How can I spend so much? How my lifestyle has gone this far?

The very first step to financial freedom is definitely to know how much you need to live. This will set the bar and help you establish goals that must be reached if you want to become financially free one day. I’ve shared my thoughts on how I intend to reach financial freedom through 4 different ways. My biggest struggle to reach this has nothing to do with how much I make but rather how much I spend. A friend and fellow blogger, Dividend Growth Investor, asked me for more details about my budget. I thought it would be a good idea to share it with all of you so maybe you can help me find solutions where I didn’t see them.

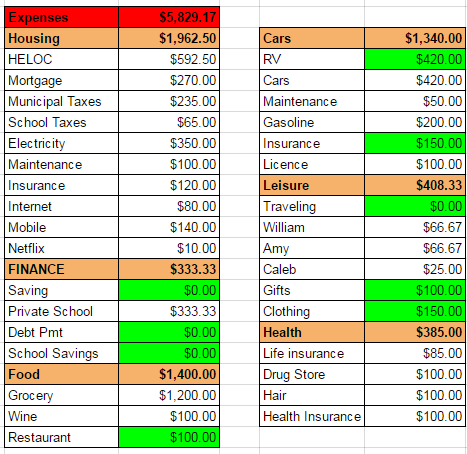

The Budget

I’ve done some extensive budgeting exercises recently. The reason is that I’m now working day and night to build sustainable income sources from my online ventures to never go back to work for the Man once I arrive home from my road trip. I tried to reduce my expenses to a minimum for a limited time to make sure I can live my dream of being an online entrepreneur. Here’s what I came up with for a “minimal budget”:

As you can see, I’m spending almost $6,000 per year and several categories are at “0” which is unsustainable for a long period of time. For example, I can’t expect to have nothing allocated for savings and debt repayment for a long period of time. I also have a zero budget for traveling and vacations. This means the first year I come back, I don’t plan to go anywhere. It’s a good thing I have an RV so we can do a few weekends that would not cost more than our regular living at home and still do something :-).

Further Analysis

Housing: possible savings $220-250

At first, we can say that living in our current house is expensive. After all, this represents 33% of my total budget. However, I include my internet and mobile phones (2) in this category. The HELOC payment represents the interest only payment on my home equity line of credit. Then again, this is not a sustainable budget as I will need to pay it off at one point. I have a small mortgage as well with a low payment. I currently owe a total of $290K on a $365K house. An interesting solution would be to sell my house and buy a smaller one. I could probably manage to buy something around $250,000 and have enough space for everybody. The mortgage payment would be relatively the same ($800-$900 per month), but I would save about $220-$250 in other fees (taxes, electricity, etc).

Finance: serious need to increase it

The finance section is more about savings and debt repayment acceleration. Once I get back from my road trip, I don’t expect to owe more than $10,000-$15,000 on my personal line of credit. At one point or another, I will need to pay it off and this is why I would like to allocate $500/month in short order.

My older son will go to a private high school. I know this is a big debate, but I take responsibility for my choice of sending my children to a private high school. I’ve seen with my own eyes the difference between both public and private schools while I was a kid and now as a parent. There is a huge difference in terms of resources, attitude and value between the two. I don’t think public school is bad, I think it’s okay. And I also believe private school is better. I know it’s not a great statistic, but all my friends from private school are all making a very good living in jobs they love while my friends from public school are all making less and don’t enjoy their work much.

Food: can’t go any lower

I think that by putting $100 in restaurants and $100 in wine, I can’t really go any lower. Feeding a family of 5 with $1,200 per month is also a minimum. Keep in mind that my two oldest children (soon to be 9 and 11) are eating as much as we do.

Car: possible savings: $500-$550

If I get to sell my RV, I will save on licence, payments and insurance. This would be a pretty good financial move. The only reason I put it in there is because I don’t know how much the RV will be worth. I have a $45K loan on the RV and I don’t know how much I will be able to sell it for once I come back from my road trip. If I can sell it and pay off my loan, I might consider it. On the other hand, the RV could be my means of cheap vacations for a few years. I expect to have one car for the family that I would need to buy and pay roughly $400/month. I might save a few bucks there, but it won’t make a big difference if I pay $30 more or less.

Leisure: minimal expenses

I’m a firm believer that children need to find their passion and enjoy life. This is why I allow my three children to do their activities. My oldest son is playing competitive soccer and my daughter is doing hip-hop dance. I expect a small budget for my 3rd kid as it is less expensive when you are 5 ;-).

Health: can’t cut on this!

I don’t think I can or should cut on health. I assume I’ll have to pay for a private health insurance mostly to cover dental care and a few other things. Since I live in Canada, the main health costs are already covered by my taxes.

In an Ideal World, I Would Need $7,700

While there are some places I can cut in my budget, my FI budget today is more $7,700. The point is not to spend more, but but allocate $1,300 in debt repayment and savings (emergency fund + school funding) per month. The remaining $575 or so would be used for family vacations and a little bit more restaurants

I know I will not need this much forever as the kids will leave the house, the mortgage will be paid and cars as well. I find that being in my 30’s is the worst time to save money since it seems I need to spend it everywhere in my budget. I think that if I can cut down on my expenses while maintaining a high level of revenues, I will be in a very strong position by the age of 40. Now, I want to concentrate on making $7,000 -$8,000 per month and pay down my debts as soon as possible. I’m seriously thinking of selling my house once I come back also, what do you think?