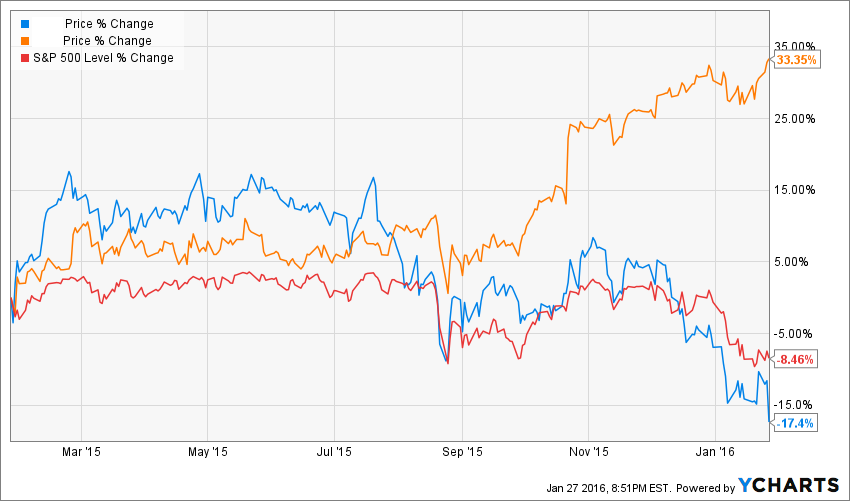

During the month of January, we were submerged by a wave of financial results. I truly appreciate earnings season as it gives me the true color of what is really going on out there. However, we don’t all understand financial results the same way. Two companies are currently heading toward very different trends. Take a look at this: I am not going to tell you which one is which, just for the sake of the exercise.

As you can see, one clearly beat the S&P 500 over the past 12 months and the other one is seriously trailing behind. For the record; both companies are leaders in their industry and are paying dividends. Let’s try to understand by looking at each company’s fundamentals why there is so much love for one company and so much hate for the other one.

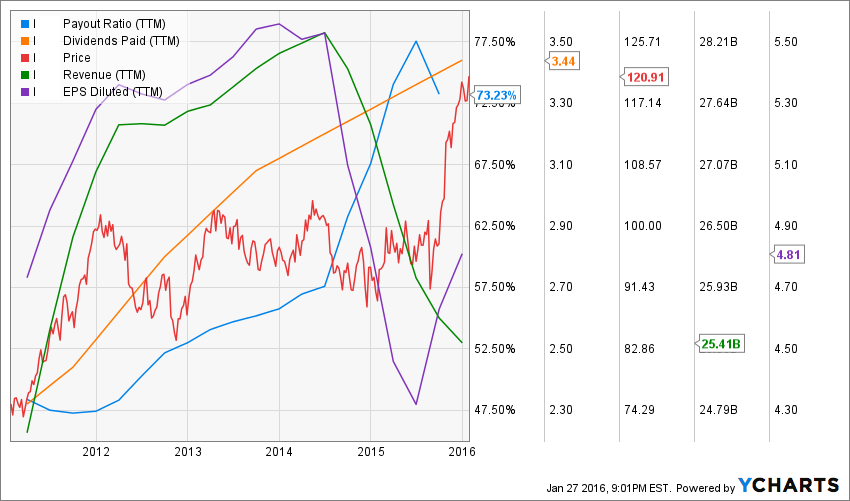

A closer look at the “Loved One”

The first company shows the following metrics for the past 5 years:

5 year revenue growth: 1.09%

5 year earnings growth: 1.48%

5 year of dividend growth: 8.77%

Current dividend yield: 2.85%

Payout ratio: 73.23%

Cash payout ratio: 69.23%

PE ratio: 25.14

At first, it doesn’t look like a superpowered dividend growth stock to me. While the 5 year dividend growth rate is very interesting, you can tell that with a payout ratio near 75% and both anemic revenue and earnings growth over the past 5 years, there is the beginning of a problem here. It doesn’t get any better when you look at the 5 year trends:

A closer look at the “Hated One”:

The hated company shows the following metrics for the past 5 years:

5 year revenue growth: 29.08%

5 year earnings growth: 33.61%

3 year of dividend growth: 73.58%

Current dividend yield: 2.17%

Payout ratio: 21.65%

Cash payout ratio: 16.57%

PE ratio: 10.16

Hum… this is getting interesting. As you can see, the second company is showing stellar numbers. In fact, it’s almost too good to be true! Please note that the company has been paying dividends for only 3 years though… but still the 5 year metrics trends looks very good:

So without knowing which one is which don’t tell me you would jump on the first company like it’s the last cake on the shelf on your kid’s birthday???

Have you guessed yet?

All right…. I agree with you, metrics are nothing without context, but still I needed to show you the numbers before I talked about the companies itself. So here we go!

The first company is McDonald’s (MCD) and the second one is…. Apple (AAPL)!

McDonald’s is the loved one for the past 12 months and everybody seems to hate Apple… let’s try to understand why!

On one side, we have a dividend paying monument, leader in its industry that is finally showing some signs that the future is not that dark. McDonald’s has multiplied different strategies to retain their clients and improve their sales. So far, their efforts have led to nothing and this is why I decided to sell the stock about 18 months ago. Well, I guess my timing sucks! However, I don’t regret the sale as I still don’t believe that making gourmet burger and serving clients at their tables will make Mickey D the new Starbucks of fast food restaurants. However, I must admit that serving breakfast (the most profitable meal at McDonald’s) all day long was a great idea. However, I really don’t see where there is so much hype for a company that has been searching for a solution to increase its revenues for a good 5 years and hasn’t come up with any solid ideas.

On the other side, we have Apple who is currently suffering from the perfect kid syndrome. No matter how great their results are, it’s never enough. When Apple posted their latest results, I even read in an article that the company only sold 74.8 million phones… Yeah… the company has unbelievable numbers, but just because the 2015 1st quarter was better (in terms of units sold and total revenues) the stock dropped 6% after their announcement. I’m not sure I get it as to me, it seems the company is showing flat sales (but increasing earnings, nobody noticed that!) in a difficult economy. It’s not like the iPhone was losing market share as Blackberry once did. The company remains dominant in the smartphone business, no doubt about it.

Final Thoughts

The point behind all this I guess is that it’s not a matter of how good you are, but how good people think you should be. Expectations are sometimes more important than real results. Nonetheless, I’m still holding on to my AAPL shares and I don’t regret selling MCD back in 2014!

What do you think? Do you think MCD is worth it at 25 times its earning compared to AAPL at 10 times?

disclaimer: I own shares of AAPL