In September of 2017, I received slightly over $100K from my former employer, representing the commuted value of my pension plan. I decided to invest 100% of this money in dividend growth stocks.

Each month, I publish my results on those investments. I don’t do this to brag. I do this to show my readers that it is possible to build a lasting portfolio during all market conditions. Some months we might appear to underperform, but you must trust the process over the long term to evaluate our performance more accurately.

Recently, there were many DSR members who replied to my last newsletter about the “yield battle” between low yield high growth companies with a yield under 2% but with a generous dividend growth, and high-yielding companies offering a yield above 5%. Some also inquired about what we should do with the medium yielders with dividend yields of 2-5%.

To be clear: I’m a big fan of mixing medium yielders with 2-5% dividends with low-yield, high-growth stocks.

If you look at my portfolio, you will find that mix where there is a stable foundation from the “usual suspects” offering a decent yield. On top of that foundation, you will find the low-yield, high-growth stocks propelling my portfolio value higher.

There are obviously more candidates in this category but I have tried to select my favorites while also making a diverse selection across industries. The mid-yielders must offer a decent dividend, but also a decent dividend triangle. You will notice that some of them will look a lot like a low-yield, high-growth company and some will be closer to the high yielders. Today, I share this selection with you!

Performance in Review

Let’s start with the numbers as of February 5th 2024 (before the bell):

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Portfolio value: $243,431.98

- Dividends paid: $4,510.78 (TTM)

- Average yield: 1.85%

- 2023 performance: +20.69%

- SPY= +26.19%, XIU.TO = +11.87%

- Dividend growth: +1.7%

Total return since inception (Sep 2017-Dec 2023): 123.82%

Annualized return (since September 2017 – 77 months): 13.38%

SPDR® S&P 500 ETF Trust (SPY) annualized return (since Sept 2017): 13.31% (total return 122.90%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 8.99% (total return 73.75%)

Canadian Favorite Mid-Yielders (2-5%)

I thought it would have been easier to find 12 stocks in the Canadian market that would meet my criterion. But If I want to be a bit more diverse and not select just financial stocks and utilities, I had to dig a little bit more than expected.

Before we jump to the mid-yielders list, here’s a thought-provoking investment strategy that relies on low-yield, high dividend growth stocks for retirement.

Brookfield Infrastructure (BIPC)

The biggest downside of BIPC is its complex structure. However, management has delivered constant distribution increases for over a decade. They always give what they promise. BIPC is an “ETF” of utilities with its incredible diversification (from pipelines to data centers and electric transmission to railroads).

Brookfield Renewable (BEPC)

Similar to BIPC, Brookfield Renewable financial statements are complex, but the distribution increases don’t lie. The company shows ~50% of its assets in the hydroelectric industry and operates worldwide.

Canadian National Resources (CNQ.TO)

I could have selected Imperial Oil (IMO.TO) that is the other exception in the energy sector when it comes to dividend growth. CNQ owns high quality assets and its vertical integration allows it to make a profit at each step of the oil industry. It’s profitable even with a barrel of crude oil priced at $35-$40!

Fortis (FTS.TO)

Fortis is probably the most boring stock I own. 99% regulated, classic distribution and transmission energy company operating utility assets in North America and the Caribbean. With a stellar management team in place, the company has delivered 50 consecutive years of dividend increases. I won’t break records with this one in my book, but it will always participate in my retirement plan!

Granite REIT (GRT.UN.TO)

Here’s a rare REIT combining a decent yield with decent growth. Granite is still exposed to its major tenant (over 25% of assets leased to Magna International), but it has lowered this exposure each year. There is a high demand for industrial properties and Granite has a large development pipeline.

Intact Financial (IFC.TO)

Selecting IFC is almost cheating as it is very close to paying a yield under 2% and it definitely has the low-yield, high-growth profile. IFC is the largest player in Canada, giving them a large amount of data to optimize its underwriting process. The company also grows by acquisitions and now has a foot in the U.S. and in Europe.

Jamieson Wellness (JWEL.TO)

Be careful with JWEL. While its narrative (selling vitamins and nutriments to an aging population) and its numbers include consistent revenue growth and generous dividend increases making the company quite seductive. Jamieson Wellness, however, remains a small cap. You know it could go both ways for them. JWEL’s biggest challenge going forward will be to maintain its growth, but also to maintain its margins so it shows some EPS growth.

Magna International (MG.TO)

Magna is highly cyclical and if you invest in this one, be ready for a wild ride. While it’s one of the world’s largest auto parts makers, the automobile industries is subject to ups and downs on regular cycles. However, management has shown it was fast to act and able to expand margins while being under pressure.

National Bank (NA.TO)

One of my all-time favorites, National Bank, continues to be at the top of my bank rankings. NA shows the most generous dividend growth while maintaining the lowest payout ratio amongst the big 6. NA’s business is well diversified and since it’s the smallest of the big guys, it can usually be nimbler in its decision-making process.

Restaurant Brands (QSR.TO)

I can’t say I’m excited about Restaurant Brands, but I can’t say I found a major flaw either. The company operates iconic brands such as Burger King and Tim Hortons. It grows organically across the world and finds a few good brands to acquire periodically. It shows good stability.

Royal Bank (RY.TO)

Royal Bank is my second most favorite Canadian bank, mostly due to its size and diversification. The company generates only 50% of its revenue from classic banking activities. I think there is more money to be made in wealth management (considering the wealth transfer between boomers and the next generation) and in capital markets. In all honesty, I could have put more banks and a life insurance company on this list as well.

TMX Group (X.TO)

TMX operates a unique business model in Canada that is often ignored by many investors. The company operates a sticky business model with several recurring revenue streams from clearing trades and derivatives, to issuing shares/IPOs, providing training and being a data provider.

U.S. Favorite Mid-Yielders (2-5%)

This is probably where it was harder to make choices. The U.S. market is filled with great companies offering a decent yield and a good dividend triangle. Many other choices could have been part of this list. Here’s a short list of stocks that have been considered but are not included in this group: American Tower, Alexandria REIT, Colgate-Palmolive, CME Group, Cummins, Equinix (too close to a low yield), Honeywell, Hershey, Coca-Cola, McCormick, Nextera Energy, Bank OZK, Qualcomm, Robert Half, Texas Instruments, WEC Energy and Xcel Energy… phew!

AbbVie (ABBV)

Depending on the day you look at it, ABBV could be a high-yielder or a mid-yielder. Its stock price fluctuates greatly according to how well its drug pipeline is developing. It’s a classic story for many big pharmaceuticals. Fortunately, its aesthetic segment (driven by Botox) is offering more stability.

Automatic Data Processing (ADP)

This one is very close to being a low-yield, high-growth company and definitely has the profile with its very strong dividend triangle. ADP operates a nearly perfect business model where it combines both stickiness (employers are not changing their payroll system often) and recurring revenues (employers don’t stop paying their employees!). However, ADP faces a lot of competition and may also suffer setbacks during a recession.

Air Products and Chemical (APD)

You will rarely find a company in the Material sector with over 40 years of consecutive dividend increases. APD has a diverse way of positioning its business in a sector where most are stuck with commodity price fluctuations. As a provider of industrial gases, APD signs long-term contracts with its customers. It provides a crucial element for many businesses which makes their business model both sticky and recurring.

BlackRock (BLK)

BlackRock is the largest asset manager and the largest ETF manufacturer in the world. Their size alone ensures stability and organic growth. While BLK stocks will fluctuate according to Mr. Market’s mood, it can count on its long-time relationship with institutional investors.

Genuine Parts (GPC)

Genuine Parts is the type of business you buy, and you forget about. It provides car repair parts across North America and it is now growing in Europe. GPC is known to grow both organically and through a series of small acquisitions in a highly fragmented market. It’s not an exciting company, but it surely does something right with its more than 60 consecutive years of dividend increases.

Home Depot (HD)

This is another company that could fit in the low-yield, high-growth model (you can see I’m not trying to cheat and show weaker stocks in the mid-yielder section!). HD is the world’s largest home improvement retailer, with more than $150B in sales. HD has built a strong relationship with PRO builders as it can make everything they need available when they need it. As we expect lower interest rates later this year, this may give a small boost to the construction industry, and improve HD’s results as well.

Johnson & Johnson (JNJ)

JNJ is one of the first stocks I bought when I switched my strategy over to dividend growers. It’s definitely a classic selection that doesn’t get old. JNJ makes most of its profit from its pharmaceutical division that specializes in specialty drugs, which makes it difficult for generic drug manufacturers to compete. I think JNJ’s Pharma segment continues to offer a promising outlook due to strong prospects on existing key drugs such as Stelara, Imbruvica, and Darzalex, along with a robust drug pipeline of 14 novel drugs.

Lockheed Martin (LMT)

There were some great candidates in the defense industry, but I decided to go with one of the largest players. Lockheed has the largest military contract with the Pentagon with its F-35 program. It has been able to consistently offer growth and increase its dividend. With political tension growing, I expect LMT to leverage its expertise in defense across the world.

McDonald’s (MCD)

MCD is definitely a classic on the U.S. landscape with over 40 consecutive dividend increases. MCD enjoys strong brand recognition and is the world’s largest fast-food retailer. MCD is attentive to its customers and has introduced many changes to its menu over the years, such as all-day breakfast and healthier options. Management came with a strong and ambitious growth plan for the coming years, and I’m convinced they will do well!

I have covered more in-depth ADP, HD and MCD in the video below:

PepsiCo (PEP)

PepsiCo has been in the middle of a lot of noise as of late. First, Ozempic (a drug now used to fight obesity) will prevent millions of consumers from eating Doritos and drinking soft beverages going forward. Second, Carrefour is the first in a long line of merchants that will ban all their products. You can guess that I’m being a bit sarcastic here. PepsiCo benefits from strong non-carbonated drink brands such as Gatorade and Tropicana. PEP’s snack division is a strong leader in this industry with a 64% market share in the U.S., 60% of Brazil’s market, and 46% of the U.K. market.

Procter & Gamble (PG)

I could plead guilty for a lack of original choice, but why go for something exotic when good old classic consumer stocks work? PG is a truly diversified fund, with its 21 brands each grossing over $1B, in 5 segments, sold in over 180 countries. Procter & Gamble is probably more stable than most bonds and pays a decent yield. There are no immediate threats that come to mind that will jeopardize its dividend in the future.

Starbucks (SBUX)

Starbucks is a good example of what a low-yield, high-growth company looks like after its fast growth period is over. While SBUX can continue to grow organically in North America and shows interesting growth potential in Asia, they are far from the company they were 10 years ago. Nonetheless, I expect SBUX to maintain a generous dividend growth policy and maintain a mid to high single-digit growth rate for revenue and earnings going forward. Consumers proved their love for Starbucks coffee despite recessions and inflation in the past!

Smith Manoeuvre Update

Slowly but surely, the portfolio is taking shape with 10 companies spread across 7 sectors. My goal is to build a portfolio generating 4-5% in yield across 15 positions. I will continue to add new stock monthly until I reach that goal. My current yield is 5.04%.

Adding more of Canadian Tire (CTC.A.TO)

It’s relatively hard to find new ideas offering a yield above 4% that is not in the energy or REIT sector these days. Since Canadian Tires was my smallest position, I used my $500 to help balance my portfolio a little by buying additional shares. I get more exposure to the consumer discretionary sector by adding shares of this depressed stock. Since my goal is to keep my Smith Manoeuvre portfolio for over 10 years, I don’t mind a little volatility!

Here’s my SM portfolio as of February 5th, 2024 (before the bell):

| Company Name | Ticker | Sector | Market Value |

| Brookfield Infrastructure | BIPC.TO | Utilities | $969.80 |

| Canadian National Resources | CNQ.TO | Energy | $897.82 |

| Capital Power | CPX.TO | Utilities | $558.82 |

| Canadian Tire | CTA.A.TO | Consumer Disc. | $1,024.24 |

| Exchange Income | EIF.TO | Industrials | $1,039.72 |

| Great-West Lifeco | GWO.TO | Financials | $758.88 |

| National Bank | NA.TO | Financials | $616.20 |

| Nutrien | NTR.TO | Materials | $892.32 |

| Telus | T.TO | Communications | $905.92 |

| TD Bank | TD.TO | Financials | $1,135.40 |

| Cash (Margin) | -$50.24 | ||

| Total | $8,748.66 | ||

| Amount borrowed | -$8,500.00 |

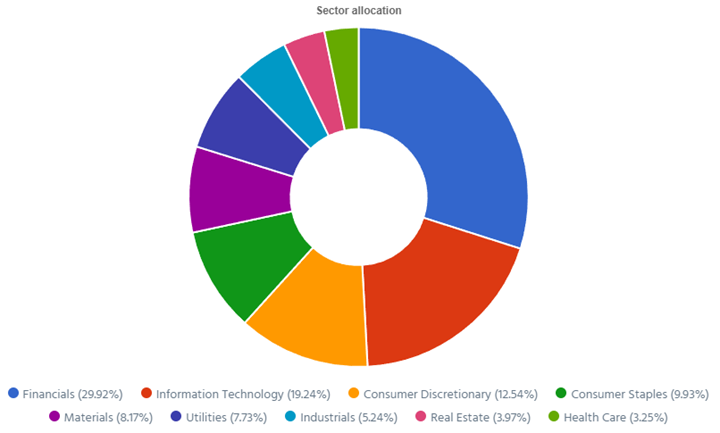

Let’s look at my CDN portfolio. Numbers are as of February 5th, 2024 (before the bell):

Canadian Portfolio (CAD)

| Company Name | Ticker | Sector | Market Value |

| Alimentation Couche-Tard | ATD.B.TO | Cons. Staples | $23,937.94 |

| Brookfield Renewable | BEPC.TO | Utilities | $9,422.16 |

| CCL Industries | CCL.B.TO | Materials | $8,015.00 |

| Fortis | FTS.TO | Utilities | $9,211.77 |

| Granite REIT | GRT.UN.TO | Real Estate | $9,568.00 |

| Magna International | MG.TO | Cons. Discre. | $5,369.00 |

| National Bank | NA.TO | Financials | $12,426.70 |

| Royal Bank | RY.TO | Financial | $8,529.30 |

| Stella Jones | SJ.TO | Materials | 11,675.62 |

| Cash | $436.71 | ||

| Total | $98,592.20 |

My account shows a variation of -$1,592.11 (-1.59%) since the last income report on January 9th.

Since most companies will report during February, I’ll wait for next month to do a big review.

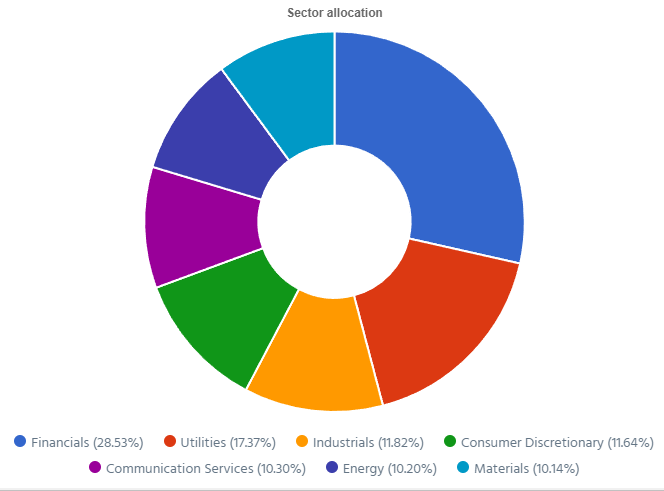

Here’s my US portfolio now. Numbers are as of January 9th, 2024:

U.S. Portfolio (USD)

| Company Name | Ticker | Sector | Market Value |

| Apple | AAPL | Inf. Technology | $7,434.00 |

| Automatic Data Processing | ADP | Industrials | $89,454.78 |

| BlackRock | BLK | Financials | $11,032.00 |

| Brookfield Corp. | BN | Financials | $13,435.31 |

| Home Depot | HD | Cons. Discret. | $10,716.90 |

| LeMaitre Vascular | LMAT | Healthcare | $5,870.00 |

| Microsoft | MSFT | Inf. Technology | $19,327.34 |

| Starbucks | SBUX | Cons. Discret. | $7,904.15 |

| Texas Instruments | TXN | Inf. Technology | $7,960.00 |

| Visa | V | Financials | $13,859.00 |

| Cash | $247.58 | ||

| Total | $107,241.06 |

My account shows a variation of +$2,604.57 (+2.50%) since the last income report on January 9th.

There were lots of companies reporting earnings over the past 30 days. Let’s review what they did!

Apple has some issues in China

02-01-2024, Apple reported a decent quarter with revenue up 2% and EPS up 16%, but the market was more concerned about China. Sales from China were $20.8B during the period, which was well below the $23.5B that analysts had expected and also showed a 4th consecutive quarter of sales declines. Here’s the sales breakdown by segments: iPhone: $69.7B (+6.0 % Y/Y); Mac: $7.78B (0.5 % Y/Y); iPad: $7.02B (-25.2 % Y/Y); Wearables, Home and Accessories: $11.95B (-11.4 % Y/Y); Services: $23.12B (+11.4 % Y/Y). It was a bit of a hit-and-miss quarter depending on the segment. AAPL generated nearly $40B in operating cash flow this past quarter.

Automatic Data Processing: strong quarter, strong guidance!

ADP reported another strong quarter with revenue up 6% and EPS up 9%, and beating analysts’ expectations. Employer Services revenue increased by 8% and PEO Services (employment administration outsourcing solutions) revenue increased by 3%. Management reaffirmed its guidance for 2024: revenue growth to be between 6 and 7% and adjusted EPS should be up by 10 to 12%. Guidance includes Employer services revenue growth of 7 to 8% while PEO services revenue is expected to grow by 3 to 4%.

BlackRock sees its dividend safety score drop!

Blackrock reported a solid quarter with revenue up 7% and EPS up 8% which handily beat analysts’ expectations. The company also agreed to acquire Global Infrastructure Partners to create a combined infrastructure platform of more than $150B and is reorganizing some of its other platforms including its Aladdin investment tech platform and illiquid alternative investments. Another good news item was their long-term quarterly net inflows were $95.6B, versus $3B of net inflows in Q3. BLK increased its dividend by a meager 2% so we had to decrease its dividend safety score from 4 to 3.

Starbucks brews more growth

Starbucks reported a good quarter with revenue up 8% and EPS up 20%. Global comparable store sales rose 5%. The average sales ticket value was up 2% and the overall transaction count was 3% higher during the quarter. In North America, operating margins jumped to 21.4% of sales in the region from 18.5% a year ago, primarily driven by in-store operational efficiencies and sales leverage. Active membership in Starbucks Rewards in the U.S. rose 13% to 34.3M during the quarter. In China, sales increased by 10% but the operating margin decreased from 14.3% to 13.1% due to higher wages and benefits. SBUX opened 549 net new stores so their growth story continues to evolve.

Texas Instruments hit a roadblock

Texas Instruments disappointed the market with declining numbers (revenue down 13%, and EPS down 33%). Results were affected by declining demand from both industrial and automotive industries. This is one more sign telling us a recession may be looming. Over the past 12 months, TXN generated $6.4B from operating cash flow and $1.3B in free cash flow. The company pays a little more than $4.5B in dividends per year. It means we could see a dividend growth policy slow down this year. We will follow the coming quarters with great attention.

Visa drives volume no matter what

Visa reported another solid quarter (what’s new?) with revenue up 9% and EPS up 25%. Payment’s volume increased 8% Y/Y in constant dollars with cross-border volume up 16% and processed transactions rising 9%. That compares with Q4 payments volume growth of 9%, cross-border volume growth of 16%, and processed transactions growth of 10%. While we expect the economy to slow down, it seems Visa continues to enjoy strong volumes.

My Entire Portfolio Updated for Q4 2023

Each quarter we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our very special additional service called DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF showing all the information about all my holdings. Results have been updated as of January 10th, 2024.

Download my portfolio Q3 2023 report.

Dividend Income: $53.43 CAD (-60% vs January 2023)

This is quite ironic that my dividend payment is down 60% vs last year, but my portfolio value is way higher (+32K or up 15%). That’s because I received my last dividends from Algonquin in early 2023 and sold my shares right after.

I guess that’s a good example of how you can improve your portfolio’s health by saying “no” to bad income!

Dividend growth (over the past 12 months):

- Granite: +3.10%

- Disney: a small parting gift ?

- Currency: +2%

Canadian Holding payouts: $35.20 CAD.

- Granite: $35.20

U.S. Holding payouts: $13.50 USD.

- Disney: $13.50

Total payouts: $53.43 CAD.

*I used a USD/CAD conversion rate of 1.3506

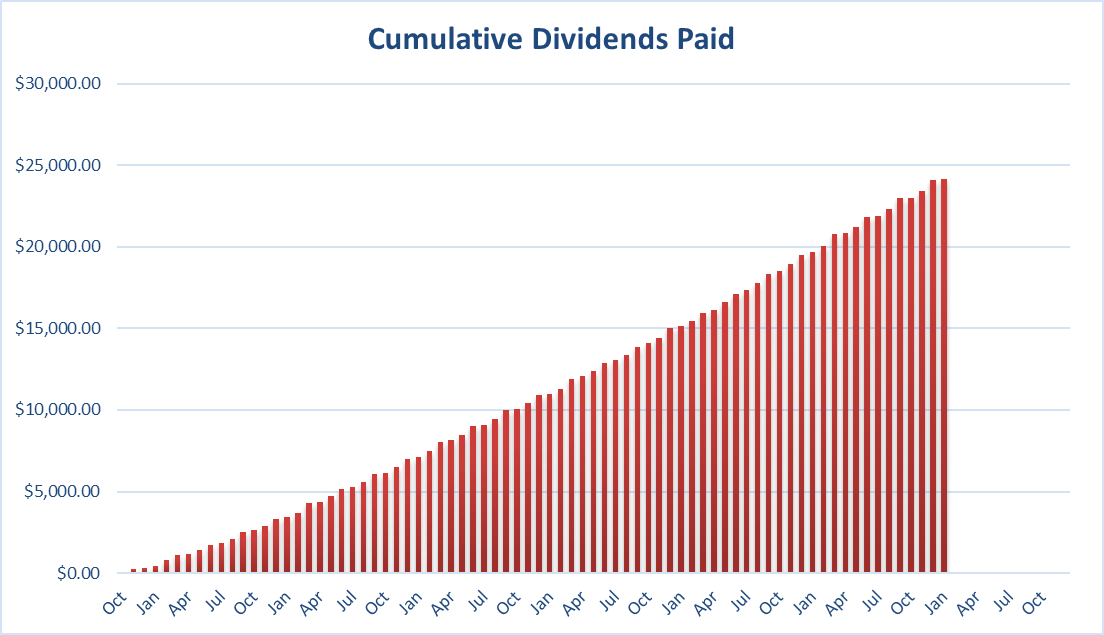

Since I started this portfolio in September 2017, I have received a total of $24,166.93 CAD in dividends. Keep in mind that this is a “pure dividend growth portfolio” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth is coming from the stocks and not from any additional capital being added to the account.

Final Thoughts

There will be a lot of information to digest in February and March as more earnings reports come in. Don’t make rash decisions. Often, stocks will move by 5-10% on earnings day. Trying to make a play on that day is playing against institutional traders who already have their trade instructions planned for many scenarios. By the time you read and analyze the new information, the trades have been accomplished way before you focus your eyes on your brokerage account.

It’s best to take a deep breath and read the reports a few days (or even a month!) after they come out.

Less stress = better decisions!

Cheers,

Mike.

The post Favorite Mid-Yielders – January Dividend Income Report appeared first on The Dividend Guy Blog.