What Makes High Liner Foods (HLF) a Good Business?

HLF is the leading North American processor and marketer of value-added frozen seafood. The company has been in operation for the past 115 years and offers over 30 species through its line of products. The company sells its products through all major supermarket chains across Canada and the USA.

Ratios

Price to Earnings: 13.58

Price to Free Cash Flow: 5.46

Price to Book: 1.991

Return on Equity: 15.48%

Revenue

Revenue Graph from Ycharts

How HLF fares vs My 7 Principles of Investing

We all have our methods for analyzing a company. Over the years of trading, I’ve been through several stock research methodologies from various sources. This is how I came up with my 7 investing principles of dividend investing. Let’s take a closer look at them.

Source: Ycharts

Principle #1: High Dividend Yield Doesn’t Equal High Returns

My first investment principle goes against many income seeking investors’ rule: I try to avoid most companies with a dividend yield over 5%. Very few investments like this will be made in my case (you can read my case against high dividend yield here). The reason is simple; when a company pays a high dividend, it’s because the market thinks it’s a risky investment… or that the company has nothing else but a constant cash flow to offer its investors. However, high yield hardly comes with dividend growth and this is what I am seeking most.

Source: data from Ycharts.

The company only recently appeared on my radar due to this major stock price decline (about -25% in the past 12 months). Now that the dividend yield is over 2%, it makes this company even more interesting. Consider the strong dividend growth trend since 2012, you will see your yield based on your cost of purchase will grow quickly. HLF.TO meets my 1st investing principle.

Principle#2: Focus on Dividend Growth

My second investing principle relates to dividend growth as being the most important metric of all. It prove management’s trust in the company’s future and is also a good sign of a sound business model. Over time, a dividend payment cannot be increased if the company is unable to increase its earnings. Steady earnings can’t be derived from anything else but increasing revenue. Who doesn’t want to a company that shows rising revenues and earnings?

Source: Ycharts

The company is obviously getting more generous with its shareholders recently. Since 2003, the dividend payment has increased by 28% CAGR. The bulk of this increase is shown on the graph above. HLF.TO meets my 2nd investing principle.

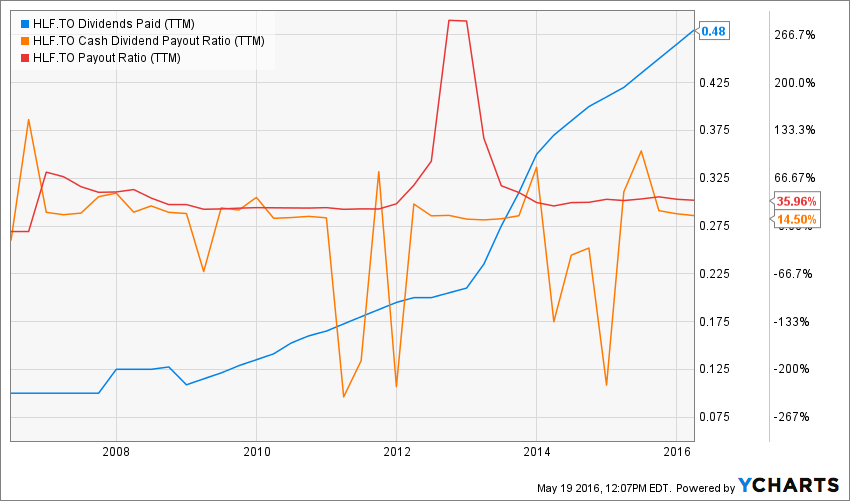

Principle #3: Find Sustainable Dividend Growth Stocks

Past dividend growth history is always interesting and tells you a lot about what has happened with a company. As investors, we are more concerned about the future than the past. this is why it is important to find companies that will be able to sustain their dividend growth.

Source: data from Ycharts.

While management has become more generous, it didn’t put the company in a precarious situation. In fact, there is plenty of room for more dividend increases in the future. As you can see, the payout ratio is well under control at 35.96% and the cash payout ratio is even lower at 14.50%. HLF.TO meets my 3rd investing principle.

Principle #4: The Business Model Ensures Future Growth

The company’s business model relies on its strong partnerships with supermarkets. Due to its size and brand recognition, HLF.TO benefits from great placement in each food store. The company has always focused on improving its products and this works well to improve the variety of fish in families’ menus.

There is an obvious trend to reduce red meat in everybody’s diet and the seafood market should be among the best food sectors to benefit from this. As cooking has become a hobby for many households, we are moving far from the classic fried trout in a pan with butter.

What High Liner Foods does with its cash?

While the company grew its dividend significantly over the past few years, it also focuses on increasing its cash flow generation for several other reasons. Management is using its cash flow to make acquisitions and then, to pay off their debts. Since the seafood category remains highly fragmented there is a lot of room for growth by acquisition.

High Liner Foods shows a strong business model and meet my 4th investing principle.

Principle #5: Buy When You Have Money in Hand – At The Right Valuation

I think the perfect time to buy stocks is when you have money. Sleeping money is always a bad investment. However, it doesn’t mean that you should buy everything you see because you have some savings put aside. There is some evaluation work to be done. In order to achieve this task, I will start by looking at how the stock market valued the stock over the past 10 years by looking at its PE ratio:

Source: data from Ycharts.

Besides an important drop in earnings between 2012 and 2014, the company has always been traded at a relatively low PE ratio. Over the past 2 years, the company has never been trading at such a low PE. The main reason behind this is the fact that seefood price have increased, hurting consumers willingness to buy more.

On a more mathematical approach, I will use a double stage dividend discount model to show how HLF’s dividend payout should be valued. Since I’ll be using an aggressive dividend growth rate (10% for the next 10 years and 9% for the years after), I will also require a high investment return (discount rate at 12%):

| Input Descriptions for 15-Cell Matrix | INPUTS |

| Enter Recent Annual Dividend Payment: | $0.52 |

| Enter Expected Dividend Growth Rate Years 1-10: | 10.00% |

| Enter Expected Terminal Dividend Growth Rate: | 9.00% |

| Enter Discount Rate: | 12.00% |

Considering their very low payout ratio and long term business perspectives, I think the company can afford such aggressive numbers. Here are the results of my calculations:

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 11.00% | 12.00% | 13.00% |

| 20% Premium | $37.00 | $24.59 | $18.39 |

| 10% Premium | $33.92 | $22.54 | $16.86 |

| Intrinsic Value | $30.84 | $20.49 | $15.33 |

| 10% Discount | $27.75 | $18.44 | $13.79 |

| 20% Discount | $24.67 | $16.40 | $12.26 |

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

As you can see, we are close to a 20% discount on the current price. HLF. TO meets my 5th investing principle.

Principle #6: The Rationale Used to Buy is Also Used to Sell

I’ve found one of the biggest investors struggles is to know when to buy and when to sell his holdings. I use a very simple, but very effective rule to overcome my emotions when it is the time to pull the trigger. My investment decisions are motivated by the fact that the company confirms or not my investment thesis. Once the reasons (my investment thesis) why I purchase shares of a company are no longer valid, I sell and never look back.

Investment thesis

First off, let’s say the healthy trend is playing in HLF’s favor. The population realizes eating more fish is better for their health than a good old steak. Plus, 45+ counts for half of the fish & seafood consumption and we know we are facing an aging population. This means more clients for HLF! The company makes 71% of its revenue in the USA & Mexico, growing markets . The company is showing strong dividend metrics and great room for additional dividend increases in the future.

Risks

Oddly enough, the company reported a decrease in sales and earnings over 2015. While logic tells us the market is increasing, HLF failed to prove it this year. The main problem is related to the price of seafood increasing significantly. This is why consumers are reluctant to put healthier food on their plate as it costs too much. Then again, HLF will have to face the battle of converting North Americans eating habits regardless of the cost. Quite a challenge!

As well, the USD drastically increased their cost of operations once converted into CAD. The company’s stock plummeted by 30%. While the overall numbers over 5 years are great, we will have to watch their financial results in 2016 carefully.

I believe the proportion of seafood place on our plates will keep increasing. Since this is a highly fragmented market, as such there is plenty of room for High Liner Foods to grow both internally and externally. This is why HLF.TO has a strong investment thesis.

Principle #7: Think Core, Think Growth

My investing strategy is divided into two segments: the core portfolio built with strong & stable stocks meeting all our requirements. The second part is called the “dividend growth stock addition” where I may ignore one of the metrics mentioned in principles #1 to #5 for a greater upside potential (e.g. riskier pick as well).

Having both segment helps me to categorize my investments into a “conservative” or “core” section or into a “growth” section. I then know exactly what to expect from it; a steady dividend payment or higher fluctuation with a great growth potential.

At this stage, I think HLF.TO could fit in both core and growth portfolio. The company is selling a consumable product and shows steady sales and increasing dividend payments. This is why it could be a core company. At the same time, there is a higher risk degree due to the fact consumers have a hard time paying higher prices for seafood. Because of this risk, the company is greatly undervalued right now. This is why this company could fit in both core and growth sides of my portfolio.

Final Thoughts on HLF.TO– Buy, Hold or Sell?

Overall, I think High Liner Foods shows great potential and since the stock price has taken a hit already, it may be the right time to fill up your plate with this company!

Disclaimer: I do not hold HLF.TO in my DividendStocksRock portfolios.

Disclaimer: The opinions and the strategies of the author are not intended to ever be a recommendation to buy or sell a security. The strategy the author uses has worked for him and it is for you to decide if it could benefit your financial future. Please remember to do your own research and know your risk tolerance.