Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas.

As both markets did well in August, more of our ideas have outperformed the market. I decided to share some of our picks with you. Today, we’ll cover two growth stocks that still show some potential return.

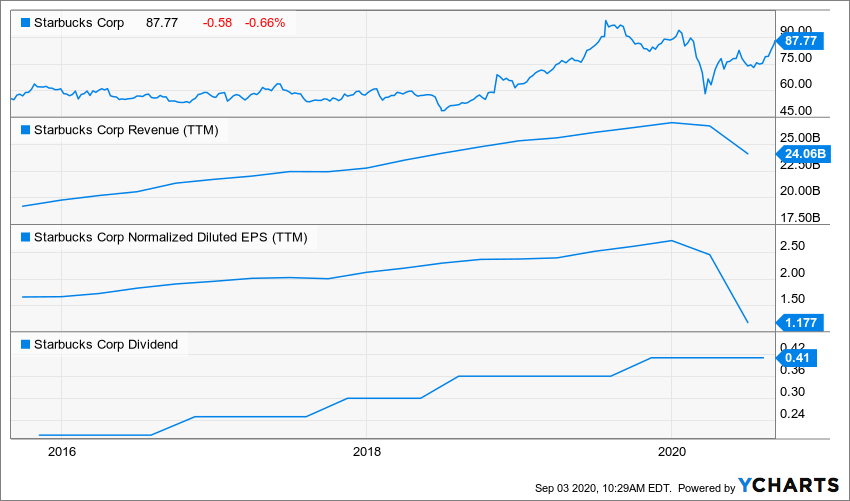

Starbucks (SBUX)

What’s the story?

SBUX has been on a roll in August. As restaurants reopened across the world, SBUX is likely to continue its growth path going forward. More attention has been drawn toward this stock as an investment firm, Stifel, has recently increased its rating to “buy”.

SBUX is arguably one of the restaurant chains that is best positioned to adapt moving forward. With over 16 million members in their loyalty program, Starbucks knows exactly what you want to consume, and when and how you will consume it. Having access to such data will be a critical turning point in adapting to the new reality of the post-COVID-19 economy.

Business Model

Through a global chain of more than 32,000 company-owned and licensed stores, Starbucks sells coffee, espresso, teas, cold blended beverages, food, and accessories. The company also distributes packaged and single-serve coffee, tea, juice, and pastries through its own stores, grocery store chains, and warehouse clubs under the Starbucks and Teavana brands and the Global Coffee Alliance partnership with Nestle. In addition, Starbucks markets bottled beverages, ice creams, and liqueurs through partnerships with Pepsi, Anheuser-Busch, Tingyi, and Arla. In fiscal 2019, Starbucks’ Americas segment represented 69% of total revenue, followed by the international segment at 23%, then channel development at almost 8%.

Investment Thesis

The company enjoys one of the strongest brand recognitions across the world and uses it to expand its stores across China. With 500-600 new store openings per quarter, SBUX is growing rapidly in this country. This growth plan will have to take a pause in 2020 but will surely keep-up in 2021 as the economy is reopening. As a bonus, Chinese stores are a lot more profitable than U.S. ones. The coffee maker also counts on its powerful membership (over 19.4M members) to boost comparable sales. Its reward program grew its members by double-digits in 2019. Finally, SBUX should grab more market in China as Luckin Coffee is stuck with fraud problems.

Potential Risks

SBUX growth potential in the U.S. is nearly nonexistent. It will get worst in 2020 as many smaller stores are in shopping malls. Plus, there is a limit to the amount of coffee that can be purchased by an American! The pandemic will affect SBUX sales as many of its customers buy coffee in the morning on their way to work. Closing some stores didn’t help either! Will the $5 coffee remain relevant when you lose your job? As the company faces headwinds in China or India, its growth potential will be highly reduced for the upcoming two years. The company has a break from competitors as Luckin Coffee if facing serious problems after fabricating sales.

Dividend Growth Perspective

Starbucks has increased its dividend payment for the past seven years. Over the past five years, SBUX raised its dividend payment from $0.16 to $0.41 quarterly. This is an incredible annualized growth rate. With low payout ratios, management has lots of room to fuel both its growth strategy in China and its dividend payments. We expect a lower dividend increase in the upcoming years and no increase in 2020. However, the long-term perspective remains the same. Starbucks will continue to dominate the coffee world as the economy reopens.

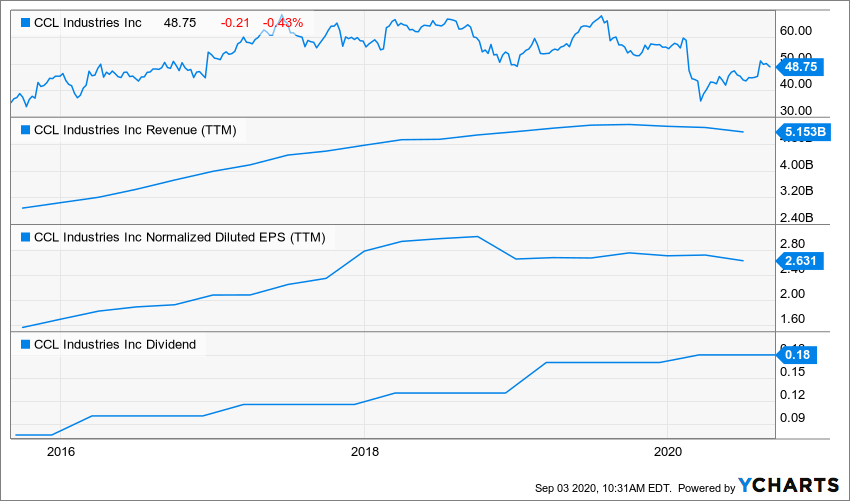

CCL Industries (CCL.B.TO)

What’s the story?

CCL reported their earnings on August 7th and it wasn’t the best quarter. Both revenue and EPS were impacted by the industry’s volatility and uncertainties. CCL segment’s sales were down 6%, Avery’s was down 28%, Checkpoint was down 31.5% and Innovia was up 21.4%. On a positive note, management expected worse.

Higher volumes and amplified demand for pantry loading fueled the latter’s performance. The company completed a bond offering, raising $600M of 3.05% 10Y bonds. Cash on hand at quarter’s end was $619.4M, with an additional borrowing capacity of $1.2B. The dividend remained intact.

Later in August, CCL announced the acquisition of Graphic West International ApS, a specialized digital printer of short-run folding cartons for the pharmaceutical and medical device industries with operations in Europe and North America. Sales for the 12 months ending June 30, 2020 were approximately $42 million with an estimated adjusted EBITDA of $6 million. GWI will be integrated into CCL’s Healthcare & Specialty business and will immediately adopt their trading identity. Closing of this transaction is subject to regulatory approvals and is expected to close early in the fourth quarter 2020.

Business Model

CCL Industries Inc manufactures and sells packaging and packaging-related products. The company operates through various segments which include The CCL segment, which generates the majority of revenue, sells pressure sensitive and extruded film materials used for labels on consumer packaging, healthcare, automotive, and consumer durable products. The Avery segment sells software, labels, tags, dividers, badges, and specialty card products under the Avery brand. The Checkpoint segment includes the manufacturing and selling of technology-driven, inventory management, and labeling solutions. And Innovia segment through which it manufactures specialty films. The majority of revenue comes from North America.

Investment Thesis

It is quite rare to find a world leader with a well diversified business based in Canada! Through a major acquisition (business units from Avery (AVY)) back in 2013, the company has set the tone for several years of growth. Strong from its previous success, CCL also bought Checkpoint and Innovia in the past few years. The company is still able to generate organic growth (roughly 4-5%) on top of their growth by acquisition strategy. You can also rest assured that management’s interests are aligned with yours since the Lang family still owns 17% of CCL shares. At this point, our only concern is its valuation and its debt level (see risks section).

Potential Risks

We often see rising stars like CCL making many investors rich over a quick period of time. Back in 2014, the stock traded at around $15. But since 2017, shares have been going sideways as the hype is fading. CCL is now a leader in many sectors, but double-digit growth will be hard to achieve going forward. The expectation of a recession is also slowing down the appetite of investors for this growth darling. The latest dividend increase is a lot smaller too. The company has used leverage for its acquisitions many times in the past few years. Further acquisitions to support growth may get riskier as many expect a global economic slowdown. In the meantime, it’s definitely a keep for current shareholders.

Dividend Growth Perspective

CCL shows a nearly perfect dividend triangle with strong revenue and dividend growth over the past 5 years. CCL’s business model is built around repetitive orders generating consistent cash flow. With low payout ratios, you can expect dividend growth for many years. The latest increase ($0.01) was lower than what investors have been used too. Considering the economic impact of the covid-19, we now expect high single-digit dividend growth going forward.

Final Thoughts

You should not expect each stock to beat the market after only a few months. Some stocks may take 12 to 18 months to demonstrate they are worthy of your investment. As is often the case when investing, patience is the most essential element of our strategy.

You may also want to consider adding a Dividend Achiever to your portfolio. This list shows nearly 300 companies with more than ten consecutive years with a dividend increase.

No matter your pick, always proceed with due diligence and make sure your pick fits in your investment strategy.

The post Two Dividend Growth Picks that Could Boost Your Return! appeared first on The Dividend Guy Blog.