Yesterday, I’ve made my list of my favorite 5%+ yielder on the U.S. market. Finding solid companies paying high yields is a very difficult task. Many investors think they can simply pull out a filter including a 5 year history and some more metrics and they can build their portfolio by picking any stocks in this basket. This sounds a lot like the perfect recipe to suffer from dividend cuts in a few years from now!

Since I started Dividend Stocks Rock 5 years ago, I haven’t suffered a single dividend cut. This is mostly because I follow a strict investment process and follow each company quarterly. The following are examples of companies that meet my retirement rules.

Inter Pipeline (IPL.TO)

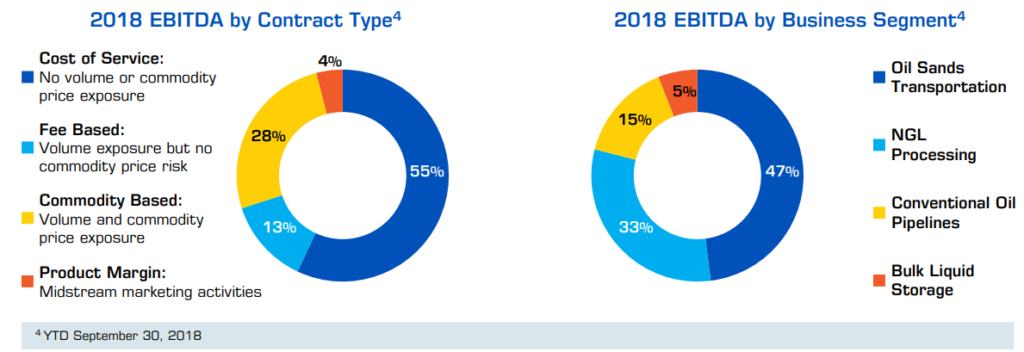

Inter Pipeline Ltd. is an energy infrastructure business engaged in the transportation, processing, and storage of energy products across western Canada and Europe. IPL is among the rare companies making our list of the top dividend energy stocks. The company operates four distinct business segments: Oil Sands Transportation, consisting of three pipeline systems; NGL Processing, including both natural gas and off-gas processing facilities; Conventional Oil Pipelines, consisting of 3,900 km of pipeline across three systems; and Bulk Liquid Storage.

Source: IPL Q3 2018 fact sheet

IPL stock has been down most of 2018. This is the case with many pipeline companies. However, you can see that it’s a “sector thing” as IPL just closed a record year with double-digit FFO increase for the year. Management increased its dividend significantly and still shows an FFO payout ratio well under control.

Polaris Infrastructure (PIF.TO)

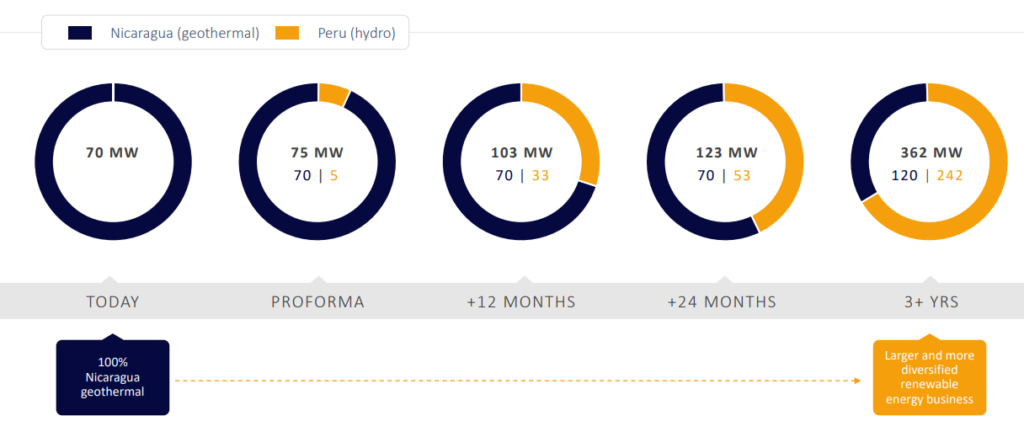

Polaris Infrastructure Inc is a renewable energy company. It is engaged in the operation, acquisition, and development of renewable energy projects in Latin America. In fact, Polaris owns and operates San Jacinto Geothermal power plant in Nicaragua. PIF has a contractual price per MWh (Power Purchase Agreement or PPA) with the government including annual escalator through 2029. Management recently announced the acquisition of Union Energy Group Corp. This transaction will open the door for many hydro electric projects in Peru and will help PIF to diversify its business model.

Source: PIF October presentation

The investment thesis around Polaris Infrastructure is a risky play that could pay off a lot. While management has proven its ability to increase its revenue and cash flow consistently since 2014, the stock plunged severely in 2018. This all happened because of the violence in Nicaragua. PIF shows a solid contract and great execution providing increasing cash flow and allowing management to pay off debts. Geothermal energy is part of the future for many countries, and it is a reliable & green source of power. Unfortunately, political instability gathers all the attention. If you are willing to take the bet, PIF could definitely make you richer. While there is a problem with the current president, Nicaragua shows the strongest GDP growth in Central America. Now that the company has found another growth vector in Peru. We think PIF will be a solid investment in the Utility sector.

Enbridge (ENB.TO)

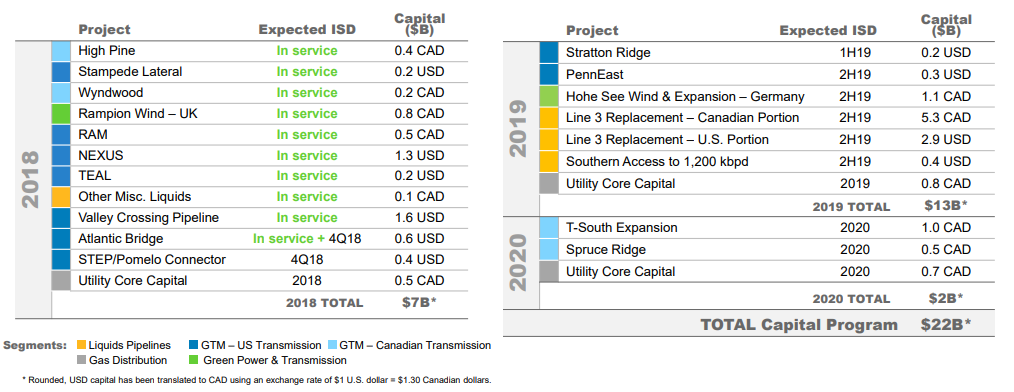

Enbridge owns and operate an impressive network of liquid (OIL) and natural gas pipelines. ENB is able to transport energy from coast to coast, from north to south. ENB shows about 96% of its business done through “take-or-pay” contracts. The pipeline is like a toll on a highway; people pay for each use and the company piles-up the cash.

Source: ENB Q3 2018 presentation

Companies do not pay a high yield for no reason. ENB raised its debts and number of shares with the merger of Spectra. As pipelines require lots of capital to build and maintain, Enbridge may find itself in a position where cash is missing. After all, management has plenty of projects to fund, a double-digit dividend growth promise to keep and larger debts to repay. There is always a possibility where this scenario turns bad.

Enbridge clients enter into 20-25-year transportation contracts. The company is already well positioned to benefit from the Canadian oil sands (as its Mainline covers 70% of Canada’s pipeline network). Now that is has merged with Spectra, about a third of its business model will come from natural gas transportation. The company has a handful of projects on the table or in development. Among those projects is the Line 3 replacement. The company expects the completion of this project in mid-2019.

Emera (EMA.TO)

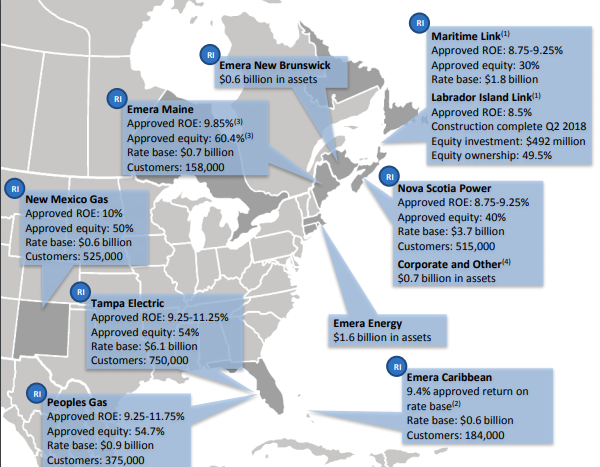

Emera is an energy and service company. Emera’s main market is Nova Scotia as it owns Nova Scotia Power, the province’s main electricity provider. Emera owns power plants and distributes natural gas in Canada, the USA and the Caribbean. This utility employs over 7,000 workers and serves more than 2.5 million customers. Tampa Electric (41%), NSPI (14%) and Maritime Link (11%) generate most of EMA’s earnings.

Source: EMA Q3 2018 investors presentation

Emera has been increasing its dividend payment each year for over a decade now. With the purchase of TECO energy, management intends to continue its tradition. The company forecasts a 4-5% dividend growth rate throughout 2020 while targeting a payout ratio of 70-75% (Emera Investors Presentation). At 5%+ dividend yield, this is a keeper for several years.

Emera is a very interesting utility with a solid core business established on both sides of the border. EMA now shows $28 billion in assets and will generate revenues of about $6.3 billion. It is well established in Nova Scotia, Florida and four Caribbean countries. This utility counts on several “green projects” with hydroelectricity and solar plants. This decreases the risk of future regulations affecting its business as the world is slowly moving toward greener energy.

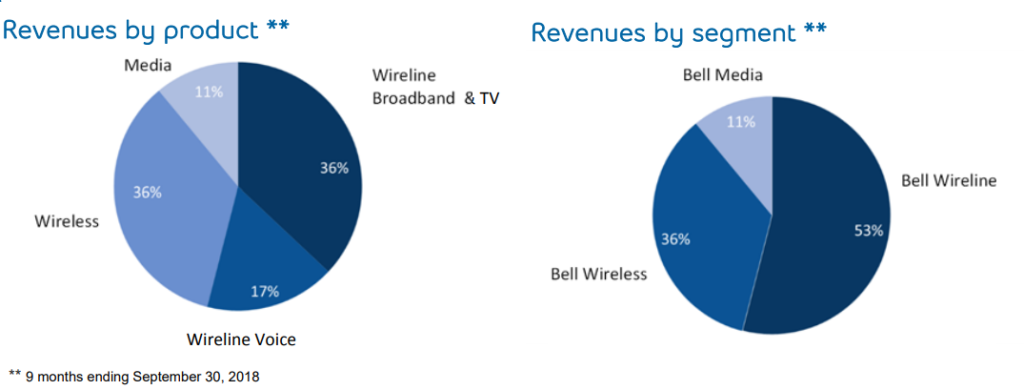

BCE (BCE.TO)

BCE is the largest Canadian telecom by market cap, about twice the size of Telus. It shows the most balanced business model among this small group. BCE has shown a very solid dividend profile for several years and my analysis proves it will continue to rise in the future. All BCE services are based on some sort of monthly subscription generating a consistent base for cash flow.

Source: BCE investors fact sheet

BCE debt level is not be underestimated. BCE is a giant… with a giants debt. This is not a perfect situation as interest rates are now rising. And, as the Canadian Government keeps pushing for more competition in the wireless industry, BCE may see additional competitors adding more pressure on margins in the future.

When you have the opportunity to invest in a strong yielder like BCE, and still hope for a small stock appreciation growth, you must take a hold of it. BCE shows a well-diversified business model and will continue to generate strong cash flow in the future. The company is a real money printing machine. As BCE is part of an oligopoly (Telus, Rogers and BCE controls about 90% of wireless market), there is limited competition and high barriers to entry. Since BCE offers a wide array of products, it can increase revenue generated by each customer.

Final Thought

Most of those companies have been selected in our 100% Canadian retirement portfolio. You can learn more about how we created safe portfolios generating 4-5% yield each year (and growing their dividend!). I’ve recently hosted a free webinar on this topic and you can now watch the free replay here:

Click here to watch the webinar replay

(must enter your email to register).

Disclaimer: We hold IPL, PIF, ENB, EMA and BCE in our portfolios.

Featured Image Source: Pixabay

The post Top 5%+ Juicy Canadian Dividend Stocks appeared first on The Dividend Guy Blog.