Warning: this article will not be easy to read for most of you. You will likely deny making this investment mistake. Yet, you keep doing it and losing money without even realizing what’s happening.

I’m not reciting classic investing mistakes with some generic solutions. I’m attacking the top investing mistakes I’ve seen across the DSR community over the past 6 years. This post covers one investing mistake you keep making and this seriously hurt your portfolio… without you knowing it!

In the following pages, I will not only identify what most investors do wrong, but why they do it and how it hurts their retirement plan. The worst mistakes are often the ones we don’t see. You don’t even realize it’s a mistake since it’s not making you lose money right away. The impact is only visible over a long period of time. It’s like my eternal battle with weight loss.

I’ve been trying to lose weight for several years. It’s a classic resolution most of us make and then forget along the way. The thing is that I don’t forget about it. I even have a plan to make sure I achieve my goal! Over the past 10 years, I’ve made sure to “stay in shape” as I was going through my 30’s. I had been going to the gym regularly until I eventually built one in my basement. I’ve been running 3-4 times a week and even completed a half-marathon. Last year, I ran a total of 735.3km. Not bad for a guy who lives in a country where winter lasts 4 months a year!

Do you know how many pounds I lost? None. For all those years, all I have been able to do is to maintain the same weight. I always had a solid training plan and followed it. Nevertheless, my story is like Groundhog Day. Do you know why?

I make the same “invisible mistake” each year.

Sometimes it is called “the weekend”, and sometimes it is “a good glass of wine by the terrace”. But each year, the mistake I make is not about training intensity, the quality of my plan or my diligence. The mistake I make is about eating too much.

You may feel your portfolio is in good shape. In fact, if it is not it would be quite surprising considering how great the stock market has been to all investors over the past decade. This is the market covering up for your mistakes. Lucky for you, there is still time to solve those issues and get your portfolio on the right track.

I know very well the following investing misstep as I’ve experienced it during my investing journey. We usually say that the ultimate result of a mistake is to allow us to learn something. Let’s explore together those major errors and learn how you can fix your portfolio.

Buy low, sell high

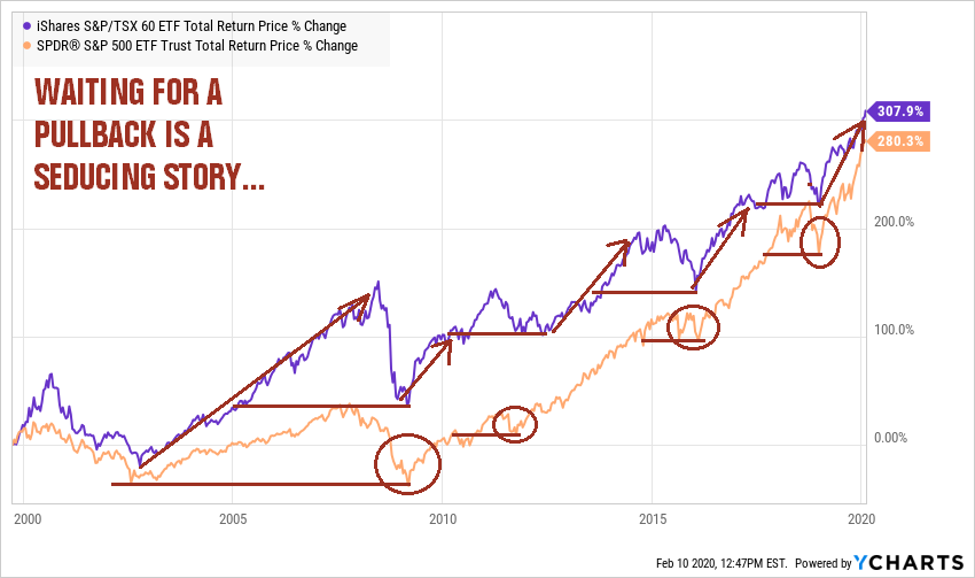

“Buy low, sell high”. That is the most basic and sound investing advice we can give to anybody starting their investing journey. Now, what do you do when the stock market keeps going higher and higher? You are not going to buy high (and sell low), are you? This is how you end-up waiting for a pullback.

Why are you doing this?

History is filled with investing horror stories. During the past 20 years alone, we had the “chance” of running into the tech bubble, the Twin Tower terrorist attack, the 2008 financial crisis, the oil bust in 2015 and we are about to see how fast this aging bull market might crash. Keeping cash aside for the next crash tells a seducing story: you will buy shares at an incredibly low price and they will eventually go back up and generate strong returns. After all, why would you buy now, if you can buy later at a cheaper price? Plus, keeping 30% of your money in cash doesn’t make you lose money. It looks like a win-win situation as you get paid (e.g. mediocre interest rate) on your cash and you will eventually get bargains in the stock market.

Source: Ycharts

For an inexplicable reason, most investors keep referring to what happened in 2008-2009 as the norm for a market crash. They expect the next bear market to be fast and furious (pun intended). Therefore, all you need to do is to wait for a few months until the bleeding stops. Then, you put all your money in, and you feel like a king.

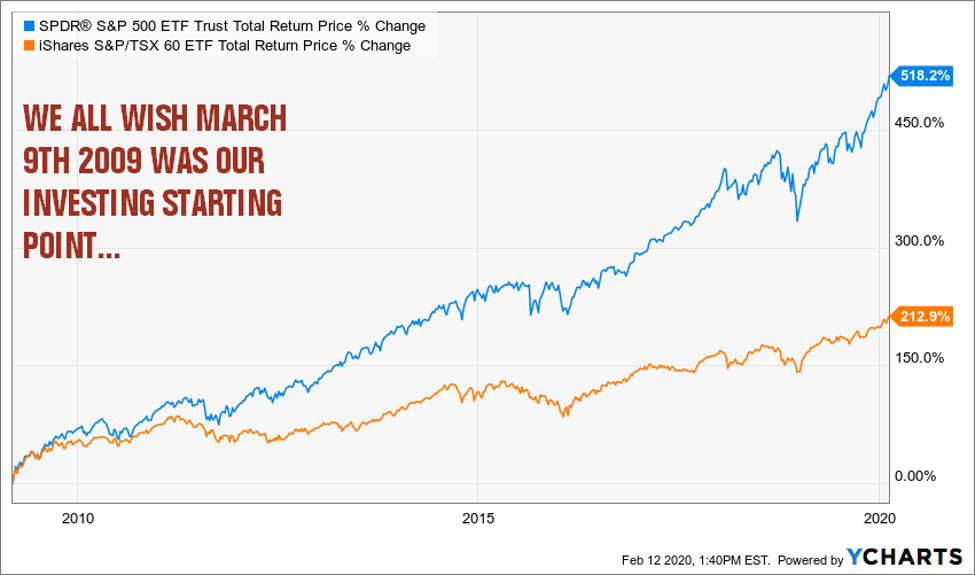

Source: Ycharts

The Canadian market tripled in value while the U.S. market soared by 500%. This is enough for any investors to be “set for life” if they played their cards correctly back in 2009. When you look at this graph, waiting for a pullback makes total sense. Unfortunately, you are wrong.

How it hurts your portfolio

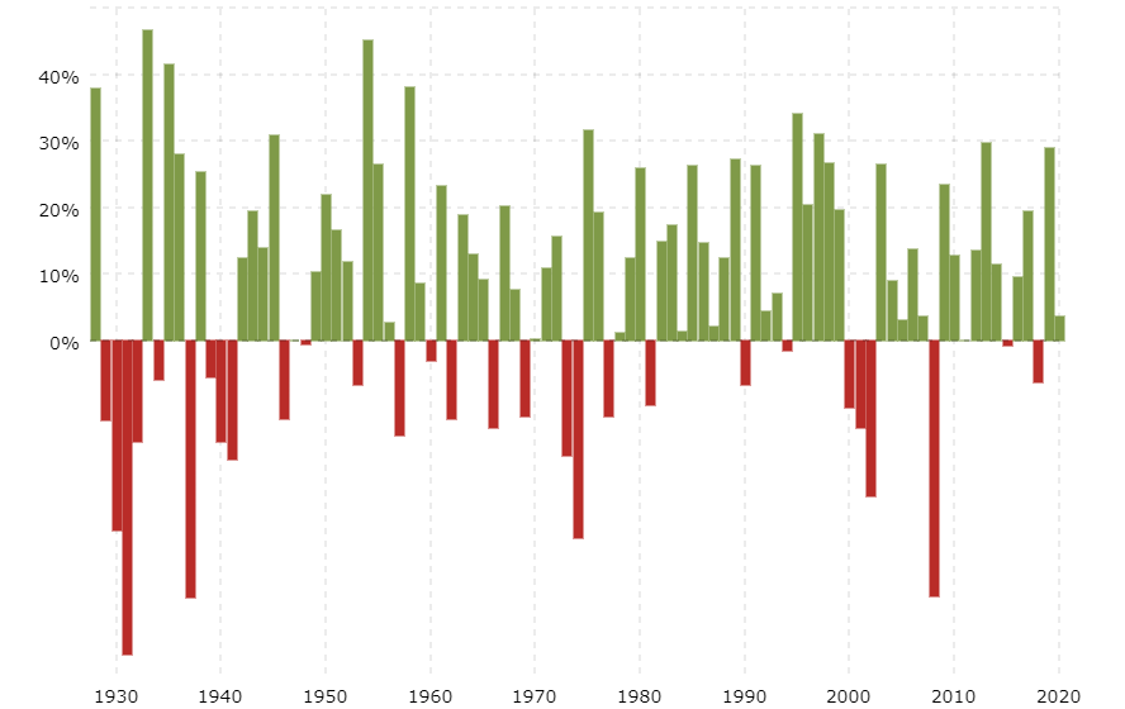

If a year like 2009 happened every 5 or even every 10 years, waiting for a major pullback would be a defendable strategy. After all, any investor who put his money to work in 2009 shows impressive results today. I remember that the famous Canadian Banks were offering yields of between 7% and 9% at their bottom. Just the thought of buying Royal Bank (RY.TO) with a 7+% yield makes me smile… but it is unlikely to happen. In fact, this happened only once in the past 25 years. Waiting for such a pullback to get “market deals” is more like hoping to see the Habs win the Stanley Cup… (this also happened once in the past 25 years). The problem is that we rarely have the chance of investing after a major stock market correction.

Source: Macrotrends

Since 1970, there have only been 3 interesting pullbacks that would have been worth the wait (1973-74, 2000-01-02 and 2008-09). Imagine if the market correction of 2018 happened in a similar timing to the one in 1990. This would mean that you would be waiting another 9 years before a market crash. Can you afford waiting another decade before investing? Do you think the next market crash will bring prices back to the 90’s? Here’s my blunt answer; it won’t.

But waiting has a more important impact on your portfolio: it inserts doubt into your investing plan. You want an example? How many of you (or your friends) invested all their available money on December 26th 2018? After both markets showed a strong double-digit decrease from their peak levels. Wasn’t that the pullback you were waiting for? Like most of us, you didn’t know that the end of 2018 would mark the start of another bullish segment. You probably didn’t invest more money in December 2018 because you started thinking about the possibility of another 2008. Even worse, what if the market moved into another bear segment like the one in 2000-2002?

Waiting for a pullback will do one thing: make you wait to invest. Nobody will come around raising a flag and tell you it’s now the time to pull the trigger. Therefore, why are you waiting?

How can you fix it?

DSR was created back in 2013. Between 2013 ad 2014, most financial analysts and the media said the market was overvalued. You could find some juicy quotes back then:

“Of course, with stocks at all-time highs, some seem to have nowhere to go but down.”

~Business Insider (2013) (quote from Goldman Sachs)

“At ValuEngine.com we show that 77.8% of all stocks are overvalued, 45.2% by 20% or more. All 16 sectors are overvalued; consumer staples by 17.6%, retail-wholesale by 26.4% and utilities by 9.8%.”

~ Forbes (2013)

“The market has jumped nearly 30%. This means the stock market’s rally has been based solely on people paying more money for the same amount of earnings — this is known as “P/E multiple expansion.”

~ Motley Fool (2013)

In 2017, I officially quit my job as a private banker and invested 100% of the commuted value of my pension plan in dividend growth stocks (read how to invest 100K for the full story). Then again, everybody agreed the market was way overvalued back then. In other words, most investors agreed the market was overvalued for 4 consecutive years. What do those people say today?… you know it already.

I know my situation is a unique case study and this doesn’t prove any trends in the market. I still found it very interesting that even after the terrible year we had in 2018, I was better off being fully invested during all that time than if I had waited with 30% to 50% of my portfolio in cash to invest on the day after Christmas. The money my portfolio made between the end of September 2017 and the summer of 2018 combined with the dividend payments I’ve received was more than enough to cover any temporary losses incurred during the second portion of 2018. I ran many calculations and none of them showed that waiting would have been a valid strategy.

As was suggested in a previous article, what you should do when you think you shouldn’t invest money is to focus on your dividend growth plan instead of the stock value. Back in 2017, I didn’t mind where the market was. I used the DSR portfolios and the stock cards to build my own portfolio. I selected among the finest dividend growers at that time. Even if the pullback happened 3 months after I invested my money, I knew my dividend payments would only continue to increase during the correction. Sooner or later, share values would go back up… because this is what has happened repeatedly over history.

Investing with confidence will prevent you from waiting for a pullback. You can look at our portfolio returns. You will see that even during the market correction of 2018, our portfolio minimized your losses by focusing on dividend growing stocks.

The best protection there is against a market crash is a solid portfolio. One way to build such portfolio is to select companies with robust dividend growth. A quick search across our free stock list

You can then select the first line (row #1), click on “Sort & Filter” and select “Filter”. This way, you can sort all stocks by revenue growth, EPS, dividend growth, payout ratio or cash payout ratio, etc.

Going through this list by selecting only the strongest dividend growers will increase your protection against the upcoming market crash. I’ve already pre-screened the market for you and identify the strongest dividend growth stocks. You can download the excel list by subscribing to my newsletter. It’s 100% free and the stock list is being updated weekly!

Download my Stock List with metrics

The post The Invisible Mistake You Keep Making appeared first on The Dividend Guy Blog.