I’m known to be an optimist, a guy that will always tell you that today is the best day to invest your money… since you missed yesterday! While I’m confident that I will have another great year in the stock market, I’m also not a lunatic with pink glasses either. Unfortunately, there are some dark clouds rising at the moment which concern me. Here are three things that scare me the most in 2018.

01 Canadian Debt Level & Housing Market

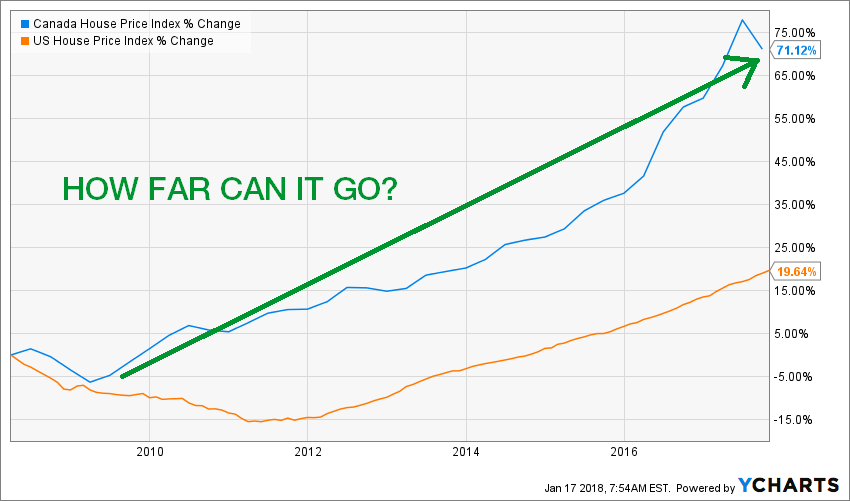

I’ve been concerned about the Canadian housing market since 2012 and I’m sure I sound like a broken record. However, this situation doesn’t make sense to me:

Source: Ycharts

Do you remember what happened when Americans started using their house like an ATM machine? Yeah… 2008 happened. As you can see from the chart above it took them until 2014 before reaching 2008 levels. What about us? We flew like Canadian goose flying wild toward their Florida party during winter time. Our market just ignored the warnings. As Canada was proclaimed the country with the “world’s best banking system”, many foreign investors shifted their money toward our Real Estate market. It’s nice to get some positive attention, but with a household debt level hovering around 170%, new mortgage rules requiring a “stress test” for all new borrowers, I don’t see how we will go through this situation without a housing correction.

What I plan to do about it

I plan on keeping my house. I’m comfortable here and I don’t plan to move for the next 5 years. I secretly hope that my children grant me the permission to sell everything and travel the world but I know their friends matter to them and I know I will be “stuck” in this winter country for a while.

As far as my investments, I have a reasonable position in the Canadian banking industry with Royal Bank (RY.TO) and National Bank (NA.TO). Both banks show strong positions in the capital and wealth management markets while leaving the classic mortgage business to TD (TD) and CIBC (CM). In the event of a market crash, National Bank should not be affected too much as the bulk of its mortgage portfolio is in Quebec, one of the provinces that has not been affected by the housing bubble.

02 Bitcoin!

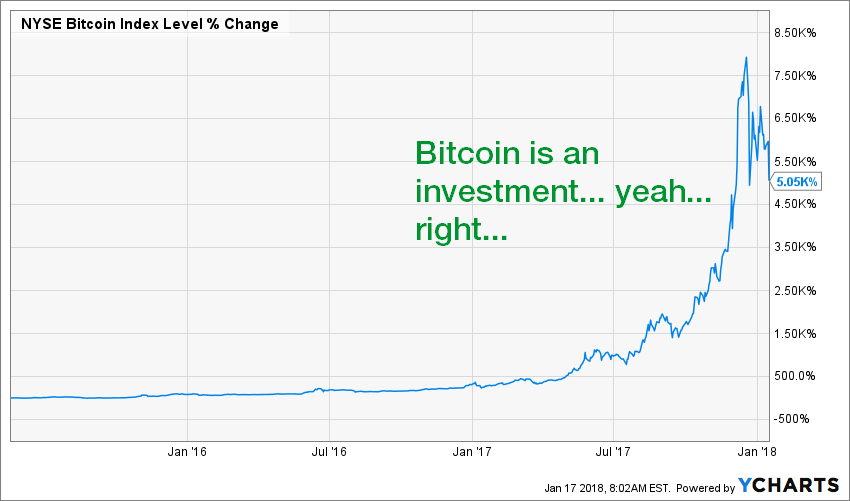

I already wrote about why I decided to ignore bitcoins and other cryptocurrencies. I don’t deny their technology is a game changer in the financial industry but investing in a stupid coin in the hope that another stupid investor would buy it at a higher price is not a risk I’m prepared to take. If this doesn’t sound like the techno bubble, I don’t know what is:

Source: Ycharts

If you are a bitcoin fan, I’m urging you to explain to me what the value is behind a bitcoin. Which gives bitcoin its value? Please tell me your rationale behind a bitcoin at $10 or $10,000 or $50,000? Here’s a hint; if you can’t tell me what your value of a bitcoin is, then don’t have an investment in your portfolio, you have speculation. Unfortunately, we all know where speculation leads. “Not this time, it’s different”… yeah… keep drinking the Kool Aid!

What I plan to do about it

Not much. In fact, I stay away from cryptocurrencies. My play was to invest in Visa (V) as it will benefit from the blockchain technology. Another play could be to look at CME Group as I discussed in a previous article about the bitcoin frenzy. But there is no way I’m buying any coins. If you leave a coin in your virtual shelf for 10 years, what that coin will produce? Nothing. This is the reason it has only value if someone else is ready to pay more for it. And the reason why someone is ready to pay more for it is only because they believe someone else is ready to pay more. Does this scream a pyramid scheme? I’ll let you decide.

03 Remember Greece?

Do you remember what happened in 2012 when we all thought the world would collapse because of the Greek debt? Let me remind you of the important parts.

- Most (if not all) countries owe money to someone else.

- A good part of this money is lent among countries, another part among banks.

- If a country fails to pay its debt, banks will fall.

Do you remember the last time banks fell? Yeah…

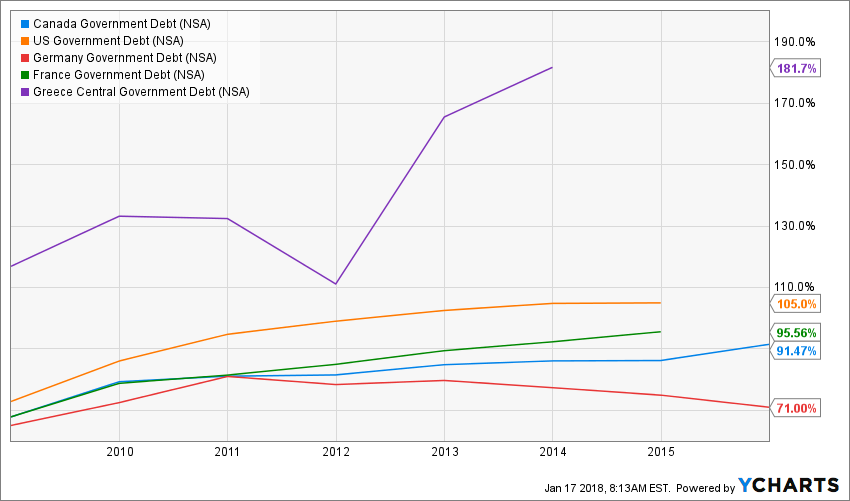

Source: Ycharts

The graph above shows some countries government debt as a percentage of their GPD. As you can see, besides Germany, everybody keeps borrowing more. My question is simple, where does this all end? As an individual, we all know that we have a limited amount of money we can borrow. This limit is set by banks and other financial institutions. While the limit isn’t 100% clear, we all know that if we keep borrowing, one day, no bank will loan us more money to keep going. The next step the banks will take is to start asking for their money back. Thus, this is how we can go bankrupt.

Government debt isn’t that easy. It’s a complex beast and not many people are able to explain it. In fact, I’m humble enough to tell you that I’m not sure how to figure it out myself. However, there is one thing I understand, borrowing indefinitely can’t be the answer. One day, somebody, will have to pay their due. But nobody wants to hear about paying down their debts, austerity or about being responsible. This has no political value. This is boring stuff. Unfortunately, one day, we will have to all sit at the big table and have an adult conversation about what is going on.

What I do about it

I personally did a stricter budget and started to focus on paying down my debts in a more proactive way. In 2018, my company should generate enough extra cash flow that I will be able to reduce my debt while not pursuing any new purchases.

As for my investment, I’ve pick solid dividend growers. The idea is to pick companies that have a strong business model that will go through the next recession with more dividend increases. Since there isn’t much I can do about the government’s debts, I rather focus on building a strong portfolio and take care of my own stuff!

What worries you about 2018?

What about you? Is there anything that doesn’t make sense in the stock market or the economy? What do you think will go wrong in the upcoming months?

The post 3 things that scare me for 2018 appeared first on The Dividend Guy Blog.