Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas.

Today, we’ll discuss two of the Canadian ideas among the list: Tecsys (TCS.YO) and Atco (ACO.X.TO).

Growth Perspective: Tecsys (TCS.TO)

Business Model

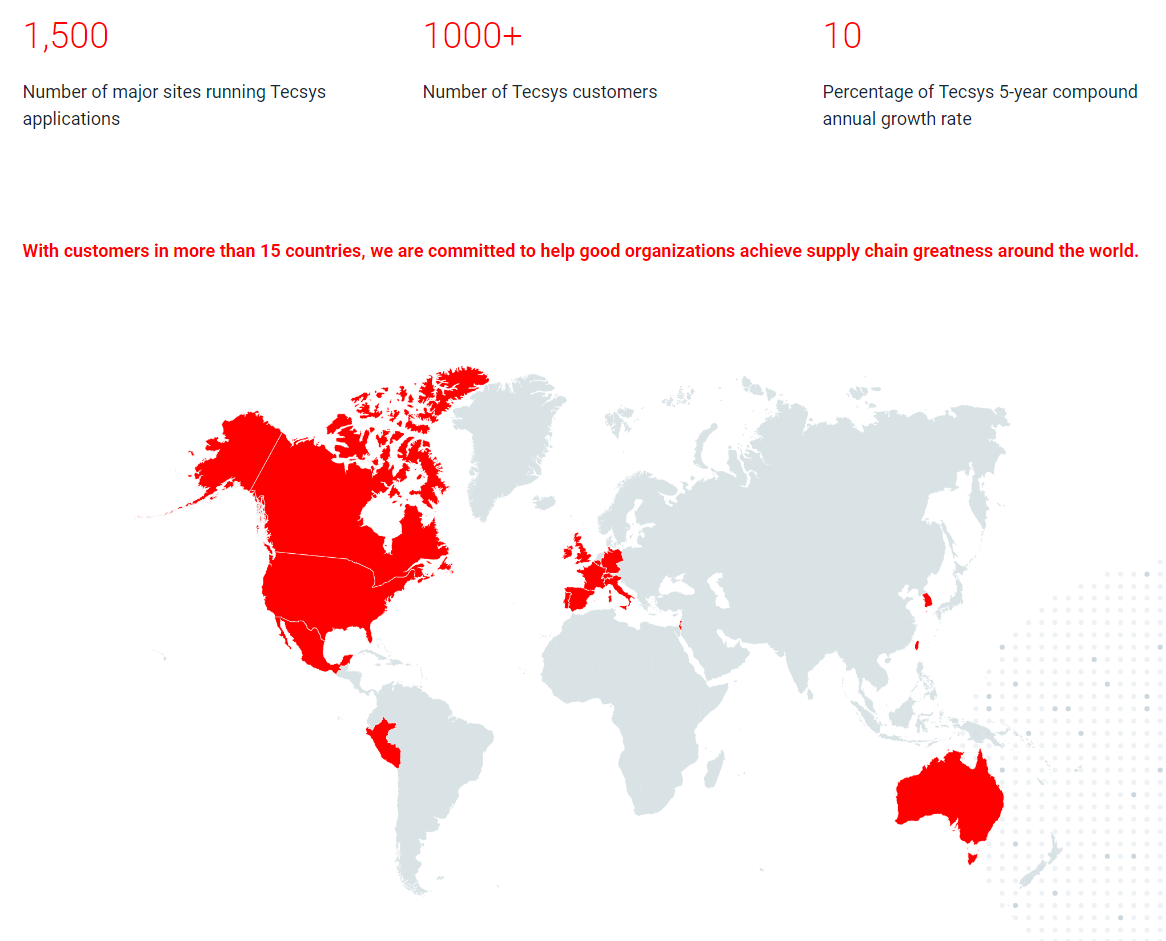

Tecsys is engaged in the development and sale of enterprise supply chain management software for distribution, warehousing, transportation logistics, point-of-use and order management systems. It also provides related consulting, education, and support services. TCS serves healthcare systems, services parts, third-party logistics, retail and general wholesale distribution industries. Geographically, it derives most of their revenue from the United States and has a presence in Canada and other countries. Its only operating segment is the development and marketing of enterprise-wide distribution software and related services.

What’s the Story

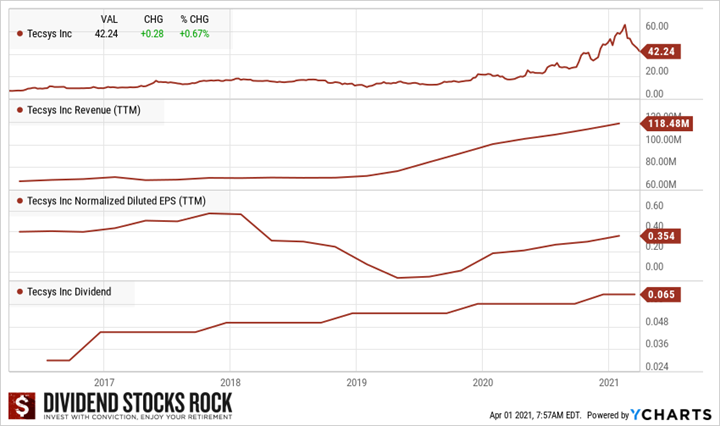

I personally bought shares of Tecsys in December of 2020. The stock surged as high as $65 and went down to the low $40’s. Its quarterly results disappointed the market that may have set the bar too high. TCS continues to focus on recurring revenues and reported a robust quarter. SaaS revenue increased by 89% to $4.7M in Q3 2021. Cloud, maintenance, and subscription revenues increased 26% to $13.4M. The performance was primarily driven by SaaS. Annual Recurring Revenue as of January 31, 2021 was up 20%. This shows strong and steady growth across the business

Investment Thesis

This small-cap (700M$ in market cap) shows much capital gain potential. TCS offers crucial software for any e-commerce business: a supply chain management software! Considering delivery fees and fierce competition in the retail world, optimizing your supply chain is a key element for any business shipping goods. Tecsys also helps large customers with complex distribution centers or in the healthcare business. With only 13% of the healthcare market share, there would appear to be much potential for growth. With over 1,000 customers and about half of their revenue coming from recurring contracts, TCS is creating a strong base for its future growth.

I also covered Tecsys and two other SaaS stocks that I like in the video below.

Potential Risks

The growth potential is obvious and the TCS shareholders enjoy the hype. However, you should always proceed with caution with a small cap that sees its price skyrocket. When you look at the company’s PE ratio, you must hope Tecsys will grow their earnings rather quickly. Fluctuation is part of the deal when you invest in such a company. Expect more stock price volatility with this company. We like that TCS doesn’t have much long-term debt ($10M), but it won’t matter if the company must fight against giants in the tech industry. Being a small fish in the ocean of technology could be dangerous.

Retirement Perspective: Atco (ACO.X.TO)

Business Model

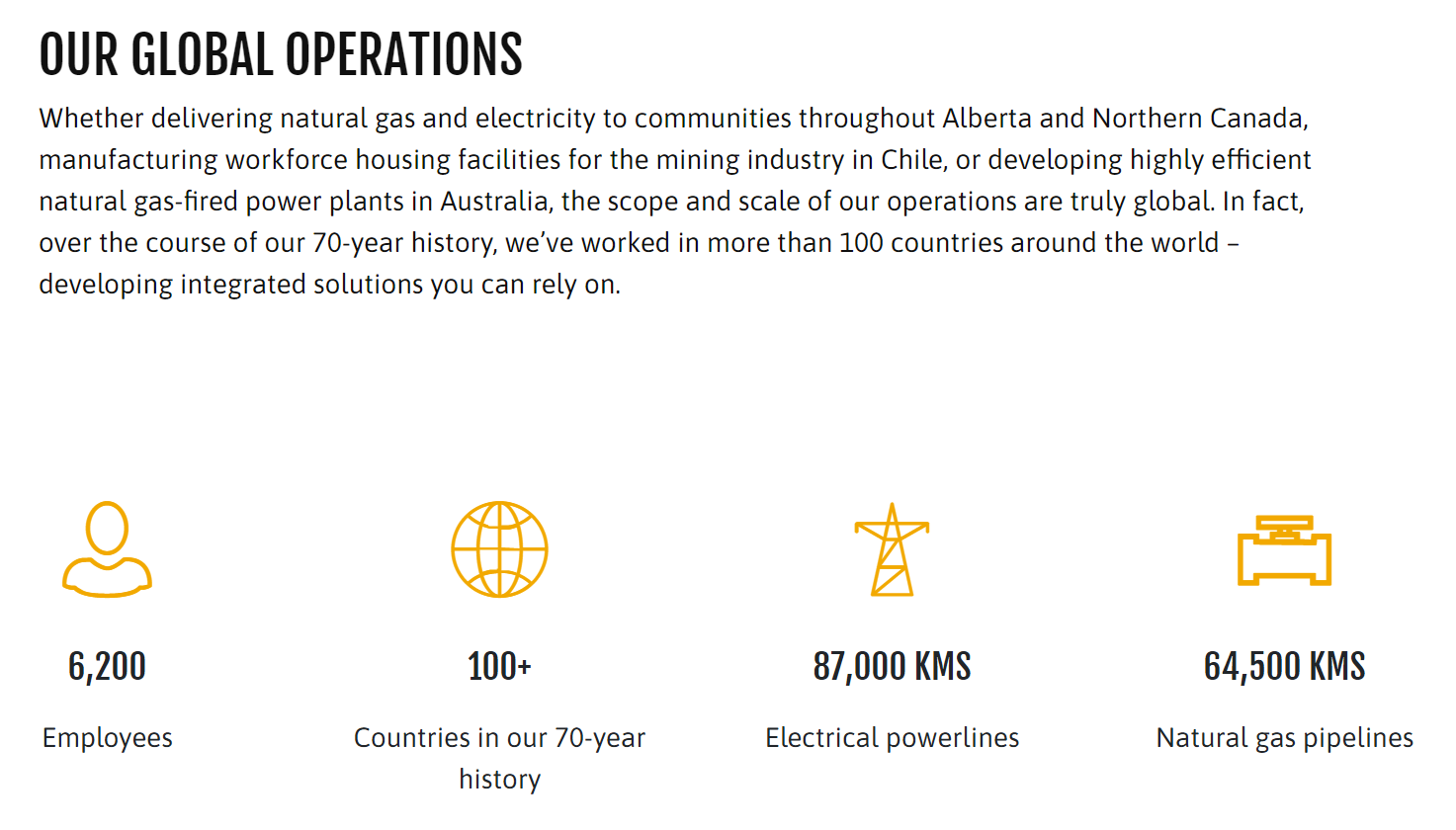

Atco Ltd is a Canadian holding company that offers gas, electric, and infrastructure solutions. The largest subsidiary of the company is Canadian utilities, which operates natural gas, electricity, and logistical services. Atco’s primary segments include electricity (generation, transmission, and distribution), pipelines and liquid, Neltume Ports and Structures and logistics. The firm mainly operates in Canada and Australia, along with some operations in the U.S, the U.K., and Mexico.

What’s the Story

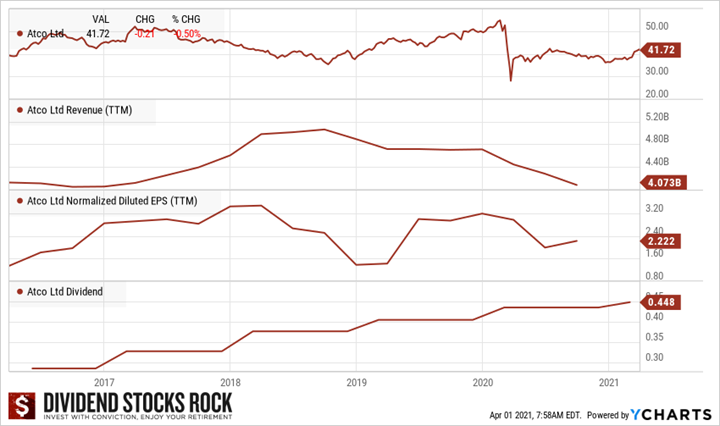

It seems that our overall play on utilities is paying off. Atco, along with ED, XEL and EMA.TO, performed well in March showing double-digit returns. It’s simply the market realizing that, once again, it has overreacted to interest rate increases. There was no notable news about Atco during March.

On February 25th, Atco released its quarterly earnings. The company did well with adjusted earnings up by 22%. Results were supported by stronger results in ATCO Frontec from additional customer work requests, in Neltume Ports from higher cargo volumes and margins, and in Canadian Utilities from cost efficiencies, growth in the asset base, and ongoing transition work related to the long-term contract to operate Puerto Rico’s electricity transmission and distribution system. During the quarter, Atco acquired the remaining 50% interest in the ATCO Sabinco S.A. joint venture partnership. With this strategic investment, ATCO Structures gained full ownership and control of its Chilean business.

Investment Thesis

Atco is known by Canadian dividend investors for its stellar dividend growth history. After selling its fossil fuel-based electricity business in 2019, Atco now concentrates on expanding its renewable energy business (Natural gas with 185MW, Hydro with 59MW and Solar with 3MW). The company has a CAPEX plan of $3.2B through 2023. Atco can count on a stable business model with 95% of its earnings coming from regulated utilities. It is also expanding outside of Alberta where its core business has been. They announced their participation (40%) in the acquisition of Neltume Ports in South America for $450M. We appreciate Atco’s plan to expand its business outside of Alberta. We think it’s a great move to diversify their business model. You can sleep well at night as your dividend is safe.

Potential Risks

Atco has been growing rapidly over the past decade through various projects and acquisitions. The problem is their debt has followed a similar trajectory. ACO now has over $9B in debt but keeps a credit rating of A- due to its stable business and ability to generate cash flow. The economic slowdown in Alberta will have an impact on the company’s growth for the coming years. As Atco is investing massively in many projects at the same time, it will be interesting to see how management remains in control. Also, the market seems to be concerned all the projects won’t be as profitable as expected. As Atco shoots in all directions with several business segments and new acquisitions, the risks of making mistakes increase.

Why Having a Buy List?

Having a buy list or a potential replacement list ready is great in order to take action. It is much easier to sell when you feel the excitement for a better holding.

Rating your holdings according to a simple, but efficient set of metrics will also solve your buy & sell dilemma. You will automatically identify the strong companies and weak companies in your portfolio. I’ve discussed my ranking system on my YouTube channel. Combined with a Buy List, this system can help you avoid paralysis by analysis.

The post Two Stocks on My Buy List: Tecsys (TCS.TO) and Atco (ACO.X.TO) appeared first on The Dividend Guy Blog.