In September of 2017, I received slightly over $100K from my former employer, which represented the commuted value of my pension plan. I decided to invest 100% of this money in dividend growth stocks.

Each month, I publish my results on those investments. I don’t do this to brag. I do this to show my readers that it is possible to build a lasting portfolio during all sorts of market conditions. Some months we might appear to underperform, but you must trust the process over the long term to evaluate our performance more accurately.

Performance in Review

Let’s start with the numbers as of June 24th, 2022 (after the market closes):

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Portfolio value: $298,288.55

- Dividends paid: $4,196.36 (TTM)

- Average yield: 2.11%

- 2021 performance: +16.78%

- SPY= 28.75%, XIU.TO = 28.05%

- Dividend growth: +3.14%

Total return since inception (Sep 2017- June 2022): 82.32%

Annualized return (since September 2017 – 57 months): 13.48%

SPDR® S&P 500 ETF Trust (SPY) annualized return (since Sept 2017): 11.32% (total return 66.45%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 8.56% (total return 47.69%)

Sector allocation calculated by DSR PRO

What a Down Market Means to Investors?

Today I wanted to focus our attention on the different realities each type of investor goes through when markets are negative. For the sake of discussion, I’ll separate investors into three categories classified by age:

- Young to mid-life investors (20 to 50)

- About to retire investors (51 to 65)

- Retiree’s investors (65+, but I guess it could be 51 to 99, but you get the point).

We keep saying it’s a good time to invest when the market is down.

“Buy the dip.”

If you are a young to a mid-life investor investing periodically, this is the best time of your life. As the market drops, you can buy more shares and build up your retirement nest egg. We often mention that a sizeable number of returns can be generated during those periods. As markets are cyclical, downturns are followed by bullish markets. Generally, the “analysis” of investing during a down market stops with “buy the dip.”

But that reality is only valid if you invest more money in the market each paycheck, each month, or each year. Therefore, “buy the dip” sounds like valid advice for those who are about to retire too. The problem is that many investors think they should modify their investment strategy when they are about to retire. They should lower their exposure to equities and “secure” their portfolio.

If you are in this situation now and are looking at selling stocks to buy more bonds or other fixed income, you probably don’t feel good selling stocks 20% down from their peak values. What if there was another alternative?

Changing asset allocation is probably premature for those in their 50s who are still adding capital to their portfolio. Technically, you still have 30-35 years (maybe 40!) in front of you. This means you will go through another 3 or 4 full economic cycles (including more bear markets and more bull markets). Why would you want to slow down now while you still have ~10 years to add more capital?

Buying the dip isn’t obvious to you, and I get that. What is important at this point is to reassess your risk tolerance. If it’s too much to take in, now is still the time to reallocate your capital into a more secure portfolio. However, if you do that, make sure to never increase your exposure to equity again. Too often, I’ve seen “growth” investors during bear markets that become “conservative” after losing 10-20%.

This type of risk tolerance bipolarity will lead to “sell low, buy high”. If you can’t take market fluctuations, this is fine. After all, the best investing strategy is the one helping you sleep well at night. But if you go for security, don’t come back once the market bounced up by 25% in a few months or years. Write yourself a note to open in case of a market emergency to remind yourself how you feel when you lose money.

What “Buy the dip” means for retirees?

I often feel that we forget to talk to retirees when the market goes down. You worked all your life and made numerous sacrifices to save and invest money. Now is the time to enjoy the fruits of your labor. You can’t buy the dip since you are not adding capital to your portfolio. Chances are you are withdrawing from it. What options do you have when there are discounts but you have no money to purchase? You get back to your plan and make sure you follow it! Speaking of plans, how do you generate your income at retirement:

Do you go for a high yield or make your own dividends?

Recently, I updated our two newsletters about retirement and withdrawal mechanics (exclusive to Dividend Stocks Rock members). There was a part about the concept of portfolio income. Your portfolio can generate enough dividends to retire on the yield alone. This strategy usually requires you to build a large portfolio or invest in high dividend-yield stocks.

If you opt for that strategy and enter a bear market, you shouldn’t worry much. If you did your due diligence, the companies in your portfolio should continue to do well and will keep up with their distributions. Your concern is ensuring all companies have a solid dividend safety score. While portfolios may go down, I doubt companies like Royal Bank or Coca-Cola will cut their dividend in 2022. By focusing on your portfolio income, you can avoid all the noise. But please make sure you have reviewed each of your holdings to make sure they are ready to face a recession (high-yielders are not paying guaranteed income!).

What if you must sell shares to generate your retirement income?

The second option retirees use to generate enough income to retire is to use a mix of dividends and capital gains (e.g., selling some shares) to support their lifestyle. This technique is also named “make your own dividend.” In all transparency, this is the strategy I intend to use in retirement. It’s not a secret that I prefer building a portfolio of strong dividend growers that will generate a lower yield but offer a higher potential total return.

My retirement newsletter suggested keeping a cash reserve if you use this strategy. You don’t want to sell shares when their price is down. Therefore, you don’t need to sell shares during most bear markets with a cash reserve of 12 to 24 months. This reserve will last even longer, considering you will receive monthly dividend payments.

The reserve is particularly important in a year like 2022. Imagine a portfolio generating a 2% yield and you need 4% of your portfolio per year to support your retirement. If your portfolio value is down by 15%, this means you will likely end the year at -17% (15% drop minus another 2% in capital withdrawals). Your portfolio will melt fast at this pace, which is enough to give you headaches.

Imagine you have a 6% cash reserve (the equivalent of 18 months of withdrawals). Throughout 2022, you withdraw from your cash reserve (-4%), but you receive 2% in dividends. At the end of the year, your cash reserve will still be good for another 12 months (6% – 4% + 2% = 4%). Imagine we are in a clear market rut and 2023 isn’t any better. This strategy will allow you to go through 2023 without selling a single share. At the end of the year, you would still be left with a cash reserve of 6 months or 2% (4% – 4% + 2%).

In general, most bear markets will recover within 24 months. If it’s a big bad one, you will have avoided the worst with your cash reserve and will start selling shares as the market is recovering.

Your statement says you’re down 15%, but what does your retirement plan say?

Focusing on your plan and your strategy is crucial to avoid emotional decisions and panic selling. Your statement may show a negative value, but your retirement plan shouldn’t have been based on a 10%+ annual return.

If you are 100% in equities as I am, you should target something around a 6.5% to 7% annualized growth rate. Anything above that is gravy (and could come and go). This pension portfolio showed a 19% annualized growth rate not too long ago. Today, I’m still way above 6.5%, but I would have been very disappointed if I had taken a 12% to 15% rate for granted.

If you plan well and stick to your investment strategy, this uncomfortable yet cyclical and temporary situation will not hurt your retirement situation. In the end, even if you are retired today, you will likely go through a couple more bears and bulls before you have no money to invest. Your plan should be followed for decades, not for just a few months.

Keep that in mind next time you look at your portfolio.

Smith Manoeuvre Update

If there is one positive note to this market downturn: I’m investing more monthly each month! It’s not much, but the feeling of investing while the market down always seems to be a good one. For this month, the $500 will go to Brookfield Infrastructure (BIPC.TO). You’ll get the detail of this transaction upon my return from Africa ?.

I’ve wanted to invest in this security for a while now. While there are other companies offering a better yield, BIPC will bring solid diversification in my portfolio. BIP has built an impressive infrastructure portfolio through various business segments: utilities, transportation, energy, and data infrastructure. BIP manages 2,700km of regulated natural gas pipelines, 2,000km of electricity transmission lines, 32,300km of railroads, 4,000km of toll roads, 13 ports,16,500km of natural gas pipelines, 20,000km of fiber backbone and 52 data centers. Brookfield has ample liquidity and no significant debt maturities over the next 5 years, and it is backed by Brookfield Assets Management (BAM). BIP has been around for a while and offers a generous dividend growth policy (5% to 9%). This is clearly a “go-to” stock if you are looking for income.

Here’s my portfolio as of June 24th, 2022 (after the market closes):

| Company Name | Ticker | Sector | Market Value |

| Canadian Net REIT | NET.UN. V | Real Estate | $421.60 |

| National Bank | NA.TO | Financials | $501.60 |

| Exchange Income | EIF.TO | Industrials | $467.61 |

| Brookfield Infrastructure | BIPC.TO | Utilities | TBA |

| Cash (Margin) | -25.22 | ||

| Total | $1,365.59 | ||

| Amount borrowed | -$2,000.00 |

Let’s look at my CDN portfolio. Numbers are as of June 24th, 2022 (after the market closes):

Canadian Portfolio (CAD)

| Company Name | Ticker | Sector | Market Value |

| Algonquin Power & Utilities | AQN.TO | Utilities | $7,447.62 |

| Alimentation Couche-Tard | ATD.B.TO | Cons. Staples | $19,806.03 |

| National Bank | NA.TO | Financials | $10,115.60 |

| Royal Bank | RY.TO | Financial | $7,460.40 |

| Brookfield Renewable | BEPC.TO | Utilities | $6,631.23 |

| CAE | CAE.TO | Industrials | $6,428.00 |

| Enbridge | ENB.TO | Energy | $8,669.85 |

| Fortis | FTS.TO | Utilities | $5,917.23 |

| Magna International | MG.TO | Cons. Discre. | $5,222.70 |

| Sylogist | SYZ.TO | Inf. Technology | $2,994.06 |

| Granite REIT | GRT.UN.TO | Real Estate | $10,119.68 |

| Cash | 96.21 | ||

| Total | $90,908.61 |

My account shows a variation of -$6,192.69 (-6.4%) since the last income report on June 3rd. During June, I used my dividend payments and added 78 shares of Algonquin Power (AQN) at an average price of $17.89. The goal was to increase my exposure to utilities and boost my dividend income. Adding more Magna International would also have been a good idea, but I was limited by the investment amount!

Here’s my US portfolio now. Numbers are as of June 24th, 2022 (after the market closes):

U.S. Portfolio (USD)

| Company Name | Ticker | Sector | Market Value |

| Activision Blizzard | ATVI | Communications | $9,041.04 |

| Apple | AAPL | Inf. Technology | $10,624.50 |

| BlackRock | BLK | Financials | $9,068.92 |

| Disney | DIS | Communications | $4,400.10 |

| Gentex | GNTX | Cons. Discret. | $6,706.90 |

| Microsoft | MSFT | Inf. Technology | $14,723.50 |

| Starbucks | SBUX | Cons. Discret. | $6,639.35 |

| Texas Instruments | TXN | Inf. Technology | $7,797.50 |

| VF Corporation | VFC | Cons. Discret. | $3,888.81 |

| Visa | V | Inf. Technology | $10,275.50 |

| Cash | $113.29 | ||

| Total | $83,279.41 |

The US total value account shows a variation of -$3,780.12 (-4.4%) since the last income report on June 3rd.

My Entire Portfolio Updated for Q2 2022

Each quarter, we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our special additional service, DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year, and I wanted to share my DSR PRO report for this portfolio. You can download the full PDF showing all the information about all my holdings. Results have been updated as of July 7th, 2022.

Download my portfolio Q2 2022 report.

Dividend Income: $485.09 CAD (-5% vs June 2021)

Please note that I’m not really down by 5% this month. Since I’ll be hiking the Kilimanjaro while you read this update, I had to write my monthly report on June 24th. I’m still waiting for my Magna International dividend payment. Last year, I received $35.91 from Magna. Therefore, considering this dividend payment, I’m up 2% vs. last year. Last year, I also received $57.60 from Intertape Polymer, which was sold with a great profit earlier this year.

Here are the detail of my dividend payments.

Dividend growth (over the past 12 months):

- Enbridge: +3%

- Fortis: +6%

- Granite REIT: new

- Sylogist: 0%

- Visa: +17%

- Microsoft: +1.5%

- VFC: +2%

- BlackRock: +18%

- Currency factor: +5.73%

Canadian Holding payouts: $276.63 CAD

- Enbridge: $138.46

- Fortis: $52.97

- Granite REIT: $33.07

- Sylogist: $52.13

U.S. Holding payouts: $161.67 USD

- Visa: $18.75

- Microsoft: $34.10

- VFC: $40.50

- BlackRock: $68.32

Total payouts: $485.09 CAD

*I used a USD/CAD conversion rate of 1.2894

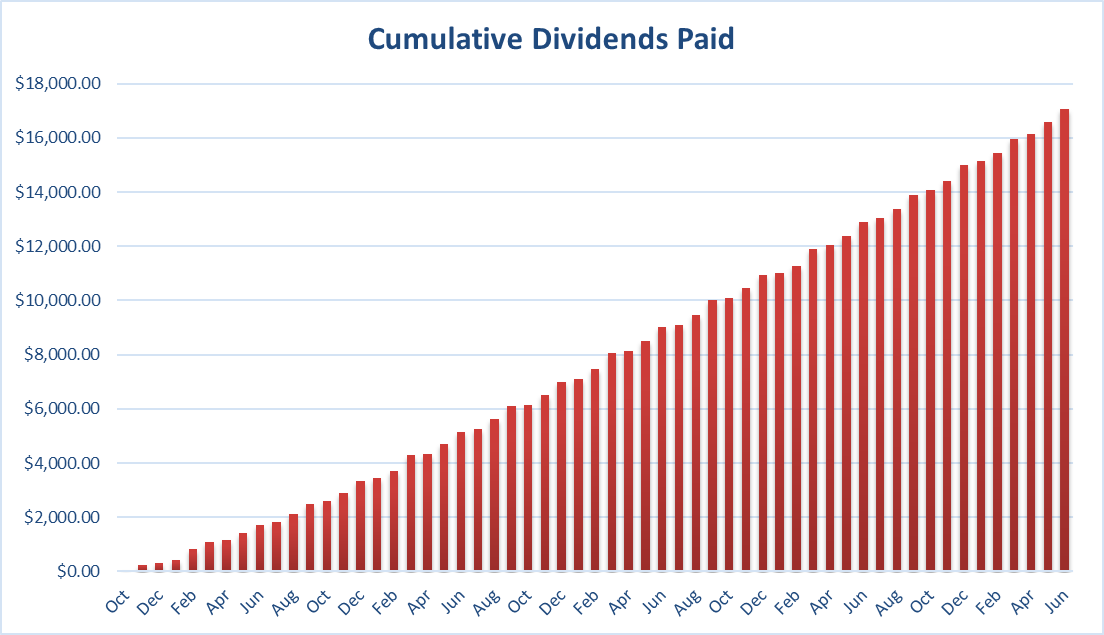

Since I started this portfolio in September 2017, I have received a total of $17,074.49 CAD in dividends. Remember that this is a “pure dividend growth portfolio” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth comes from the stocks and not from any additional capital added to the account.

Final Thoughts

As you read this, I’m in the middle of the final push to climb Mount Kilimanjaro. I can’t wait to return home and tell you more about this experience! I often compare investing with hiking, and I’m sure I’ll have more analogies upon my return.

So, here’s the first thought: I’m currently far away and completely disconnected from the real world (the first time in 5 years I don’t have access to any kind of network!). I don’t know what is happening on the market, but I know one thing; companies in my portfolios continue to make sales, generate profits, and pay dividends. Having this certitude is key during market fluctuations, and not looking at my portfolio for a while will certainly help!

Cheers,

Mike.

The post What a Down Market Means to Investors – June Dividend Income Report appeared first on The Dividend Guy Blog.