most advanced fighter aircraft (F-35), made important advances in light tactical vehicles and continues its work in space exploration. These are costly industries where not many competitors can compete.

How LMT fares vs My 7 Principles of Investing

We all have our methods for analyzing a company. Over the years of trading, I’ve gone through several iterations of stock research from various sources. This is how I came up with my 7 investing principles of dividend investing. The first four principles are directly linked to company metrics. Let’s take a closer look at them.

Principle #1: High dividend yield doesn’t equal high returns

The first principle is pretty much straight forward; if you look at a company with a high dividend yield, chances are the company won’t do very well in the future. The concept is fairly easy to understand; when interest rates are so low, investors are desperately looking for other sources of revenues. They then find dividend stocks! Since there is a strong demand for dividend stocks, the price increases and pushes the yield lower. If you can find companies that are paying a high yield today; it’s because they have little to no growth to offer. By looking at LMT, we can see the yield has considerably dropped from 4-5% to close to 3% these days.

Now consider the company increased its dividend by 18% annually during the last 5 years… quite impressive. This leads me to my second investing principle.

Principle#2: If there is one metric, it’s called dividend growth

In the past 5 years, the 1st quintile of dividend growers (companies that have the highest dividend growth rate) outperformed the others:

LMT is among the best dividend growers over the past five years and there is no coincidence that the stock price surged during the same period. Strong dividend growth is a sign management is confident about the company’s future. Over a short period of time however, it could be a simple way to lure investors. On the other hand, a company can’t keep up this strategy very long if it doesn’t generate strong sales and profits. There is a limit to playing with accounting standards and the limit is called time.

In the case of LMT, revenues didn’t go so well as the company faces a terrible problem; its client (80% of its business comes from the US govt) wants to cut their defence budget. This won’t help LMT in the years to come. While LMT will benefit from a small break since many contracts have been awarded for 2015 and 2016, the Gov’t still has to cut its budget before 2021 due to the sequestration law. We can clearly see that LMT did a remarkable job in increasing its earnings while cutting its costs, but this can’t last forever. Revenues will have to increase again to maintain a solid dividend growth.

Principle #3: A dividend payment today is good, a dividend guaranteed for the next ten years is better

In the light of LMT’s current sales growth problem, can we expect them to keep the dividend payment for the next ten years and beyond moving forward? The answer is yes. The defense business will always remain a strong need in the world and LMT will remain a key player. The payout ratio is under control at 50%. This is why I’m not concerned about the dividend payment for several years ahead.

However, I don’t expect an annualized 18% rise in the future either. A more reasonable increase in line with single digit earnings growth would be more realistic.

Principle #4: The Foundation of dividend growth stocks lies in its business model

I think it is safe to assume Lockheed Martin operates in a very strong moat. The resources and knowledge required to compete with LMT in the defense industry is very hard to acquire. While revenues might hit a speed bump in the upcoming years, the need for defence products will not stop. The business model is strong and LMT has recently improved its margin on the F-35 production.

I think LMT has a short term problem and this could affect the price you should buy the stock at. However, for a long term dividend portfolio, this could be a great core stock.

What Lockheed Martin Does With its Cash?

I’m under the impression management does everything to keep their investors happy and almost blinds them with major share repurchases and strong dividend growth. The business obviously requires tons of cash to be invested in R&D and new technology, but management still has $3.6 billion worth of shares approved for repurchase in the future. In their 2014 financial statement, management clearly stated their focus will be applied to increasing the dividend and to buy more shares over the next three years.

Note that even if LMT shows a heavy pension contribution in the 2014 financial reports ($2 billion), the business generated an additional $3.9 billion cash flow from operations. This is a true cash flow machine.

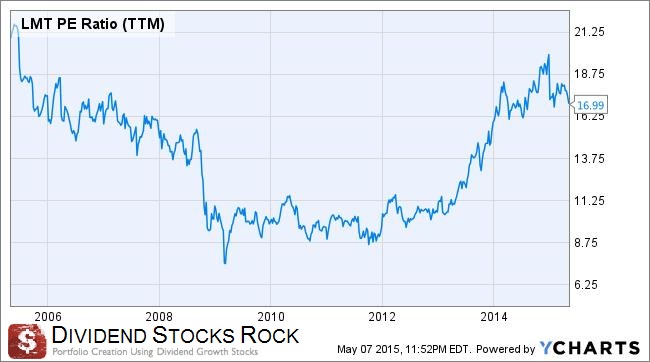

Should You Buy LMT at this Value?

Ah! This is the right question to ask; are you burning cash buying LMT at this price? Let’s take a look at the past 10 years history of price earnings ratio:

We have to understand LMT’s value was hurt mainly because of the sequestration bill passed after the 2008 crash. Defence budget was clearly hit by this law and put LMT revenues under pressure with little to no growth for ten years. We all know 10 years is bigger than the cosmic universe on the stock market. Nonetheless, LMT management caught investors’ attention with strong earnings growth doubled in conjunction with high dividend growth. As dividend investors, we probably overlooked the company revenues a bit to focus on our own.

In order to have a better understanding of the company’s value, I used the dividend discount model calculation spreadsheet with two stages. I used a 10% dividend increase for the next 10 years and dropped it down to 5% afterward. I think the company will continue to hike the dividend as high as it can until revenues come back up. They have a strong cash flow machine in hand and can play this game for a few more years. Since the business is relatively stable and the worst may have already happened to LMT, I use a 10% discount rate.

Source: Dividend Toolkit

Source: Dividend Toolkit

The stock is currently trading near $190 and my fair value calculation stands at $170. In other words; the stock is trading at a 20% premium.

A premium paid for strong dividend growth in the past years, a strong economic moat where competitors won’t play very long against LMT and a premium paid for a dividend stocks showing a yield over 3%… still in this crazy market!

What I Would Do With LMT if I Had 10K in Hand

If I had a new 10K to invest in this company, I wouldn’t do it at the moment. I think the stock is overpriced and doesn’t show the growth potential that can lead to a higher price. However, I’m keeping my shares since they are part of my core portfolio where I expect to keep a company for 10 years and maybe more. LMT is definitely a good company to hold, but it’s just not the right time to buy it now…

Disclaimer: I hold LMT shares at the moment