Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas.

Yesterday, I covered two stocks that could boost your return. Today, I’ll share with you two picks offering an interesting yield for income investors.

While I’ve always been skeptical about AT&T (T) for years, it could finally see its debt level getting under control and becomre more interesting. Algonquin Power & Utilities (AQN.TO) has been hit by the pandemic. However, everything seems to be aligned for them to bounce back.

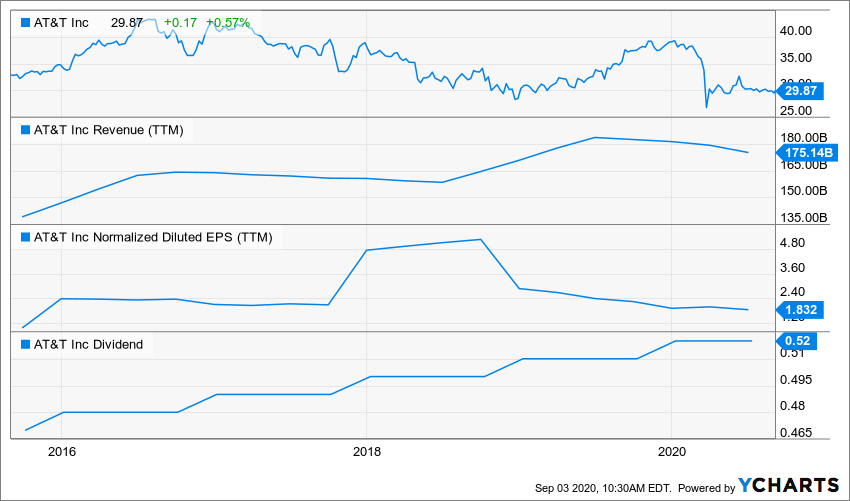

AT&T (T)

What’s the story?

The AT&T stock price is not moving much these days. While the company’s balance sheet is improving, AT&T must also face the consequences of some bad decisions. Back in 2015, T paid a steep price for DirecTV ($49B). There are now chatters that the telecom may be looking to sell this low performance business segment.

While there is no deal on the table, some talk about a potential sale around $20B is evident on the street. I’ve criticized AT&T for several years and mentioned repeatedly that the company had too much on its plate to be successful everywhere. Between the integration of Time Warner, the (failed) transformation of DirecTV, the 5G development and its generous dividend policy, AT&T finds its cash flow getting squeezed. While selling DirecTV at this price isn’t a good deal, this would put an end to this nightmare and would lighten AT&T’s total debt on the balance sheet.

Business Model

Wireless communication remains AT&T’s largest business, contributing nearly 40% of revenue. As the second- largest U.S. wireless carrier, AT&T connects more than 100M devices, including 63M postpaid and 16M prepaid phone customers. The consumer and entertainment segment (about 25% of revenue) includes the consumer fixed-line and DirecTV satellite television businesses, serving 20M television and 14M Internet access customers. WarnerMedia now contributes a bit less than 20% of revenue with media assets that include HBO, the Turner cable networks, and the Warner Brothers studios. Fixed-line business communications (14%), Latin American satellite television (2%), and Mexican wireless services (1%) constitute the remainder of the firm.

Investment Thesis

AT&T doesn’t need presentation. It is the largest telecom in the world by revenue. With over $180B in revenue, a ?6.5% yield, and 35 years with consecutive dividend increases, the big T is a favorite among income seekers. Really, what’s not to love? Unfortunately, we can say that the stock’s performance hasn’t impressed anyone in the past 5 years. Even by including its juicy payout, T’s investing return lags behind the market big time. The problem is that T requires lots of cash flow to shift its business (find growth vectors), expand to 5G and continues rewarding its shareholders.

Potential Risks

There are a few reasons why AT&T offers such a high yield (it doesn’t come for free!). First, the company must generate lots of cash flow to support new technologies (5G deployment), maintain dying technologies (wired lines), paying down its huge debts, and rewarding generously his shareholders. AT&T will also deal with customers which budget has been hurt by COVID-19. This is not a perfect solution, but the stock is priced accordingly.

Dividend Growth Perspective

At first glance, T’s dividend profile looks very good. High yield with consistent increases sounds perfect. However, looking at the dividend growth rate, things aren’t so well. Over the past decade, T’s annualized dividend growth rate is at 2.21%. Over the past 5 years, it goes down to 2.12%. This year again, the dividend increase was $0.01/share. You can expect a $0.01 increase per year going forward. Maybe it will get better once the debt gets under control.

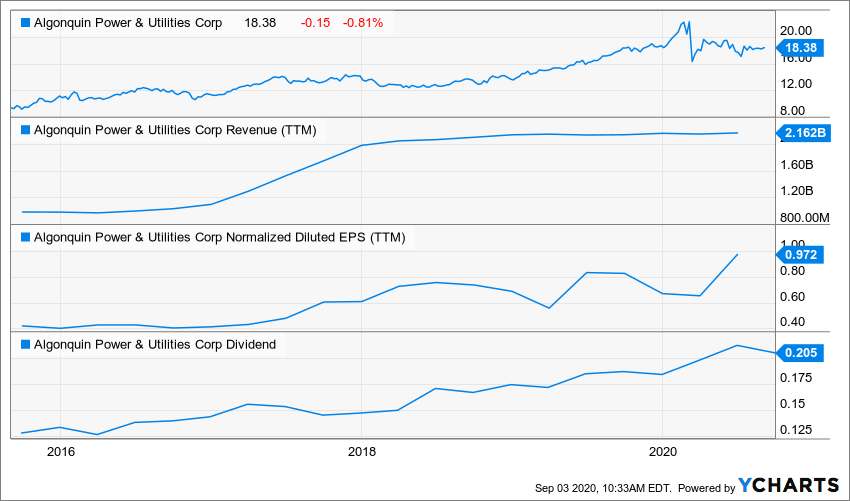

Algonquin Power & Utilities (AQN.TO)

What’s the story?

I’ve decided to add Algonquin to my buy list for its relatively high yield compared to Fortis (FTS). Canadian utility companies such as Emera (EMA.TO), Fortis (FTS) and Algonquin show a very interesting profile right now. Please note that AQN pays its dividend in USD.

AQN’s latest results were hurt by the pandemic. The COVID-19 pandemic and resulting business suspensions and shutdowns have changed consumption patterns of residential, commercial and industrial customers across all three modalities of utility services, including decreased consumption among certain commercial and industrial customers. The Company re-iterated its capital investment estimates for the 2020 fiscal year of between $1.3 billion and $1.75 billion. It also reaffirmed its EPS guidance for the full year (no changes). AQN achieved $5M in cost savings and expects to achieve further expense reductions of $10M in the last six months of 2020.

Business Model

Algonquin Power & Utilities Corp is a North American generation, transmission, and distribution utility. Within its distribution group, Algonquin owns and operates regulated water, natural gas, and electricity distribution utilities in the United States. Most of the company’s revenue is derived from this division and, in turn, most of this division’s revenue comes from its distribution of natural gas. In its generation group, Algonquin sells electricity produced by its energy facilities, including hydroelectric, wind, solar, and thermal power plants. Algonquin’s wind farms account for most of its generation revenue. Finally, the company’s transmission group focuses on building and investing in natural gas pipelines and electric transmission systems.

Investment Thesis

Like many utilities, solid growth is coming from outside the company. AQN had about 120,000 clients in 2013 and now serves 762,000 clients. It achieved this impressive growth through acquisitions, the largest one being Empire District Electric for $3.4B, completed in early 2017. With a budget of $9.2B in CAPEX, AQN has several projects through 2024. These include more acquisitions, pipeline replacements and organic CAPEX. The utility counts on its regulated business to grow its revenue once those projects are funded. AQN shows a double-digit earnings growth potential for the foreseeable future but expect a short-term slowdown due to the economic lockdown.

Potential Risks

Like most utility companies, AQN uses leverage to support its growth. It currently shows about 50% of its capital structure from long-term debt, and the rest comes from the equity market. The company has posted solid growth since 2012, but this may slow down after the next round of projects in 2024. If regulators are less generous than anticipated, revenue growth may fall short. AQN will see its revenue decrease by 10-15% in 2020 due to the coronavirus pandemic. Economic lockdowns will affect commercial and industrial demand for power. However, management still increased its dividend in May (+10%) and confirmed their CAPEX through 2024. Finally, AQN still runs pipelines and is not sheltered from spills.

Dividend Growth Perspective

The dividend fluctuation is due to currency as the company once paid its dividend in CAD, and now it is in USD. As a Canadian company, 93% of AQN EBITDA is in the U.S. Therefore, there is no reason to worry for the company’s cash distribution if the stock drops and the yield reaches close to 5%. With projects generating cash flow, AQN expects to raise its dividend by 10% CAGR and its EPS to grow at a faster rate. Shareholders can expect a single high-digit dividend growth rate for the next decade.

Final Thoughts

Keep in mind that having a strong investment strategy in which you identified what is a buy and what is a sell will greatly help you making the right decisions and avoiding paralysis by analysis.

No matter what stage of life you’re in and no matter what the economy goes through (e.g. a pandemic), there will always be buy opportunities when investing for the long haul.

If you need to refine your game plan for fall, you might want to watch this webinar replay.

Disclaimer: I do not hold T nor AQN.TO. I’m long FTS.

The post These Two Stocks Should Bounce Back and Offer Good Income for Your Retirement Portfolio appeared first on The Dividend Guy Blog.