Last year hasn’t been quite what we expected. And let’s admit it, while 2021 brings some hope, a number on a calendar is not magic.

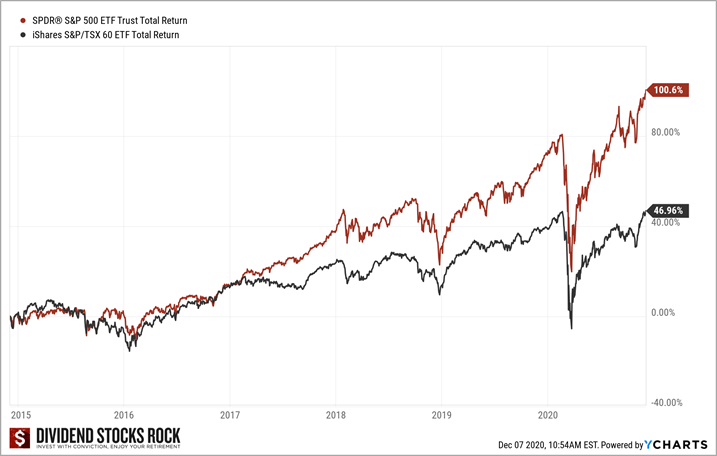

If there is one single piece of wisdom you must remember from 2020 it is this: stay invested. If you stayed invested over the past 6 years, you went through much consternation, but also much growth and success.

2015: The market was going nowhere and CNBC said that 2015 was the hardest year to make money in 78 years.

2016: Brexit was on the rise, and stocks took a hit. The Brexit vote led to stock market crashes around the world. The market losses amounted to a total of 3 trillion US dollars by 27 June 2016.

2017: The market was trading at an all-time high, then the dreaded Hindenburg Omen returned. If you don’t feel like reading, let’s just say that the Hindenburg Omen called for a market crash.

2018: The Hindenburg prophecy was real! The market dropped during the second part of 2018, but the worst was yet to come. CNBC called for 2018 to be the worst year for stocks in 10 years (they have a knack for clickbait titles!).

2019: Oops! The apocalypse did not happen during this year. In fact, 2019 was the best year of the past 10 years.

2020: The queen of uncertainties! However, if you look back at the past 6 years, nothing has changed dramatically. The apocalypse is always about to happen. Yet, if you stayed invested since December 2014 your portfolio is now clearly in better shape now with the US market having doubled in value and the Canadian market being up 50%.

Which Canadian Dividend Stocks Should be in your portfolio for 2021?

Today, I’m picking companies that will pay and increase their dividends and will likely provide you with a nice capital appreciation. The selection methodology of those companies is explained in this article:

What should a Dividend Growth Investor buy in 2021?

Here are some great stock ideas for 2021:

Franco Nevada (FNV.TO)

- Market cap: 32B

- Yield: 0.61%

- Revenue growth (5yr, annualized): 18.05%

- EPS growth rate ((5yr, annualized): 25.73%

- Dividend growth rate (5yr, annualized): 10.57%

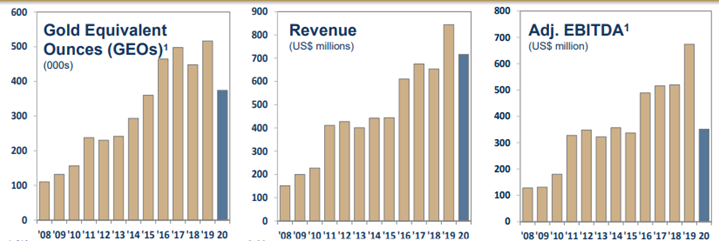

If you must buy a gold stock, we would go with Franco Nevada. Why? Because the company is somewhat sheltered against commodity price fluctuations and because it has no debt. Franco-Nevada doesn’t waste its time operating mines, but rather manages a portfolio of royalty streams. The company owns 45,300 square kilometers of geologically prospective land but will let “gold miners” spend their time and money on exploration. If the miners find something, the royalty will kick in. We like this “cash flow focused” business model. As FNV is a play on gold and precious metals, it enjoys stronger cash flows when gold prices surge. The company shows unparalleled portfolio diversification offering shareholders some peace of mind in volatile markets. It is a “Covid-19” proof business model.

When you look at how gold prices have fluctuated since 2008, you can appreciate FNV’s revenue relatively stable growth. The company is also showing 13 years of consecutive dividend increases which is quite a milestone in this industry! Franco Nevada is pretty much a money printing machine that will do well if the FED and Bank of Canada continues to print their own money!

The company shows larger gold reserves than the average in its industry. Considering FNV has no long-term debt, it could also easily acquire more assets and make sure its gold reserves are even larger. This would lead to a long period of positive cash flow generation (and you can see the dividend increases coming your way!).

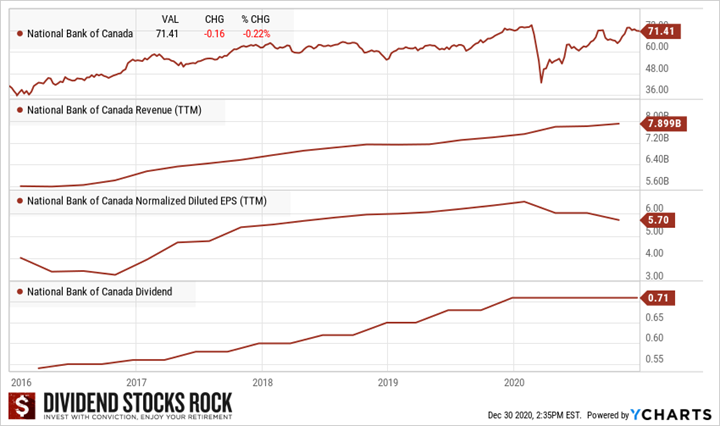

National Bank (NA.TO)

- Market cap: 24B

- Yield: 3.97%

- Revenue growth (5yr, annualized): 6.67%

- EPS growth rate ((5yr, annualized): 4.79%

- Dividend growth rate (5yr, annualized): 6.84%

If I had to rank Canadian banks, I would do it like this:

#1 National Bank: Smaller than the others and not considered by many. NA is swift and agile like a ninja. The company counts on a strong performance from capital markets and wealth management to grow their business. In the past few years, they have successfully expanded their business across the U.S. and a part of Asia (ABA bank in Cambodia).

National Bank enjoys a strong position in Quebec. It has been ignored by the 5 banks for a while leaving plenty of space for both Desjardins (credit union) and NA to expand their network. Today, NA is expanding its business through targeted acquisitions (Credigy a speciality credit firm in Atlanta, ABA bank in Cambodia).

NA has built an impressive wealth management division including National Bank Financial, National Bank Brokerage and Private Banking 1859. It has sold its mutual fund segment to Fiera a few years ago to concentrate on financial advice to its clients. This was a smart move as they couldn’t always compete with larger asset managers. At the same time, they are now able to pick any type investment product from any asset manager to build their clients’ portfolios.

Going forward, I think NA will continue to perform well (probably better than the other Canadian banks) and therefore, it remains my number one pick in this industry. The other banks are ranked as follows:

#2 Royal Bank: It’s a giant with ties to all business segments. I like their exposure to wealth management, capital markets and insurance. Even better, they post consistent results all the time.

#3 TD Bank: I love their classic but successful approach to banking. They have a strong exposure to the U.S. and understand how to combine their branches with wealth management services. A top performer.

#4 BMO: I like their guts (1st to offer ETFs in Canada, and the Harris bank acquisition) and their focus on wealth management and capital markets. However, their weak dividend growth (compared to its peers) and inconsistent results take them out of the top 3.

#5 Scotiabank: Their international narrative hasn’t generated results in the past 10 years. It’s still a good bank, but others are just better.

#6 CIBC: A classic savings and loan bank that doesn’t do anything better than TD. They do offer a great yield though.

You can watch my end of year Canadian banks review here.

Find out about 6 companies that will crush 2021

Each year, I compile a list of 20+ stocks that are expected to do better than the market. Back in December of 2019 we just finished an amazing year with double-digit returns. Then, the pandemic crushed the market (down 30%) and the flood of new money combined with strong growth from tech, consumer staples and gold brought the market back up by double-digits. Staying invested has been the key factor to the many who had success with their portfolio in 2020.

You can download 6 of my top 20 for 2021 right here:

Disclaimer: I hold shares of National Bank.

The post Top Canadian Dividend Stocks for 2021 appeared first on The Dividend Guy Blog.