If you are a regular of this blog, you know that each year, I pick 30 stocks to beat a dividend ETF in the upcoming 12 months. Each year, I select 20 U.S. and 10 Cdn stocks and try to build a portfolio. So far, I have a great batting average where I had failed to beat my benchmark only twice (one on each market) since 2012… That was before 2017. Unfortunately, I failed to beat both markets last year. I went a little too aggressive on both selections and 1 pick in each portfolio nailed my results.

Author’s creation.

A look at 2017 performances

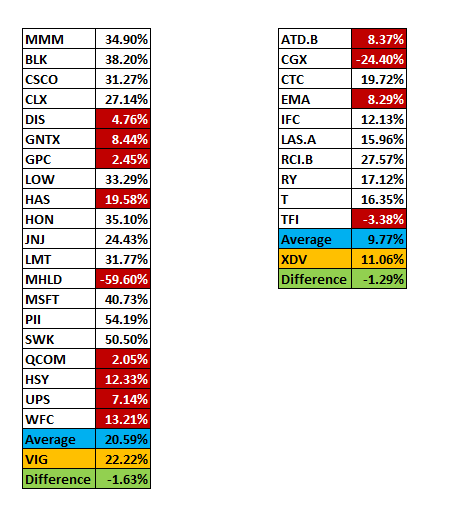

As I just mentioned, my performance in 2017 were below my expectations. When I look at my overall results, a single pick in each portfolio crushed my hope of beating my benchmark.

As you can see, I lagged my benchmarks by 1.63% and 1.29%. When you look at the overall performances, I have picked 11 companies out of 20 (55%) that beat the VIG and 6 companies out of 10 (60%) that beat the XDV. By taking off the worst performing stock in each portfolio (MHLD and CGX.TO), I would have beat both benchmarks by more than 1%.

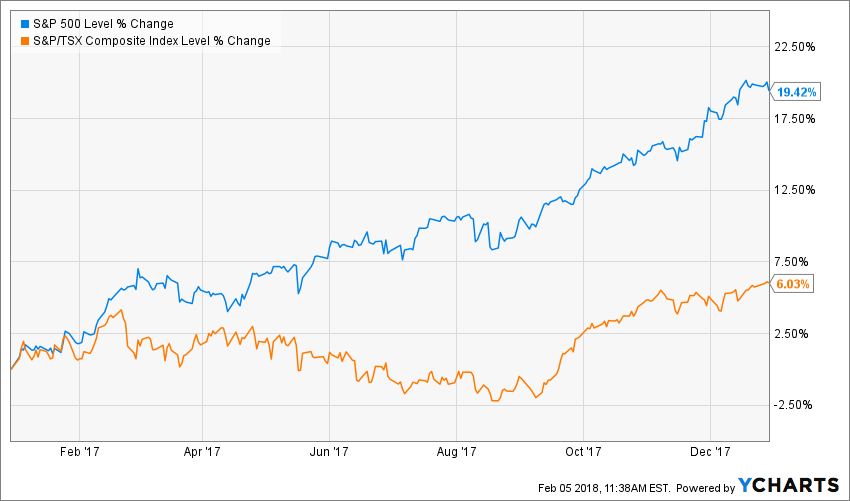

This is not an excuse, but it shows you how easily you can make one mistake in your portfolio and underperform the market. On the other, I couldn’t really complain when my portfolios did 20% and nearly 10% return last year. At least, both portfolios beat the market:

Source: Ycharts.

Now, what about my 2018 book?

I have a feeling that my book is getting larger year after year. It’s the second issue with 2 pages analysis per stock. Each pick is represented in a similar way that we do at Dividend Stocks Rock with our stock cards.

I kept the idea of having 20 U.S. picks and 10 Canadian candidates. The whole book is over 15,000 words across 65 pages of content. Here’s an example of what you will find over there:

STARBUCKS (SBUX)

Business Model

I don’t only love Starbucks coffee; I love the whole company and its business model. SBUX is one of the rare restaurant success stories. Founded in 1971 by the opening of the first coffee shop at the iconic Seattle Pike Place Market, it now operates 22,519 stores in 75 countries. Starbucks is known for its stellar customer experience and its variety of beverages. It built a reputation of listening to its customers and using technology (Facebook, Twitter, mobile payment) to continuously improve its in-store experience.

Main Strengths

I first discovered SBUX as an investment when I compared it to McDonald’s (MCD). I’ve discovered a company that is moving fast (opening new stores everywhere), that is flexible (through its various menu offering and stores size) and whose sole purpose is to adapt to please its clientele (through their mobile app, membership program and social media). There is a reason why Starbucks has built an iconic brand in such a short period of time; because it is willing to do whatever it takes to stay close to its customers’ ever evolving tastes.

Potential Downsides

SBUX growth potential in the U.S. is nearly nonexistent. There is a limit to the amount of coffee that can be purchased by an American! Therefore, if the company faces headwinds in China or India, its growth potential will be highly reduced. The stock price is still at a PE of 28 (forward PE at 26.70); a loss of interest from the market could also hurt the valuation temporarily.

Dividend Growth Perspectives

Just by saying that management increased their dividend by 25% toward the end of 2017 is enough to convince me. SBUX shows a low payout can cash payout ratios along with a robust double-digit dividend growth rate over the past 5 years. The company is generating enough cash flow to fund both its stores’ growth and its aggressive dividend policy. SBUX is a keeper for years.

Investment Thesis

Starbucks’ future is still bright. The company is currently growing fast in China and there is no reason it won’t continue to do so. Therefore, while SBUX can continue to optimize their U.S. offering (store sizes, menus, etc.), it will open new stores in China where 1.3 billion people will start enjoying high quality coffee. The dividend yield is almost at 2% now with a great perspective of payout increase during their next quarterly report.

Valuation:

| Intrinsic Value | Discount Rate (Horizontal) | ||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $152.16 | $90.07 | $63.51 |

| 10% Premium | $139.48 | $82.56 | $58.22 |

| Intrinsic Value | $126.80 | $75.06 | $52.93 |

| 10% Discount | $114.12 | $67.55 | $47.63 |

| 20% Discount | $101.44 | $60.04 | $42.34 |

Upon management’s latest dividend increase announcement, we have decided to increase the 10 year dividend growth rate to 12%, and reduced the long term rate to 7.50%. SBUX may scare you with its high PE, but keep in mind that the company will continue to grow at a rapid pace throughout the next decade.

ANDREW PELLER (ADW.A.TO)

Business Model

Andrew Peller (ADW.A.TO) owns wineries in British Columbia, Ontario and Nova Scotia. It doesn’t only produce its own wine, but also markets it along with other products. ADW owns several brands like Peller Estates, Trius, Hillebrand, Thirty Bench, Sandhill, Copper Moon, Calona Vineyards Artist Series VQA wines and Red Rooster. Currently the company has an estimated 14% share of the total wine market, and a 37% share of domestic wines. The company is known to grow its revenues through acquisitions. Since 1995, management invested over $114M to purchase 14 vineyards.

Main Strengths

The company has built a solid relationship with provincial liquor stores, but also maintains company-owned retail stores in Ontario. Andrew Peller shows a strong and steady growth of its sales mainly due to the creation of multiple products, a strong marketing program, and several acquisitions. The Canadian wine business is doing well and ADW continues to ride this bullish trend. Its recent alliance with Wayne Gretzky vineyard will not only be good for wine sales, but will also open the door to whisky production.

Potential Downsides

The wine industry and the domestic and international market in which the Company operates are consolidating. While this could be a great opportunity, it also brings stronger competitors to the table. ADW must continue investing in its brands to keep its market share. Since Wine is a luxury product, any economic downturns would affect ADW sales. For now, I don’t think it’s an issue as the Canadian economy has proven to be more resilient than anticipated.

Dividend Growth Perspectives

Wow… such a low dividend yield for this wine company. Does it even make sense to invest? Well, if I sell you that while the yield went down from 3.75% to 1.28%, the stock price surged 260% over the past years, would you be more lenient? The dividend payment also increased by 36% or 6.34% annualized growth rate during the same period. After investing massively in their brand and new wines, ADW will most likely reward shareholders with another dividend raise in 2018.

Investment Thesis

In all honesty, ADW seems a bit pricey right now. When you find a company growing at this pace, it’s hard to not pay a premium. However, it seems the wine isn’t that pricey these days. It could be a good timing to buy some bottles. I think management is building a great future for this company with constantly growing through acquisitions and surfing on the growing wine trend in Canada. An investment in ADW, is buying the leader of a growing market, you can’t go wrong.

Valuation:

| Intrinsic Value | Discount Rate (Horizontal) | ||

| Margin of Safety | 8.00% | 9.00% | 10.00% |

| 20% Premium | $27.62 | $13.72 | $9.09 |

| 10% Premium | $25.32 | $12.57 | $8.33 |

| Intrinsic Value | $23.01 | $11.43 | $7.57 |

| 10% Discount | $20.71 | $10.29 | $6.81 |

| 20% Discount | $18.41 | $9.14 | $6.06 |

Where Can You Download the Book?

I think that getting the stock picks is great, but learning how to select those companies by yourself is the real deal. For that reason, I don’t sell the Best 2018 Dividend Stocks book alone anymore. I package it with the Dividend Toolkit. The toolkit will give you the methodology to pick the right companies and the Best Dividend Book will have done the job for you this year. Isn’t that cool?

You can get both copies for $19 right here:

CLICK HERE TO GET BOTH BOOKS FOR $19 USD

The post The 30 Best Dividend Stocks for 2018 appeared first on The Dividend Guy Blog.