In my last article, I discussed the first steps to transform a retirement portfolio into a retiree’s portfolio. Today, I’m going to press fast forward on my current pension account and see what changes I would make if I was going to retire tomorrow. Let’s imagine for a minute that I wake up at the age of 64 and in 364 days I will retire and expect to live another 20. Let’s see what can I do to make my portfolio “retiree lovely”.

Let’s start by looking at my current holdings… not retiree lovely!

I’ve taken the holding I show in my latest January income report:

| Company Name | Ticker | Sector | Yield |

| Company Name | Ticker | Sector | Yield |

| Alimentation Couche-Tard | ATD.B.TO | Consumer Defensive | 0.58% |

| Andrew Peller | ADW.A.TO | Consumer Defensive | 1.24% |

| Royal Bank | RY.TO | Financial | 3.60% |

| Canopy Growth Corp | WEED | Healthcare | 0.00% |

| Enbridge | ENB.TO | Energy | 6.08% |

| Fortis | FTS.TO | Utility | 4.10% |

| Lassonde Industries | LAS.A.TO | Consumer Defensive | 1.00% |

| Magna International | MG.TO | Consumer Cyclical | 2.09% |

| Shopify | SHOP.TO | Technology | 0.00% |

| Apple | AAPL | Technology | 1.53% |

| Disney | DIS | Consumer Cyclical | 1.54% |

| Gentex | GNTX | Consumer Cyclical | 1.73% |

| Hasbro | HAS | Consumer Cyclical | 2.22% |

| Honeywell | HON | Industrial | 1.80% |

| Lazard | LAZ | Financial | 2.80% |

| Microsoft | MSFT | Technology | 1.77% |

| Starbucks | SBUX | Consumer Cyclical | 1.92% |

| Texas Instruments | TXN | Technology | 2.17% |

| United Parcel Services | UPS | Industrial | 2.95% |

| Visa | V | Technology | 0.57% |

| Average | 1.98% |

Let’s pretend that I rebalance all my holdings to have equal value for each position. Let’s assume I have $1M invested and I need to generate $50,000 per year. I also want to keep up this $50,000 with a 2% inflation rate.

Therefore, my average yield would be 2%. I have 2 stocks not paying dividend and 3 paying 1% or less. This is a problem if I’m going to retire tomorrow. As a young retiree, I will want to earn a lot more in dividend as I will not aim at selling all my precious shares to generate the bulk of my income.

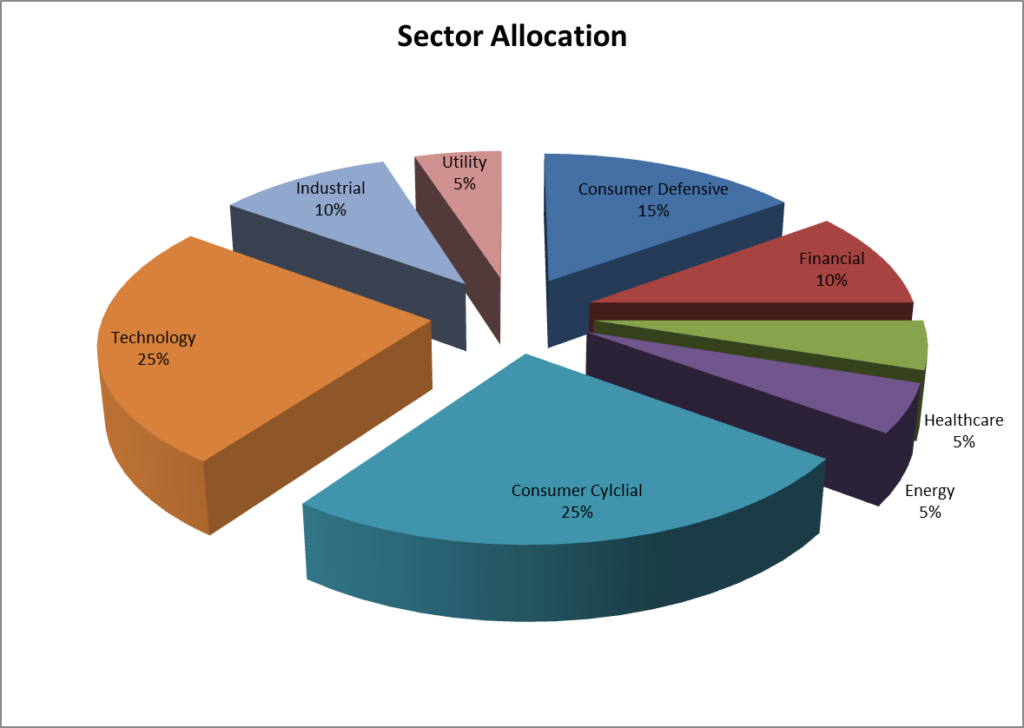

The second problem I have is the concentration in some sectors:

I obviously have an important concentration in techno and consumer cyclical stocks. While those sectors are perfect for what I want to achieve now (e.g. growth), they are more likely to provide additional volatility too. As a young retiree, I don’t want that. Canopy Growth (WEED.TO) is considered to be part of the healthcare sector… let’s just say I don’t have any in this sector!

Now… let’s see how I can modify my portfolio to A) generate higher yield and B) diversify my portfolio in order to avoid a big drop at a bad moment for me.

Which stocks am I dropping?

To be honest, when my friend pitched me the idea of making a “retire now” portfolio, I thought it would be easy. I thought I would simply change a few stocks and then write my article within an hour. But it turns out that changing an existing portfolio toward an income generating machine isn’t that easy.

My first goal was to raise my average yield over 3%. My second goal was to change my sector allocation to make sure I would not suffer from a crash due to a single industry.

| Company Name | Ticker | Sector | Yield |

| National Bank | NA.TO | Financial | 3.85% |

| Emera | EMA.TO | Utility | 5.22% |

| Royal Bank | RY.TO | Financial | 3.60% |

| Bell | BCE.TO | Telecom | 5.06% |

| Enbridge | ENB.TO | Energy | 6.08% |

| Fortis | FTS.TO | Utility | 4.10% |

| Telus | T.TO | Telecom | 4.46% |

| TFI International | TFII.TO | Industrial | 2.73% |

| Apple | AAPL | Technology | 1.53% |

| Disney | DIS | Consumer Cyclical | 1.54% |

| Procter & Gamble | PG | Consumer Defensive | 3.37% |

| Hasbro | HAS | Consumer Cyclical | 2.22% |

| 3M | MMM | Industrial | 2.33% |

| Lazard | LAZ | Financial | 2.80% |

| Microsoft | MSFT | Technology | 1.77% |

| Starbucks | SBUX | Consumer Cyclical | 1.92% |

| Texas Instruments | TXN | Technology | 2.17% |

| United Parcel Services | UPS | Industrial | 2.95% |

| Pepsi | PEP | Consumer Defensive | 2.84% |

| Average | 3.19% |

As you can see, I’ve made a lot of changes. The first thing I did was get rid of low yielding stocks:

- Alimentation Couche-Tard

- Andrew Peller

- Canopy Growth

- Lassonde Industries

- Shopify

- Magna International

- Honneywell

- Visa

- Gentex

Yup… that’s 9 stocks out of 20… nearly 50% of my portfolio! You can see how having so many low yielding stocks could be problematic when you try to generate income! I also “sold” one position to have the equivalent of 5% in cash.

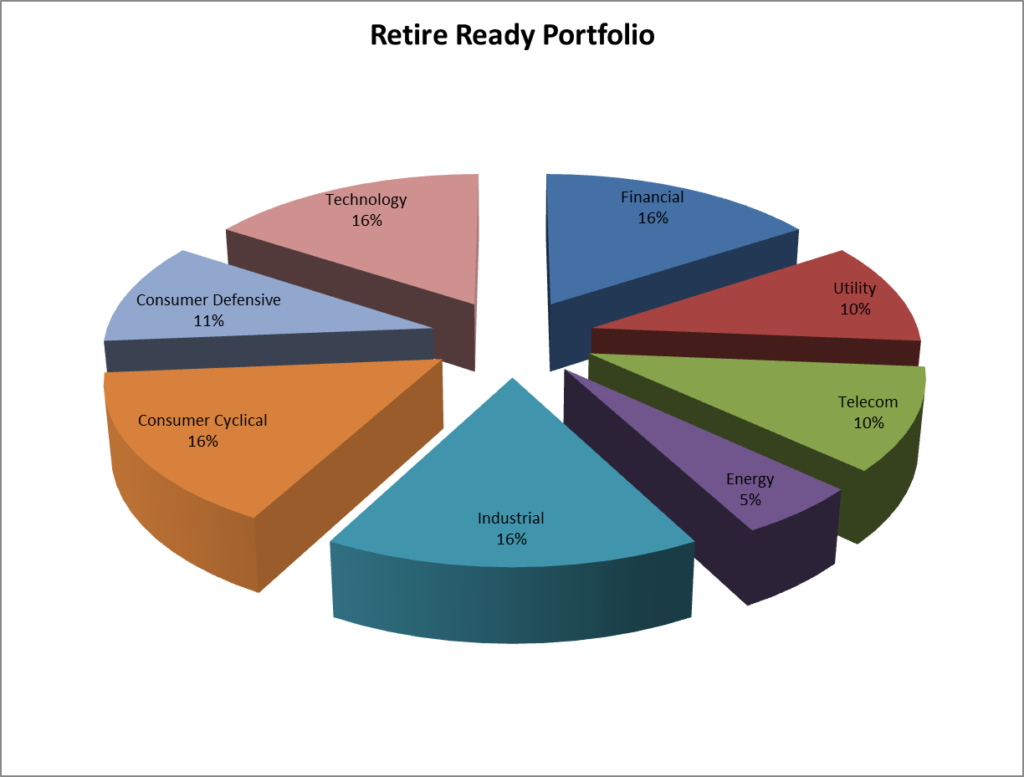

I’ve added companies with higher yield, but that still show positive dividend growth over the past 5 years. National Bank will increase my exposure to Canadian bank. Emera will boost my average with a 5%+ yield. BCE and Telus are 2 great yielders that are part of an oligopoly. This is perfect for stability. I decided to sell Magna and replace it with TFI international as I rather get a higher dividend yield from a trucking company. On the US side, I’ve played it safe by adding classic dividend payers with Procter & Gamble, 3M Co and Pepsi. The new sector allocation is a lot more diversified as no industry represents more than 16% of the portfolio:

The new portfolio is “Retire Ready!”

Imagine that I have $1M in my portfolio. I now have 19 stocks for $50,000 each and a $50,000 in cash. This allows me to withdraw money from my portfolio on a monthly basis without worrying about the current state of the market.

The remaining $950K invested would generate roughly $30K per year. This amount will certainly keep up with inflation as all my 19 stocks are known to increase their dividend on a regular basis. Each year, I will only have to sell for $20,000 or 2% of my portfolio to finance my lifestyle. You don’t need to be a math geek to know that you will have enough to live for more than 20 years with this kind of plan.

Final Thoughts

This was a fun exercise and I realized it was more complicated than I thought. Starting from an existing portfolio aimed at growth and transform it into an income machine isn’t an easy task. I’m sure you have some suggestions of other stocks I didn’t include in this portfolio.

In the last part of this series, I will make a list of my Top 10 “retire ready” stocks for each market. Stay tuned!

The post The Portfolio I Would Build if I Retire Today Part II appeared first on The Dividend Guy Blog.