As you might have read about it here, I do live webinars and certainly have fun doing so. I have been surprised by the positive interest attendees had towards many of my stock picks. This is how I came to the idea of sharing here some of my “Video of the Week”, during wich I go through a company recent news or results and explain why I believe it is currently a good or a bad pick for a dividend investor.

Investors looking for a safe consumer defensive stock during tougher market times will be served with Pepsi (PEP), part of the consumer defensive sector. Having 90% of its brands as #1 or #2 in their sector, this Dividend Aristocrat is there to stay. Its recent healthier products are also interesting moves for the future!

Video

If you enjoy the videos format and want more of them, subscribe to my YouTube channel!

Verbatim

00:02 Mike Heroux: Hello fellow investors, this is Mike Heroux from Dividend Stocks Rocks. I hope you’re doing well today. For the stock pick of the week, we are going back on Canadian territories. Once again, I wanna discuss a leader in its market a company that is paying a 5% dividend yield with lots of growth going on over there, but for some reasons, it has been ignored by the stock market and now the stock is down double digits since the beginning of the year. So let’s talk about BCE also known as Bell. Ticker is BCE as well, both trading on the Canadian and on the US market. So even my fellow American investors can pick some shares of BCE which I think it’s probably a better investment than the AT&T or Verizon.

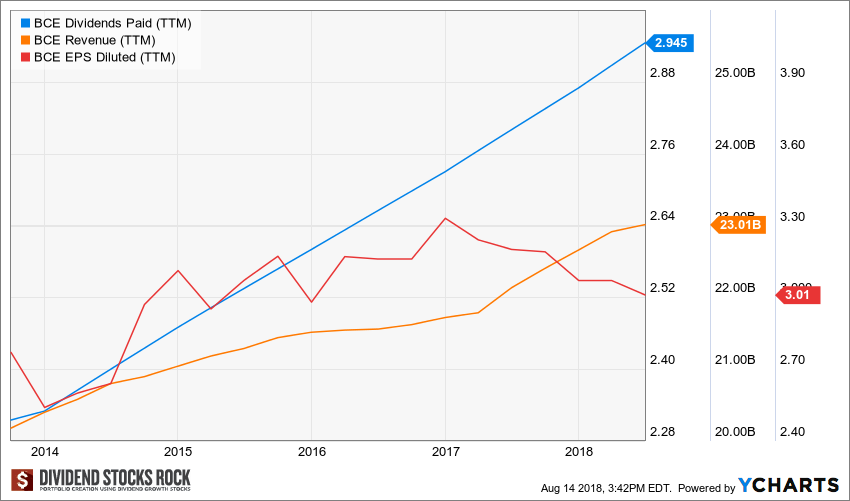

00:54 MH: What is important to understand is about 40% of BCE’s revenue are coming from its wireline business. This includes the phone wireline that is probably dying, cable that is not doing so well, but it also includes its internet services. And as a client of Bell, I can tell you that their internet is very fast and reliable. I think there is a good growth potential over there. And also to mention that client cutting down the cable is a phenomenon, but it’s not that common in Canada. So I think that Bell will be able to benefit from this cash cow for several years, also because 10% of its revenue is coming from BCE media.

01:42 MH: So they’re producing their own content, they have their own channels, they’re involved in sports, so in MLS in hockey with The Toronto Maple Leafs. So they have an interesting growth vector over there as well, so they’ll be able to produce original content and not lose all their cable clients at the same time. But the real growth vector is obviously wireless. That is the other 40% of revenue for Bell. So this is the largest telecom company in Canada. It’s important to understand that wireless industry is dominated by three players in this country. So we’re talking about Bell, TELUS, and Rogers. So together, all three, they control about 90% of the wireless market. So in other words, they are working in oligopoly, they pretty much put their service and their fees at whatever they want.

02:42 MH: It’s a subscription-based model, so each month the money’s coming in, so highly recurring which is very great for a company that’s paying a 5% dividend yield right now. So it’s quite an opportunity for income-seeking investor because you have the opportunity to invest in a company that is quite stable, evolving in a protected area with the wireless, and that is known across Canada. So I think that Bell will continue to increase its dividend, probably around 3% to 4% each year, but that’s enough to keep up with inflation and still earn a good living from this stock. What’s wrong with BCE? I guess the major concern is around its debt level. The company bought Manitoba Telecom a few years ago, MTS, so now they are well involved and well present in this province, but this help to crank up the debt a little bit higher. So obviously, as interest rates are rising, it will be a little more difficult for Bell to do other deals like that as profitable and they will still also have to reimburse that debt.

03:53 MH: I don’t think it’s justified. I don’t think that the value is justified right now. I think that there’s a good potential that BCE, it’s higher than 60 bucks shortly. So if you want a chance to pick a 5% yield, I think here it is. Once again, this cannot be taken as a buy or sell recommendation, it cannot be taken as a financial advice. I am not your broker or your personal advisor, therefore you cannot sue me after watching this video, if you’re ever losing money on BCE. But on the good side of things, you just have to give me a thumbs up if you’re making some. Don’t forget to subscribe to my YouTube channel and if you want more videos like this and more information about the stock market, head over to my blog, thedividendguyblog.com, and sign up for my newsletter over there. So hope that you have enjoyed this video, and we’ll see you next week.

Image source: pixabay

The post Video of the Week: BCE – The Phone is Ringing, Will You Pick It Up? appeared first on The Dividend Guy Blog.