Almost every week, I’m trying to update you with what we have done so far with regards to our 12 month RV trip across Central and North America in 2016. So far, very few people around me know about my project. Besides my family and close friends, nobody is aware of what we do. I would say that half of them sometimes start their sentence with words like:

If you ever go…

and

If you don’t chose to go…

I guess it’s part of the game of doing things unconventionally; most people have a hard time understanding that you are actually going to do these things. It’s not that they disapprove; it’s more that they don’t understand what pushes a young man in his early 30’s to throw a well-paid job in the garbage, sell everything he has to live in a small cube with a steering wheel and 4 tires. I can’t blame them, I still remember watching a documentary about a very promising young man in the advertising field selling everything and quitting his super well paid job to buy a small farm and to raise sheep!

Another reason they might not understand is that I don’t really share the financial aspect of our project with them. Funny enough, I will give it all to you this morning ;-).

Paying off my Debts

The very first move I must do is to pay off all my debts before I go. They are listed as follow:

Credit card: $9,000

Line of credit: $19,000

Mortgage: $265,000

Car loan: $25,000

RV loan: $45,000

I’ve cleared all my consumer debts earlier in January with my year-end bonus. The 9K standing on my credit card is expense used to finance a part of our project. We had to buy several things for the RV and we also had to spend money on our house before we put it up for sale. Finally, our basement flooded in March which chewed up part of our savings as well. These are expenses I would not have if I didn’t plan on leaving.

It will be relatively easy to clear my debts once I sell my house as I should get about $365,000. I will use the equity in our house to pay off all our debts besides the car loan. This will leave me with $27,000 in my pocket and will sell my car for the remaining balance owed.

At that time, I will have no debts and $27,000 sitting in my bank account.

Liquid Assets $30,000-$35,000

Aside from selling my house, I also plan to have a few thousands on the side to add to my immediate liquid assets totaling between 30K and 35K. Each month, I buy shares of my employer’s stock and I will also count on a final year-end bonus to be paid in January 2016.

I know, $30K doesn’t seem like a big chunk of money for someone who plans on quitting his job and has a family to support. However, this represents 10 to 12 months of living on my “new budget”. As a second emergency fund, I will also count on an empty $20,000 line of credit.

I intend to invest the 30K or so in dividend stocks. This will not generate any interesting income (roughly $900 per year at 3%… not very interesting!), but I will not keep this money sleeping in my account while I travel!

Not So Liquid Asset $45,000

If things really turn sour, I can also count on my RRSP (my retirement account). I currently have 64K sitting there counting my wife’s account. If I ever had to withdraw money from this account, this would be 100% taxable income. This is why I consider $45,000 instead of $64,000.

The only reason I see I would dip in this pocket would be if I don’t sell my house before I leave. In my mind, there is no turning back and selling my house or not is not a factor in my decision. I want to do this trip so badly I don’t care if I have to cash out my retirement account, pay taxes to keep my house in good shape. I’ll obviously try to rent it if I can’t sell it but I’m the kind of guy who looks at the worst case scenario to make sure I’m ready to live with it.

I don’t count my pension plan in the “not so liquid asset” because even if I quit the bank, my pension plan won’t count as a liquid asset until I reach the age of 55. In the meantime, I would still have about 75K to manage + roughly 10K for my wife. Unfortunately, this is money I can’t even consider for my trip…

Income Source

I obviously have to find a way to generate income while I’m on the road. If I’d leave with only what is left in my bank account, I would come back 12 months later with almost nothing in hand but a half-burnt-off RV showing 100,000 miles. This doesn’t sound like a plan for a father of three!

In fact, I don’t expect to touch a single penny from the 30-35K I will put aside. I’m working very hard on my online business to make sure I can withdraw a salary big enough to pay off for all my expenses. I expect to spend between $2,500 and $3,000 per month depending where we live and what we do. If I’d leave tomorrow morning, I would be able to withdraw about $1,500 to $2,000 from my online company without hurting the business. I still have a long way to reach the $3,000, but it is highly feasible. About 6 months ago, I couldn’t withdraw more than $500!

I’m confident I will reach the 3K/month I need before I leave and think I will double this amount during the 12 months I’m on the road. I already plan on working near 30-40 hours/week on my online company while I travel. This should be enough to double the income I make and eventually make me financially independent for the rest of my life.

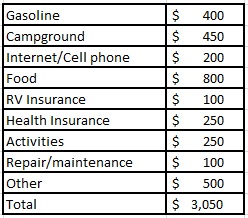

Budget

This is what my budget will look like while traveling:

Obviously, there are months where gasoline will go through the roof while we won’t even go to a single campground and other times, food costs will be much lower (especially once we leave the USA!). Therefore, the overall budget should look like the above mentioned chart but where I put my money will vary greatly. This is where the “other” section will come into play from time to time. To be more realistic, I should create a North American budget which will probably hit $3,500/month and a Central America that will definitely drop down around $2,000 to $2,500 per month.

This will be exciting to see how it goes. I guess the good news about it is that I’ll be earning US dollars while I travel.

Another Scenario

There is also another scenario I’m looking into. This is the scenario where I pay off my house, but keep my RV loan in order to have more liquid asset. With over 70K in my pocket, I would have enough to buy a rental property before I leave. My cash down would probably sufficient enough to generate a passive income while I’m on the road. I can expect to generate a net passive income around $300/month while my RV loan costs me $400/month.

I like the idea as it would make my life easier when I come back since I would have an asset that banks like. It would be easier to “restart” in the real world and I could probably live in my rental property for a while once I come back and keep my cost of living to its lowest level possible. I will only consider this scenario once I sell my house as I will clearly know how much I have in hand.

The last factor to consider is when I sell my house. If I’m lucky enough to sell it this fall, I could probably save around $2,000/month until I leave in May-June. This would also change my plan of buying a rental property or not!

What do you think of my financial plan so far, would you pay off all debts or go with scenario #2?