I have now finished my Canadian telecom dividend tour with this analysis of Telus. You can read the other analysis here:

Shaw Communications (SJR.B.TO)

Rogers Communication (RCI.B.TO)

BCE (BCE.TO)

What Makes Telus (T) a Good Business?

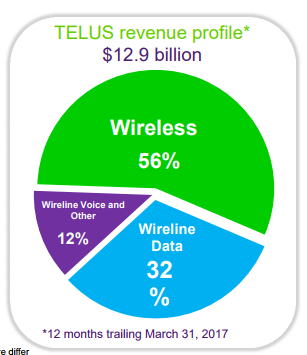

Telus is what is closest to being a pure play in the Canadian wireless industry. With 56% of its revenue coming from this segment, Telus has made a very good job at growing its business in the most profitable telecom & media segment.

source: 2017 Fact Sheet

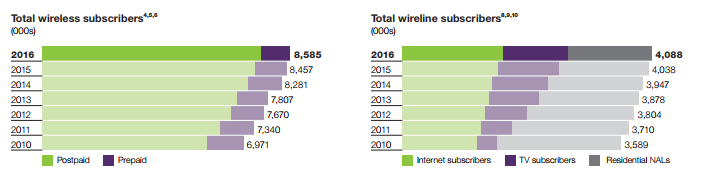

Telus is very well aware of this situation and makes sure to keep very strong client service to keep everybody happy. I guess it works as the number of clients never stops increasing:

source: 2016 annual report

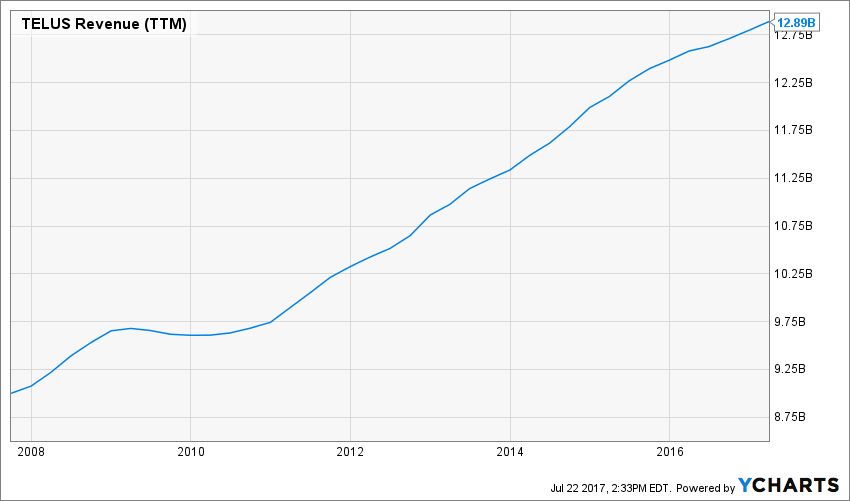

Revenue

Revenue Graph from Ycharts

As you can see, Telus has been showing a consistent and growing revenue trend. There is still room in the wireless industry as Canadian smartphone adoption rate is now at 76%. Over the past couple of years, Telus has also invested in their television and internet services to compete (and grab clients from) Shaw Communications.

How Telus fares vs My 7 Principles of Investing

We all have our methods for analyzing a company. Over the years of trading, I’ve been through several stock research methodologies from various sources. This is how I came up with my 7 investing principles of dividend investing. Let’s take a closer look at them.

Source: Ycharts

Principle #1: High Dividend Yield Doesn’t Equal High Returns

My first investment principle goes against many income seeking investors’ rule: I try to avoid most companies with a dividend yield over 5%. Very few investments like this will be made in my case (you can read my case against high dividend yield here). The reason is simple; when a company pays a high dividend, it’s because the market thinks it’s a risky investment… or that the company has nothing else but a constant cash flow to offer its investors. However, high yield hardly comes with dividend growth and this is what I am seeking most.

Source: data from Ycharts.

Telus has been able to push both its stock price and its dividend payment on a consistent basis over the past decade. This leaves Telus with one of the most appreciable dividend yield on the Canadian market.

Telus meets my 1st investing principles.

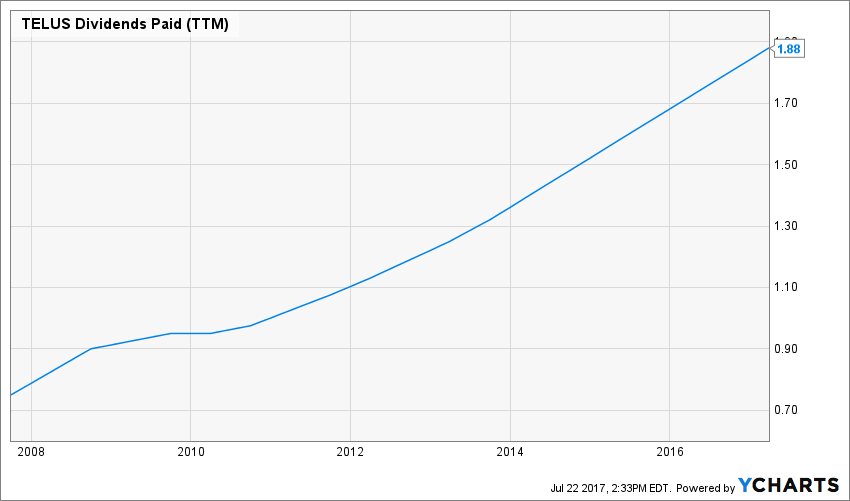

Principle #2: Focus on Dividend Growth

Speaking of which, my second investing principle relates to dividend growth as being the most important metric of all. It proves management’s trust in the company’s future and is also a good sign of a sound business model. Over time, a dividend payment cannot be increased if the company is unable to increase its earnings. Steady earnings can’t be derived from anything else but increasing revenue. Who doesn’t want to own a company that shows rising revenues and earnings?

Source: Ycharts

Telus is by far the Industry-best dividend payer and recently declared another increase of 7.1% to $0.4925 cents per share. This is the 13th dividend increase since 2011. Do I have to mention Telus is part of the Canadian Dividend Aristocrats? In fact, if it was based in the U.S., it would even make the cut for being part of the Dividend Achievers list.

Telus meets my 2nd investing principle.

Principle #3: Find Sustainable Dividend Growth Stocks

Past dividend growth history is always interesting and tells you a lot about what happened with a company. As investors, we are more concerned about the future than the past. this is why it is important to find companies that will be able to sustain their dividend growth.

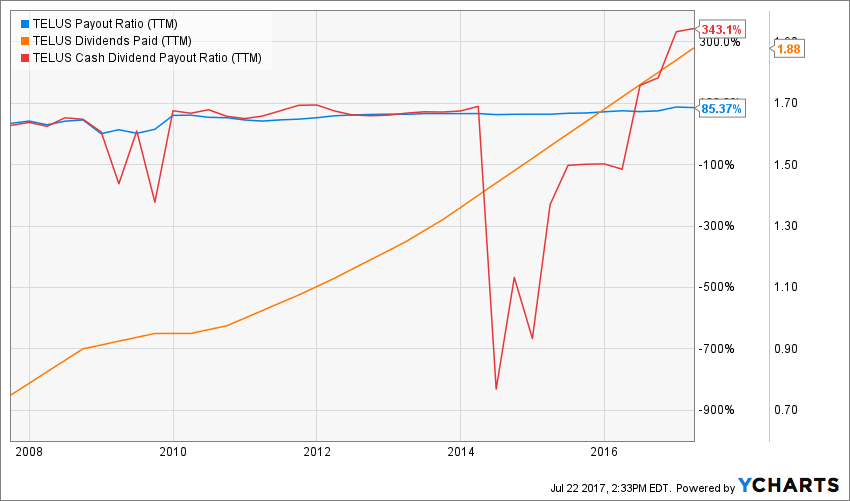

Source: data from Ycharts.

The company is showing a very high cash payout ratio as Telus invested more money than usual into investments and capital expenditure. Capital expenditures increased by $106 million in 2017 due to massive investment in broadband infrastructure and network enhancement. Such investments are crucial in this kind of business. Telus is basically filling the cash flow gap through financing for now. I’m not worried about this situation since management continued to raise its dividend and keep a payout ratio of 85%.

Telus meets my 3rd investing principle but we need monitoring.

Principle #4: The Business Model Ensure Future Growth

Telus has made the most profitable telecom segment its priority and main business model. Telus has proven its client service quality over the years and demonstrated its ability to retain its customers. Such a business model provides Telus with consistent cash flow incoming. While this business requires continuous investment to maintain and upgrade their network, Telus is in a solid position to continue its growth.

Telus still shows a strong business model and meets my 4th investing principle.

Principle #5: Buy When You Have Money in Hand – At The Right Valuation

I think the perfect timing to buy stocks is when you have money. Sleeping money is always a bad investment. However, it doesn’t mean that you should buy everything you see because you have some savings aside. There is valuation work to be done. In order to achieve this task, I will start by looking at how the stock market valued the stock over the past 10 years by looking at its PE ratio:

Source: data from Ycharts.

Looking at the company PE ratio, we can see how valuation has been increasing since 2010. While the company shows a strong business model, it seems that valuation is high at 21 PE.

Digging deeper into this stock valuation, I will use a double stage dividend discount model. As a dividend growth investor, I rather see companies like big money making machine and assess their value as such.

Here are the details of my calculations:

| Input Descriptions for 15-Cell Matrix | INPUTS | ||

| Enter Recent Annual Dividend Payment: | $1.97 | ||

| Enter Expected Dividend Growth Rate Years 1-10: | 7.00% | ||

| Enter Expected Terminal Dividend Growth Rate: | 6.50% | ||

| Enter Discount Rate: | 10.00% | ||

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $105.06 | $74.92 | $58.19 |

| 10% Premium | $96.31 | $68.68 | $53.34 |

| Intrinsic Value | $87.55 | $62.44 | $48.49 |

| 10% Discount | $78.80 | $56.19 | $43.64 |

| 20% Discount | $70.04 | $49.95 | $38.79 |

Source: how to use the Dividend Discount Model

Surprisingly, Telus still show a strong upside potential. This is mainly because management has made such a strong commitment towards increasing its dividend payouts year after year. An upside potential of 38% may seem a bit exaggerated but I have to reduce the dividend growth rates to 6% and 5% to get a fair value. I expect Telus to continue a high single-digit dividend growth in the upcoming years.

Telus meet my 5th investing principle with a potential upside of 38%.

Principle #6: The Rationale Used to Buy is Also Used to Sell

I’ve found that one of the biggest investor struggles is to know when to buy and sell his holdings. I use a very simple, but very effective rule to overcome my emotions when it is the time to pull the trigger. My investment decisions are motivated by the fact that the company confirms or not my investment thesis. Once the reasons (my investment thesis) why I purchase shares of a company are not valid anymore, I sell and never look back.

Investment thesis

Telus has been showing a very strong dividend triangle over the past decade. The company is able to grow its revenues, earnings and dividend payouts on a very consistent basis. Telus is very strong in the wireless industry and now attack other growth vectors such as the internet and television services.

Telus shows a solid investment thesis and meet my 6th investing principle.

Principle #7: Think Core, Think Growth

My investing strategy is divided into two segments: the core portfolio built with strong & stable stocks meeting all our requirements. The second part is called the “dividend growth stock addition” where I may ignore one of the metrics mentioned in principles #1 to #5 for a greater upside potential (e.g. riskier pick as well).

Telus is one of the rare companies showing both core and growth perspectives. It could really fit a core portfolio as it shows a stable business model with high dividend yield but you can also expect a stock price jump as the company continues growing.

Telus is both a growth and a core holding.

Final Thoughts on Telus – Buy, Hold or Sell?

If I have to buy only one Canadian telecom company, Telus would be my choice. I’ve been holding it since the beginning of my dividend portfolio and will stick to it for many years to come.

Disclaimer: I do hold Telus in my DividendStocksRock portfolios.