A while ago, I wrote an article about the key metrics to find strong dividend growth stocks. This article opened a discussion with one of my readers, Ron, as he preferred higher dividend yield companies. He agreed to share with us the result of a very interesting calculation he made. He also wrote a quick article to explain what he found.

The Shocking Truth About Dividend Growth

Today, I was reading another dividend investing book and some statements by the author got me to thinking. What is the definition of investment “risk” and how should it enter into one’s thinking or decision making regarding dividend investing?

Many dividend investment consultants suggest or advise against relying too much on high current yields when selecting or constructing a dividend producing portfolio. I will not go into all the possible risks and reasons why a dividend may be “too high”, as I am certain you know them better than I do. You also know by now that I feel that settling on a low or average initial yield may be very costly for the investor, particularly if his investment time frame is less than 20 years.

Most of us have a difficult time trying to quantify yields versus dividend growth rates (DWRs) versus number of investment years and comparing what it means in real dollars, etc. so I thought I would make a chart comparing a couple of fictitious dividend investor portfolios and their stories.

Two investors have $10,000 to build their dividend investment portfolio, and both know enough to split the total investment equally between 10 different securities in this situation. Both plan to reinvest all of their dividends for 20 years.

Steady Eddy is a guy who has read all the investment advice and carefully picks his securities. His portfolio ends up with an initial yield of 3% and DGR of 8%. All of his stocks are blue-chippers.

Crazy Cal is a guy who does not have the patience to read everything on investing, but has some gut feels and has even visited Las Vegas. But he is not dumb either, and builds his portfolio with an initial yield of 5% and DGR of 8%. He figures he needs to beat inflation and after all these were not penny stocks but pretty good stocks with a pretty good track record at least recently.

Steady Eddy tells Crazy Cal that he is being too risky and doesn’t he realize what can happen. Crazy Cal doesn’t pay attention and takes a vacation in Vegas.

Well… unfortunately for Crazy Cal the stuff hits the fan for some of his securities and within 1 month of purchase 4 of the 10 securities have their dividends cut and within the next months all 4 of these securities go belly up… as in zilch, nada, worth zero!! What bad luck. Well this is exactly the type of thing Steady Eddy warned him against. His original $10,000, 10 stock portfolio is now a $6,000, 6 stock portfolio. Crazy Cal goes into hiding wondering how stupid can he be.

A few years go by and Steady Eddy and Crazy Cal meet up again and Steady Eddy can’t help but remember the dividend investing catastrophe of his buddy and ribs him about his own last year’s dividends. “What?”… Responds Crazy Cal…”My dividends were exactly the same!” Sure enough after getting out their respective records it was clear that Crazy Cal’s yearly dividends on his $6,000 portfolio was exactly the same as Steady Eddy.

The moral of this story is that although risk is something to be aware of in investing, it should also be analyzed to determine its true or actual cost. Trying to reduce all risk by being too conservative can reduce investment returns by surprising amounts. In this case, having catastrophic results for 40% of the picks still works out better than being conservative. I do not think most people would anticipate this outcome with the above example.

-Ron-

Further Thoughts on Ron’s Article

I was quite surprised to see the outcome of Ron’s little story. But when I started thinking about it, I found out it made sense. After all, a 3% dividend yield is 60% of 5% and $6,000 is the same percentage (60%) of $10,000. On year 1, both portfolio would generate the same amount in dividend income, so $300. Then, both portfolio payments would grow at the same pace assuming the same dividend growth rate.

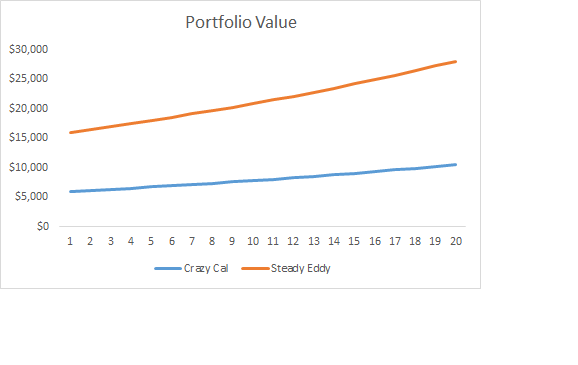

However, there is more thought to be added to such rationale. The first one is the end portfolio value. While both portfolios generate the same income, Steady Eddy ends up with over $7,000 more than Crazy Cal after 20 years:

This means that Steady Eddy could start withdrawing from its capital and boosts its yearly income for several years before getting back to Crazy Cal’s level. Even if Steady Eddy doesn’t touch its capital, then his heirs will still be happier to receive a bigger amount ;-).

The second point to consider is the dividend growth rate. It is unlikely to happen that a set of companies paying a 5% yield will increase at the same rate as a set of companies paying a 3% dividend yield. The rationale behind this statement is simple, but so true: higher yielding stocks always come with additional risk. This is one of the basics of finance 101: when an asset is riskier, the expected return by investors must be higher. This is also the case with the dividend payment. I’m not saying it’s impossible that you find a few companies that challenge my theory, but I’d be quite curious to see a portfolio of 10 companies showing a 5% dividend yield 10 years ago and posting an 8% dividend growth rate since then.

Overall, Ron’s rationale makes sense. However, I think that a short story is always more complicated when you factor everything in. There is rarely a black & white answer when you discuss investing strategies.