The US market started on a downer in January 2014 showing -2.70% (S&P 500). There were many investors who supposed that this one month trend would set the tone for the year. Well, if you were one of these investors, you have missed something. As at November 28th 2014, the S&P 500 posted a positive return of over 13% excluding dividend, 15.29% with dividend.

In general, the stock market has become more volatile. We went through a few drops throughout the year, the most important being after Germany announced they were entering recession territory in October. However, Q3 earnings season results were better than expected and the market has since hit new records.

In November, during Q3 earnings season, 77% of the S&P500 companies beat earnings estimates while 59% of them reported sales above expectations. These results are better than what was posted for Q3 2013. The current 12 month forward P/E ratio is 16, still sitting on the historic average.

Similar to what happened in 2013, the US economy continued to pick-up more strength with a GDP growth in November of 3.9%. New home construction is now slightly over 1 million (annualized), and the unemployed rate dropped under the bar of 6%. All this led the FED to stop its QE3 completely in October. However, while the FED stopped injecting money into the bond market, it will continue to renew its portfolio with new maturities and reinvest interest for now.

One of the biggest challenges for 2015 will be to see how the market will react when the FED will increase the overnight interest rate (expected mid-2015). In the meantime, the very low price of oil should help US consumers to spend more and drive the economy higher.

As I do it each year, I’ve picked 20 dividend stocks to beat the market in 2015. My 2015 selection includes companies selling products directly to American consumers in order to benefit from the drop in oil price leading to a bigger family budget. Once again, I am bullish for 2015, but which dividend stocks will do better? Using my 7 dividend investing principles, I’ve made my list of the best dividend stocks for 2015.

Which Stocks Will Outperform the Market in 2015?

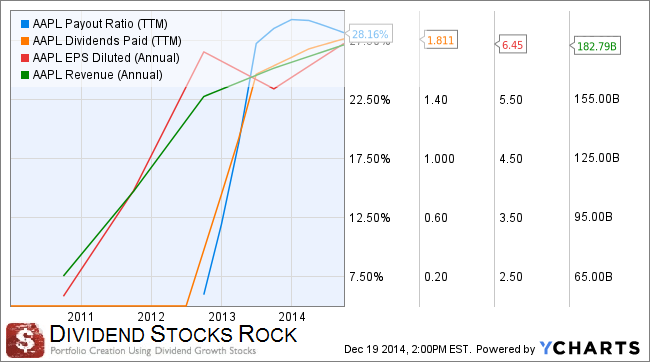

APPLE (AAPL)

COMPANY DESCRIPTION:

COMPANY DESCRIPTION:

We all know what Apple does, but just in case you have been sleeping under a rock for the past 10 years, Apple designs, manufactures and markets mobile communication and media devices.

STRENGTHS:

Apple has come back strong on the market in 2014 with a +48% (as at November 28th). This is due to unexpected sales growth of its famous iPhone series. This rally is also due to another phenomenon; it seems that AAPL is now winning its war against Samsung by offering a bigger phone for its 6 series. Samsung has put so many products on the market that it’s now struggling to generate bigger profits and has forced a retreat. In the meantime, AAPL is pushed by strong winds and will launch its Apple Watch early in 2015. This won’t be the next big thing, but it will surely contribute to Apple’s almost perfect product ecosystem.

WEAKNESSES:

I note two weaknesses that could hurt Apple in 2015. The first one is the price the stock is trading at (currently at a PE ratio around 17-18). Investors might expect too much from this techno in 2015 and the stock could suffer. The second weakness lies within its tablet offering. The iPad is struggling to keep its market share and this hasn’t helped AAPL to diversify its income sources since the iPhone represents about 50% of its profits. Expect volatility, and you can’t go wrong with a company generating about $10B in free cash flow per quarter.

COMPANY METRICS:

COMPANY DESCRIPTION:

COMPANY DESCRIPTION:

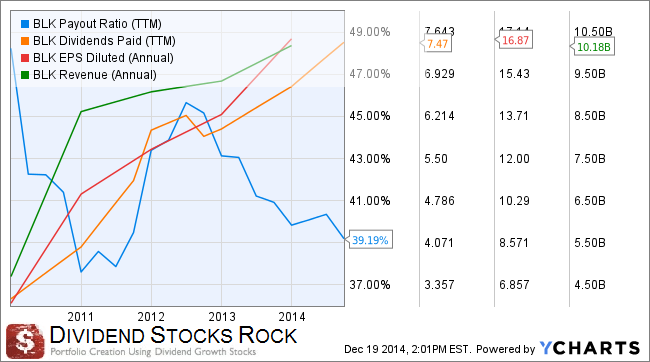

BlackRock Inc., along with its subsidiaries, provides investment management services to institutional clients and individual investors through various investment vehicles. It is very well known for its iShares ETF products.

STRENGTHS:

As long as the market is bullish, BlackRock will be among the top performers. ETF investing is a strong trend and will continue in the upcoming year. The fact that almost anybody could follow a coach potato approach and simply rebalancing index ETFs once every 6 months makes these products very interesting. BLK shows a strong dividend profile also with strong growth (16% over the past 5 years) combined with an EPS growth equally strong (almost 24% over the past 5 years). When you combine these results with such a low payout ratio (39%), you definitely get a winner to add to your portfolio. BlackRock did not only surf the wave over the past two years, but clearly posted impressive results. Plus, there is still lots of money invested in mutual funds that could head into ETFs over the years to come.

WEAKNESSES:

While ETF investing is a very strong trend in the industry, there is also lots of competition. BLK has to play with other behemoths such as Vanguard. If the market slows down, BlackRock might also find it more difficult to increase its asset under management (AUM). In this kind of business, the size of your assets truly matters.

COMPANY METRICS:

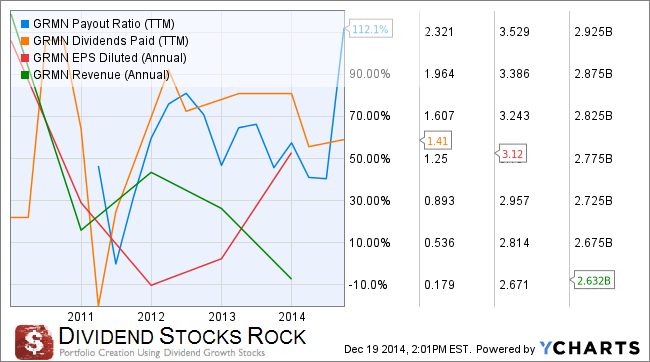

GARMIN (GRMN)

COMPANY DESCRIPTION:

COMPANY DESCRIPTION:

Garmin Ltd., designs, develops, manufactures and markets a diverse line of user-friendly handheld portable and fixed-mount products for the auto/mobile, outdoor, fitness, marine and general aviation markets.

STRENGTHS:

Strong from many innovations to integrate its technology, Garmin doesn’t only tell you when to turn left anymore; 58% of its revenues come from the non-automotive and mobile segment. Aviation (+19%), marine (+19%) and outdoor products (+10%) show strong revenue growth. As their first quarter reports, their 2014 FWD guidance was in line with analysts’ estimates. They also increased their dividend payout from $0.45 to $0.48 a share. Their fitness line (outdoor products) is not only trendy but highly lucrative. Since 2012, the EPS is going up and has made up for the high payout ratio. The major transformation in their core business (introducing aviation, marine and outdoor products) has been proven successful and GRMN is about to reap the benefits of a long wait. Note that the fitness segment now represents 16% of its sales and combined with the other outdoor products, this is 33% of all sales.

WEAKNESSES:

GRMN shows a high payout ratio at the moment (112%). This is why it still represents a risk and should not be considered for conservative investors. Combined with a high P/E ratio (33), this company is now surfing on the hope of strong results in 2015. If it fails, the stock will plunge.

COMPANY METRICS:

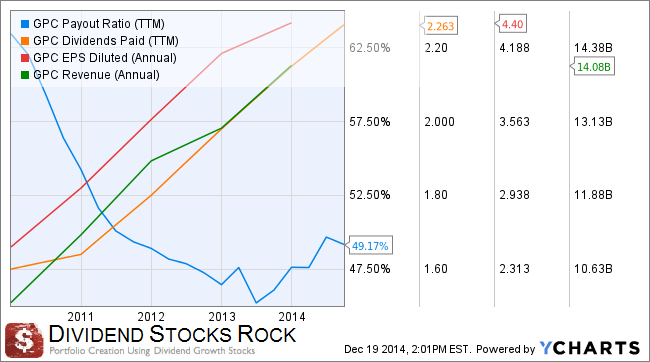

GENUINE PARTS (GPC)

COMPANY DESCRIPTION:

COMPANY DESCRIPTION:

Genuine Parts Co is a service organization engaged in the distribution of automotive replacement parts, industrial replacement parts, office products and electrical & electronic materials. This dividend aristocrat has an interesting growth model combining small but recurrent acquisitions added to internal growth.

STRENGTHS:

When you look at the metrics, you can see that sales, earnings and dividend payments are all going in the same direction. We also believe in the car industry for 2015. GPC is another strong dividend aristocrat that should continue to raise its dividend this year. The company shows a strong balance sheet and the ability to increase its dividend for years. GPC not only shows good results but it also grows by acquisition. In 2014, they bought Garland C. Norris, EIS, Electro-Wire and Impact products. GPC continually looks for companies to buy with revenues in the range of $25M to $125M. These bites are easy to chew on and don’t affect their balance sheet in a negative way. Their ability to integrate new companies is reflected in their earnings which show a steep uptrend. GPC will continue to be a leader in its industry and we won’t lack for car parts in the near future.

WEAKNESSES:

While I like the numbers, I don’t like the fact that GPC failed to meet analysts’ estimates from time to time. They were too optimistic at the beginning of 2013 and raised their guidance to disappoint 9 months later with lower than expected results. Then again, the stock shows a low dividend yield around 2.25%, this might turn off some investors… not me!

COMPANY METRICS:

Want More? I have 16 other Dividend Stock Picks in my Book!

I’ve compiled a list of 20 dividend stocks to do well in the market for 2015. You just read about four of them, but there are still lots to discover in the book! The book includes the 20 dividend stock analysis plus 10 Canadian dividend stocks. That’s 40 pages worth of information for only $4.99.

This year, I offer both versions: PDF or Kindle.

Click here to buy the PDF version (pay with credit card)

Click here to buy the Kindle version (Amazon link) (coming soon)

Disclaimer: I hold AAPL in my personal portfolio and all stocks mentioned in this article are part of our DSR portfolios.