What’s the worst thing that could happen to a retiree?

a) 2 golf balls in the lake the same day

b) A Barista at Starbucks putting cinnamon topping with whole milk on his Non-Fat Vanilla Latte

c) Outliving his savings

Once you retire, it’s finally time to enjoy life. It’s time to relax, do what you love most and stop stressing. Unfortunately, this definition of retirement is pretty rare. Most retirees still have to work to fill the hole in their budget and others worry about how long they can hold on to their savings before the well dries-up.

The answer to this question is often answered by two factors you can control:

a) how much do you withdraw per year and;

b) how you are invested (asset allocation)

For those who choose dividend investing; this is good news. If you have a well diversified portfolio, your dividend payouts should increase over time protecting your lifestyle from inflation. Plus, your capital shouldn’t move enough to worry you. But if you have chosen to put most of your investment in a “safe place” such as bonds; you might outlive them.

The Bond that Will Kill You

There is nothing safer than an investment in a bond, right? Pick a Gov’t bond which is guarantee beyond reason and you will never lose money. On paper, you are right about 99% of the time. If you buy a Gov’t bond at any level (even municipal), you are pretty sure that you will not lose your capital.

But the issue at retirement is far bigger than protecting your capital; we are talking about protecting your lifestyle. I found some interesting stats on Canadian bonds that will show you we are not in the right place to invest for the years to come. This article is also good for Americans as we are in the same boat in terms of interest rates.

What Happened Before and After 1981

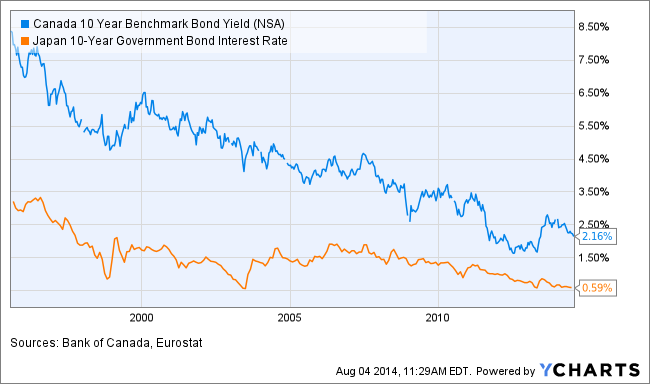

Funny enough, 1981 is the year of my birth. More importantly, this is the year where the world of bonds changed for a very long time. Between 1950 and 1981, the 10 year Canadian bonds yielded 3.8%. From 1981, the year when interest rates spiked higher than the Rockies, to 2013; the same 10yr Canadian bonds generated a 9.6% yield. By comparison, stocks did 9.2% for the same period.

For 30 years (starting in the 50’s) the interest rates in Canada (and US) climbed a long mountain to reach its peak in ’81. Investors lost on bond value but gained on higher interest rate year after year. However, starting in 81, rates started to drop. I was able to find a 10yr Canada bond graph since 1995:

The line is pretty obvious here: it has gone down big time. So the best move in the early 80’s was to buy long term bonds and watch them grow in value year after year. This is why bonds yielded so much during this period.

What Will Happen in the Next 10-20 Years

Since 2008, bond rates have kept on falling to the lowest level we’ve seen in a long time in 2012-2013. Now that we have reached the bottom, there is only one place to go: higher.

When you think about it; this means investors are stuck with 5 years of incredibly low yield in their portfolio and a big wave of dropping value ahead. There are no winning bids here: either you sell at loss, or you keep your low interest yield barely covering inflation for the next 10 years.

The risk for retirees is here: chances are you will get stuck for a 10-20 years period where interest rates will rise or worse, will stabilize at a very low yield (anybody see what happened in Japan for 20 years?).

So don’t think we only have a few years of low interest rates and this is going to end. Japan has been stuck in this turmoil for the past 20 years.

What Can You Do if You Have Bonds

You don’t have many choices;

a) make sure you don’t need much capital so you can count on the low interest yield and live happy

b) return to work again to compensate for the gap between the expected investment return and the real investment return

c) sell your bonds and move towards other types of securities (dividend stocks, real assets, non-traditional asset classes, etc)

This won’t perform miracles overnight (after all, dividend stocks will also drop one day), but, over time, you may end-up with a much higher yield with stocks than with other asset classes such as bonds for the next decade at least!

I’m 100% stocks right now and I’ll keep it this way, what are you going to do?