Wal-Mart just released its third quarter results with a great performance. To be honest, I think we were many to doubt about WMT’s ability to generate growth before the Holiday season.

We will go through the main highlights of their reports, but first, we will analyze what Wal-Mart has been doing over the past five years and determine whether or not it should be part of your dividend portfolio. Let’s see if “Save Money, Live Better” can translate into “Make Money, Invest Better”!

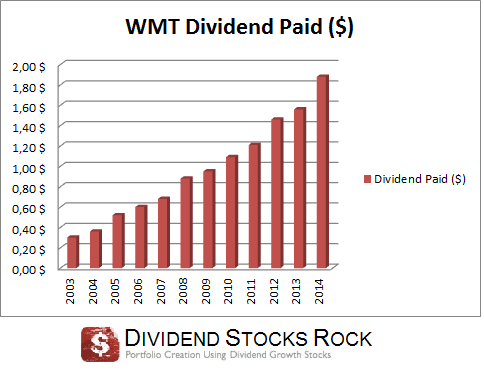

This dividend aristocrat has increased its dividend for 41 consecutive years. Over the past ten years, the dividend doubled more than twice! The dividend paid back in 2004 was $0.36/share and WMT will pay $1.88/share to shareholders this year. However, lately WMT has struggled to show solid growth and deals with high margin pressures.

Business Model

Wal-Mart Stores Inc, operates retail stores in various formats under various banners. Its operations include three reporting business segments, Walmart U.S., Walmart International and Sam’s Club in three categories retail, wholesale and others.

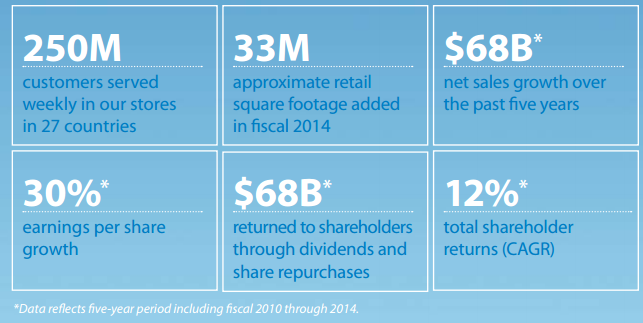

Here are a few numbers to show you how big Wal-Mart is:

The company has put several initiatives into action to increase sales with a more complete food offering, electronic departments’ new look and a massive investment in e-commerce. The battle in e-commerce is far from being a walk in the park as Wal-Mart will compete against Amazon, the champion of volume and recurring losses. It’s hard to compete against a giant who doesn’t care about profits for the sake of growth. In the brick-and-mortar industry, the consolidation of dollar stores also brings more powerful competitors. Yet, WMT remains the biggest retailer in America.

Now let’s go dive further into the numbers. Following the first 4 Dividend Stocks Rock Investing Principles, I’ll take a look at Wal-Mart and share a full dividend analysis.

Principle #1 High Dividend Yield Doesn’t Equal High Returns

Did you know that the highest dividend yield stocks underperform more “reasonable” yielding stocks? The Hartford Mutual Funds company wrote:

The study found that stocks offering the highest level of dividend payouts have not performed as well as those that pay high, but not the very highest, levels of dividends.”

Read more about this research here.

As a dividend aristocrat, we can’t really expect WMT to pay a very high dividend yield. At 2.44%, we can’t really talk about a high dividend yielding stock. In fact, it would fall outside of many dividend investors’ filter research. It would have not been part of my own investing criterion a few years ago, but I’ve given more importance to another metric since then…

Principle #2: If There is One Metric; It’s Called Dividend Growth

If I had to go blindfolded to pick a stock and have only one metric to look at, I would pick dividend growth. This is the most important metric to me as it is a clear sign of the company’s financial health and its ability to pay me for years to come. Here’s an interesting quote from Saturna Capital:

“Indeed, dividend growth has been a much larger determinant of equity returns in this new era of low benchmark rates and higher levels of uncertainty.”

You can get the full detail here.

I previously wrote that the company quadrupled its dividend over the past 10 years. This means you can expect to see your dividend doubled about every five years.

The management team has clearly made a statement over the years that dividend growth is a priority. This helps any investors to be patient during tougher stretches. Since we don’t expect robust growth in sales or earnings in the upcoming year, it will be important to see how dividends will increase compared to its payout ratio.

Principle #3: A Dividend Payment Today is Good, A Dividend Guaranteed For the Next 10 Years is Better

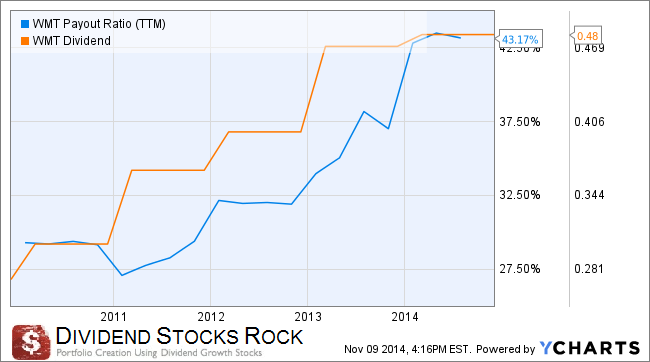

I think it’s very important to cross the payout ratio with the dividends paid over at least 5 years to see where the company is going with its dividend policy. It’s a key indicator to know if the payout will continue to increase or if it will reach a plateau at one point in time.

WMT’s dividend increases and the payout ratio followed similar trends. While 43% is far from raising a red flag on Wal-Mart, the fact we went from 27.50 to this level in three years tells you earnings are not growing fast enough. We can expect WMT to continue raising its dividend in the future but if the company keeps it on the same trend, I will be worried 3-4 years down the road.

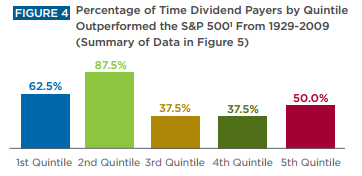

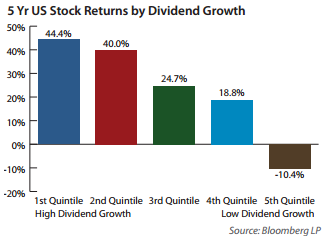

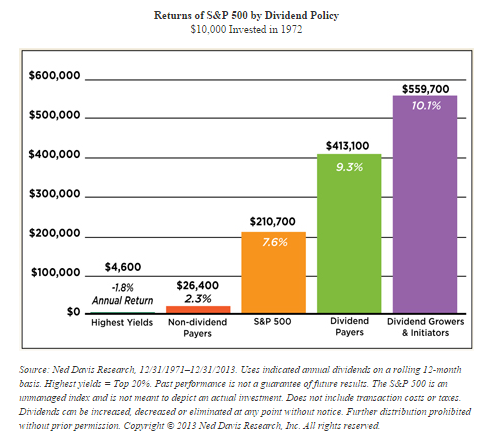

Principle #4: The Foundation of Dividend Growth Stocks Lies in its Business Model

A company that doesn’t have a sound business model won’t be able to sustain consecutive dividend increases over the long haul. On the other hand, businesses which pay dividends and increase them will outperform other stocks:

Source: Edward D. Jones – Dividend Stocks Rock

Now how can you find these marvels? This is why you need other financial metrics to identify companies that will be able to sustain and increase their dividend for the next 10 years. At DSR, we look at the 3 and 5 year metrics for Sales and Earnings per Share (EPS) growth. We only select companies showing positive growth over both the 3 and 5 year periods. Since an economic cycle lasts between 5 and 8 years, a strong company should be able to post increasing sales and earnings over these periods. I’m using both EPS and Revenue data from Ycharts:

DSR STOCK METRICS

3 year revenues = 4.13% Pass

5 year revenues = 3.33% Pass

3 year EPS growth = 2.97% Pass

5 year EPS growth = 7.56% Pass

Wal-Mart Company passed the four tests easily. However, we noticed the 3 year EPS growth is smaller than the 5 year. We might even see negative numbers in 2015. Therefore, WMT may not pass our tests a year from now. On the other hand, WMT is the leader of the retail business and benefits from a highly stable business model generating important cash flow. Considering its history, I think it’s worth it to be patient with such a company. This is why WMT is still part of my core dividend portfolio.

A Look at the Most Recent Results

Wal-Mart reported third quarter consolidated net sales of $118.1 billion, which is up 2.8% over last year’s Q3 revenues of $114.9 billion. Beating analysts estimates.

EPS is up by $0.01 compared to last year’s Q3 at $1.15 per diluted share. The company’s earnings beat analysts’ estimates of $1.12 per share, while revenue fell short of the $118.37 billion expectation.

For the end of 2014, WMT has narrowed its guidance to a range of $4.92-$5.02 from its previous range of $4.90-$5.15. Analysts are expecting FY2014 EPS of $4.99.

21% increase in e-commerce sales, this is a perfect timing before the big season.

This is not the most amazing growth ever, but still growth is growth, especially when your name is Wal-Mart! I will definitely keep WMT in my portfolio.

Disclaimer: I personally hold WMT shares at the moment of writing this article. Also, WMT is held in some Dividend Stocks Rock Portfolios.