Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas.

As we prepare for another surge of COVID-19 cases, it’s more important than ever to have the right holdings in your portfolio. Here are two dividend growth stocks that should face the second wave without much problems. Next time, we’ll cover two options for income-seeking investors.

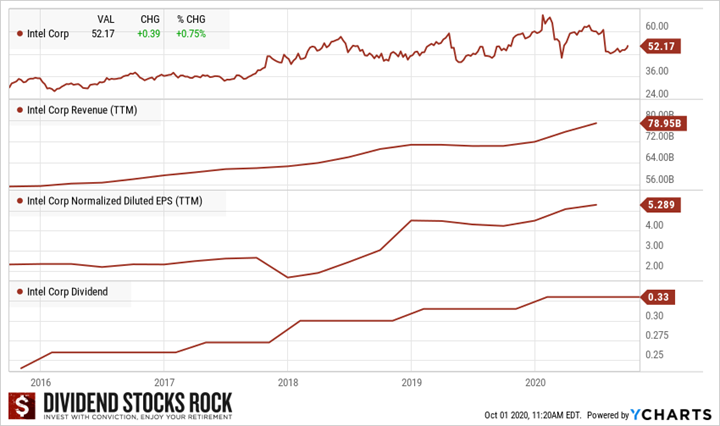

Intel (INTC)

What’s the story?

Intel was added to my buy list last month after disappointing the market about delays on their new chip. Interestingly enough, investors blamed INTC for having a large exposure to the PC market. While it’s not good news, INTC could lose some market share to AMD. Intel’s main growth is not going to come from this segment in the future.

In fact, many seem to have forgotten INTC has shifted towards data-centric business services. This segment is now bigger than its PC market (52% vs 48%). The most important point is that the data-centric segment was up 34% last quarter. Management expects to grow this business up to the point where it will represent 70% of INTC’s total revenue.

This is where your attention should go. INTC will lag a bit on their 7nm chip, but will continue to grow their business, nonetheless. INTC will not stay in the $50’s for very long.

Business Model

Intel Corp is one of the world’s largest chipmakers. It designs and manufactures microprocessors for the global personal computer and data center markets. Intel pioneered the x86 architecture for microprocessors, and it is also the prime proponent of Moore’s law for advances in semiconductor manufacturing. While Intel’s server processor business has benefited from the shift to the cloud, the firm has also been expanding into new adjacencies as the personal computer market has declined. These include areas such as the Internet of Things (IoT), memory, artificial intelligence, and automotive.

Investment Thesis

INTC is the microprocessor king. As it enjoys strong cash flow from its PC business, the company has expanded into new business segments. INTC developed a completely new business model around the cloud with its data-centric services. With this fast-growing segment, INTC has gained some love from the market. INTC generates strong cash flow from its core business while its data centric (about 50% of revenue) is showing double-digit growth. We liked INTC’s decision to sell its 5G modem business to Apple to keep its focus on data-centric businesses. INTC is going for acquisitions in AI and IoT in the automotive industry. Those plays will contribute to its growth plan.

Potential Risks

While everything is positive for INTC these days, technology evolves fast. INTC isn’t the only one interested in server processors, IoT and AI technology. The company faces strong competition from other “old techno’s” such as NVIDA and AMD. INTC is doing well with data centers, but it has failed miserably to enter one of the most lucrative markets in tech over the past decade: smartphones. For a chipmaker of that size, we would have expected dominance in that field. This proves that Intel isn’t flawless. Finally, the PC business is still profitable, but is also mature and declining. Therefore, INTC won’t be able to count on this cash flow machine forever.

Dividend Growth Perspective

Intel shows consecutive dividend increases since 2015. Strong from its new growth drivers, INTC show a low payout ratio. With both payout ratios under 50%, expect mid to high-single digit dividend growth for the upcoming years. The PC business will continue to generate strong cash flow that is not only used to finance the company’s growth, but also to buy back shares and increase its payouts.

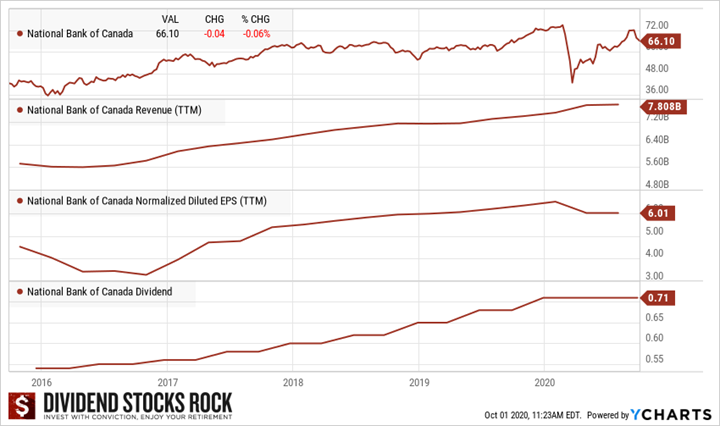

National Bank (NA.TO)

What’s the story?

If you follow me on a regular basis, this isn’t a surprise! Most of my readers know my love for National Bank already.

As COVID-19 cases have surged in Quebec for the past 2 weeks, National Bank has seen its share price tumble. On September 28th, the Government announced a series of business temporary closures (28 days) and a partial lockdown for the region of Montreal and Quebec City. This should slowdown the economy and hurt NA’s business.

At the same time, I expect strong volatility coming from the market in the coming months. NA’s exposure to capital markets and wealth management segments should compensate for sluggish savings & loans activities.

Business Model

National Bank is very small compared to the big 5 Canadian banks. As the sixth largest one, NA is mostly in Quebec with 62% of its revenues earned in this province. Its smaller size is currently paying off as National Bank was quicker to develop a strong brand in Wealth Management with Private Banking 1859 and built a highly profitable Financial Market division.

Investment Thesis

Like BMO, NA aimed at capital market and wealth management to support its growth. Private Banking 1859 has become a serious player in that area. The bank even opened private banking branch only in Western Canada to capture additional growth. Since NA is heavily concentrated in Quebec, it concluded deals to do credit for investing and insurance firms under the Power Corporation (POW). Branches are currently going through a major transformation with new concepts and enhanced technology to serve clients. While waiting for the results, it seems wise to invest in digital features to reach out to the millennials and improve efficiency. The stock has outperformed the Big 5 for the past decade as it showed strong results. Recently, NA is seeking additional growth vectors by investing in emerging markets such as Cambodia (ABA bank). Can it have more success than BNS on international grounds?

Potential Risks

National Bank is still highly dependent on Quebec’s economy. As a “super-regional” bank, NA is more vulnerable to economic events. So far, the covid-19 situation in Quebec as been well managed and NA posted satisfying results in May 2020. However, we are far from being done with the pandemic. Capital markets revenues are also highly volatile. NA could run into a bad quarter if the stock market enters into a bearish environment. The bank has considerable exposure to the oil market through its commercial loan portfolio. Overall, the bank performs very well, but usually take a little more risk to find growth vectors (such as ABA bank investment and capital markets). So far it has paid well, but it doesn’t mean it will always work.

Dividend Growth Perspective

National Bank offers a generous dividend growth policy. The bank has shown one of the most generous dividends increase in the past 5 years (vs the other Big 5). Not bad considering the company had to take a pause in its increase between 2008 and 2010 due to the financial crisis. The bank should pause its dividend growth policy in 2020 and wait to know the full impact of the pandemic on its loan portfolio. So far, it seems that NA can easily navigate through this challenge. However, we are far from being done and we must wait a few more quarters (ready beginning of 2021) to understand the full impact of the covid-19 on the economy.

Canadian Banks Ranking for More Ideas!

If you want more dividend growth (yet safe) stock ideas, I suggest you go through my Canadian Banks Ranking! These banks have outperformed the Canadian market for many years; they show strong metrics and can still offer growth potential. Finally, they also trade on the US side. Do not be mistaken though, they are not created equal! Make sure you choose the right one for your portfolio.

The post Ride the Crest of the Second Wave with These Two Dividend Growth Stocks appeared first on The Dividend Guy Blog.