In September of 2017, I received slightly over $100K from my former employer, representing the commuted value of my pension plan. I decided to invest 100% of this money in dividend growth stocks.

Each month, I publish my results on those investments. I don’t do this to brag. I do this to show my readers that it is possible to build a lasting portfolio during all market conditions. Some months we might appear to underperform, but you must trust the process over the long term to evaluate our performance more accurately.

Performance in Review

Let’s start with the numbers as of March 6th, 2023 (before the bell):

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Portfolio value: $212,674.73

- Dividends paid: $4,614.03 (TTM)

- Average yield: 2.17%

- 2022 performance: -12.08%

- SPY= -18.17%, XIU.TO = -6.36%

- Dividend growth: +10.83%

Total return since inception (Sep 2017-March 2023): 95.55%

Annualized return (since September 2017 – 66 months): 12.97%

SPDR® S&P 500 ETF Trust (SPY) annualized return (since Sept 2017): 11.23% (total return 79.53%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 9.42% (total return 64.08%)

Dynamic sector allocation calculated by DSR PRO as of January 2nd.

Spring Break With a Spring Clean-Up

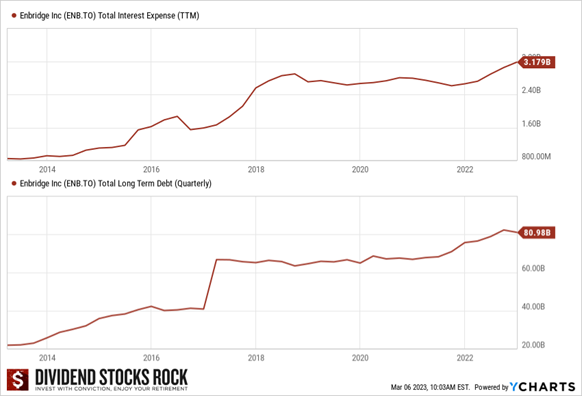

At the end of February, we performed our “spring clean-up” in our model portfolios with several trades. One of them raised many eyebrows: The sale of Enbridge (ENB.TO). Enbridge is NOT a “sell” or a “screaming sell”. My biggest problem with Enbridge is not the dividend safety but rather the growth potential. In the coming years, expenses will increase from the right, left, and center. Inflation of raw materials needed for new pipelines and pipeline maintenance, labor shortages (pushing for higher wages), and higher interest rates on debt are just a few examples. Delays in new projects (due to regulations and labor shortages) are also increasing costs, as explained in Enbridge and TC Energy’s latest quarterly earnings. You may think “but Mike, we need oil & gas, and those pipes aren’t going anywhere”. That didn’t prevent Inter Pipeline from slashing its dividend by 72% in 2020 and Kinder Morgan from slashing its dividend by 75% in 2015 (after claiming it was safe). Am I saying Enbridge is about to cut its distribution? Not at all. But at this point, I don’t expect extraordinary total returns to come out of Enbridge over the next 5 years. The company will likely continue to increase its dividend by 2-3% annually and grow slowly but surely (then again, you must review its earnings quarterly!). But besides a generous dividend, I don’t expect much growth. If you are happy with a deluxe bond (not much capital gain and a relatively safe dividend), then you’ll be happy with Enbridge. I see the debt increasing each quarter and the interest rates and expenses going up, and I think I can find a better candidate for my portfolio. Again, to each their own.

Sell ENB.TO to buy 140 shares of CCL.B.TO at $61.38

After selling my shares of Enbridge, I invested the proceeds into CCL Industries, another strong dividend grower. Did you know that there are only 14 companies that have increased their dividend for a longer period than CCL? Ironically, Enbridge is part of that select group! CCL shows 21 years of consecutive dividend increases and operates a business model around repetitive purchases (tapes, packaging, wrapping, and labels). CCL has a good dividend triangle and a double-digit annual dividend growth policy. It’s a low-yield, high-growth potential company that I would qualify as an educated guess for two reasons. #1, Its business model is highly dependent on commodity prices which explains why it’s part of the materials sector and not the consumer discretionary sector. #2, The company will likely see sales slowing down if we enter a recession as demand for its products will follow economic cycles.

Sell VFC to buy 8 shares of HD at $302.35

As I briefly discussed in my last update, VF Corporation preferred pushing its restructuring plan faster. While management expects revenue growth for the coming years, it decided to end 50 years of dividend increases with a dividend slash of 41%. Following my investing rules, I kissed this one goodbye (it wasn’t a big part of my portfolio anyway) and bought more Home Depot.

I bought VFC as a speculative play during the Covid crash. I believe in their iconic brands and their unique abilities in brand management. During that crisis, they spent more than $2B on buying Supreme, a logical move when you see what it did with Vans (propelled the brand with double-digit growth for several years). That reinforced my conviction in VFC’s business model and its ability to work through these challenging times and reward shareholders with more dividend increases. That dividend cut proved that I was mistaken in my investment thesis.

I already started a position in Home Depot in January with the proceeds from the sale of my shares of Gentex. I have now completed my position in HD. I still have Air Products & Chemicals on my buy list, but I prefer to complete my position and have a full investment in HD than to start a ~$2K position in APD at this time.

Smith Manoeuvre Update

The SM strategy is back! When you do any kind of leverage strategy, you must be sure to follow those rules:

#1 Have a long-term horizon (minimum 10 years) to benefit from an entire stock market cycle.

#2 Be comfortable with market fluctuations (your portfolio could go down 20%, it’s part of the game).

#3 Be comfortable financially (having an emergency fund + the ability to pay the debt without the asset).

I followed my rules and took a break after spending a bit too much in my lifetime memories with my family in Africa. I’m now back with a new $500 monthly starting March 1st!

After discussing with my accountant, I also decided to sell my position in Canadian Net REIT. REITs pay distributions, and you can’t deduct interest paid from them. While I knew that already, I was excited to add this fast-growing REIT. However, my accountant explained to me that it wasn’t that profitable considering the distribution and the accounting nightmare going forward.

I then added Canadian Natural Resources (CNQ.TO) and Telus (T.TO) to this play. Unlike Enbridge, CNQ is paying off its debt and offering a more generous dividend growth policy. Both companies have proven to be recession-resistant, but CNQ shows a better growth profile over the next 5 years.

Telus currently offers a yield above 5%, which is rare for this great telco. This is an excellent example of how you can benefit from market fluctuations to add a strong company with a wide moat and several growth vectors.

So far, the Smith Manoeuvre strategy works well as the portfolio shows a total return of more than 9% while I paid less than 6% in interest (which is tax deductible). My current interest rate is 6.72%, but I don’t expect it to stay high for several years. In the meantime, I’m buying great companies at a good price, and I can handle the interest rate.

The portfolio is slowly taking shape, with 6 companies spread across 5 sectors. I aim to build a portfolio generating ~5% in yield across around 15 positions. I will continue to add new stock monthly until I reach that goal.

Here’s my SM portfolio as of March 6th, 2023 (before the bell):

| Company Name | Ticker | Sector | Market Value |

| Brookfield Infrastructure | BIPC.TO | Utilities | $537.39 |

| Canadian National Resources | CNQ.TO | Energy | $491.16 |

| Exchange Income | EIF.TO | Industrials | $568.15 |

| Great-West Lifeco | GWO.TO | Financials | $620.84 |

| National Bank | NA.TO | Financials | $616.44 |

| Telus | T.TO | Communications | $491.58 |

| Cash (Margin) | -$50.60 | ||

| Total | $3,274.96 | ||

| Amount borrowed | -$3,000.00 |

Let’s look at my CDN portfolio. Numbers are as of March 6th, 2023 (before the bell):

Canadian Portfolio (CAD)

| Company Name | Ticker | Sector | Market Value |

| Alimentation Couche-Tard | ATD.B.TO | Cons. Staples | $23,442.70 |

| Brookfield Renewable | BEPC.TO | Utilities | $9,012.88 |

| CAE | CAE.TO | Industrials | $6,276.00 |

| CCL Industries | CCL.B.TO | Materials | $9,151.80 |

| Fortis | FTS.TO | Utilities | $9,319.50 |

| Granite REIT | GRT.UN.TO | Real Estate | $10,528.00 |

| Magna International | MG.TO | Cons. Discre. | $5,430.60 |

| National Bank | NA.TO | Financials | $12,431.54 |

| Royal Bank | RY.TO | Financial | $8,205.00 |

| Cash | $372.44 | ||

| Total | $94,170.46 |

My account shows a variation of +$1,338.59 (+1.44%) since the last income report on February 2nd. Many Canadian companies reported their earnings in February, so let’s look at them!

Brookfield Renewable rewards shareholders!

Brookfield Renewable reported another solid quarter with revenue up 10%, FFO per share up 6% and a 6% dividend increase! BEP continues to work on its pipeline of projects commissioning approximately 3,500 megawatts of new projects that are expected to contribute $45 million of FFO annually on a run-rate basis. BEP also continued to execute on its 19,000-megawatt under-construction and advanced-stage pipeline, which, along with its sustainable solutions pipeline, is expected to contribute approximately $235 million of FFO annually to Brookfield Renewable once commissioned. BEP is also working on $4.6B worth of asset recycling.

CAE is getting back on the growth track.

CAE pleased the market with strong revenue growth (+20%), but, most importantly, more robust profitability (EPS up by 47%). During the quarter, Civil signed training solutions contracts valued at $713M, including contracts for 14 FFS sales for a total of 43 as of the end of the third quarter of the fiscal year. Defense booked orders for $476.7M marking the sixth consecutive quarter with a book-to-sales ratio above one, and it continued to book new business across all domains. CAE is back on its growth track; they are paying down its debt (from $3.2B to $3B) and they have $1.4B in liquidity at the end of the quarter. Will we see a reinstatement of the dividend soon?

CCL Industries goes with a double-digit dividend increase!

CCL Industries ended the year with a 3rd consecutive record year. The company reported adjusted EPS up 3% and revenue was up 7%. Management also announced a 10% dividend increase! Most of the growth came from the CCL Segment (revenue up 7.2% on 1.8% organic growth, 2.2% on growth from acquisitions, and 3.2% positive impact from currency translation) and Avery (+33.3% on 2.6% organic growth, 27.1% acquisition and 3.6% currency). Unfortunately, results were offset by a decline in sales of 1.9% from Checkpoint (-2.2% organic) and Innovia (-10.7%, -12.2% organic). In 2022, CCL spent $287M on acquisitions, repurchased $200M in shares and invested $419M in CAPEX.

Fortis confirms strong guidance.

Fortis reported a good quarter, with EPS up 14%. The increase was due to rate base growth, higher retail electricity sales and transmission revenue at UNS Energy, higher hydroelectric production in Belize, and the timing of expenses at FortisAlberta. Fortis also benefitted from a stronger USD to bolster revenue and earnings. Management announced a $22.3B capital plan (CAPEX), representing steady rate base growth of 6% and supporting annual dividend growth guidance of 4-6% through 2027. We are up for another 4 years of growth with Fortis despite the looming recession.

Magna International got destroyed.

Magna International got destroyed on the stock market after reporting EPS down from $1.54 to $0.33. On top of that, Q1 EPS is expected to decline from Q4 as the company continues to encounter inflationary headwinds. The problem isn’t revenue growth (it was 5% this quarter), but rather compressed margins. This has been an ongoing problem for a while now and management seems unable to secure an effective fix. Management expects sales to continue to outgrow global light vehicle production and margins to expand by 230 basis points or more by 2025. Are you that patient? We have revised our rating from 4/4 to 3/3, considering the weak dividend triangle and the recent dividend increase of only 2%.

National Bank did okay.

National Bank reported a small decline (EPS down 3%), mostly due to higher provisions for credit losses and the impact of a tax expense arising from the Canadian government’s 2022 tax measures. PCLs totaled $518M, up 29% from $403M last year. P&C banking was up 10%, driven by growth in total revenues, partly offset by higher PCLs. Wealth Management was up 16% due to higher net interest income. Financial Markets were down 2%. U.S. & Intl markets were down $1M as growth in total revenue was more than offset by higher non-interest expenses and PCLs (mostly coming from Credigy).

Royal Bank is generating more profit!

Royal Bank is one of the rare banks reporting positive (yet adjusted) numbers (adjusted EPS up 7%). Results this quarter also reflected higher provisions for credit losses. Total PCL of $532 million increased $427 million from a year ago. P&C banking was up 8%, primarily attributable to higher net interest income driven by improved spreads from increased interest rates and average volume growth of 9% in loans. Wealth Management was up 3% on higher transactional revenue. Insurance was down 25% due to higher capital funding costs, partially offset by improved claims experience. Capital market was up 9%, primarily driven by a lower effective tax rate.

I did a complete review of the first quarter of 2023 for the big 6 Canadian Banks on my YouTube channel.

Here’s my US portfolio now. Numbers are as of March 6th, 2023 (before the bell):

U.S. Portfolio (USD)

| Company Name | Ticker | Sector | Market Value |

| Activision Blizzard | ATVI | Communications | $9,209.24 |

| Apple | AAPL | Inf. Technology | $11,327.25 |

| BlackRock | BLK | Financials | $9,733.36 |

| Disney | DIS | Communications | $4,551.30 |

| Home Depot | HD | Cons. Discret. | $8.953.50 |

| Microsoft | MSFT | Inf. Technology | $14,040.95 |

| Starbucks | SBUX | Cons. Discret. | $8,886.75 |

| Texas Instruments | TXN | Inf. Technology | $8,784.00 |

| Visa | V | Inf. Technology | $11,188.50 |

| Cash | $351.34 | ||

| Total | $87,026.71 |

The US total value account shows a variation of $2,058.33 (-2.31%) since the last income report on February 2nd. The remaining companies in my portfolio reported their earnings in February.

Activision Blizzard is doing well in the meantime.

While the deal with Microsoft is creating more drama with regulators worldwide, Activision Blizzard announced a solid quarter. Revenue was up 43% and EPS surged by 50%, beating analysts’ expectations. It reported bookings of $3.57B, up from $2.49B in the fourth quarter of 2021. For videogame publishers such as ATVI, order bookings are seen as a key measure of a company’s business health. The latest version of the company’s bellwether title, Call of Duty: Modern Warfare II, was one of ATVI’s highlights of the quarter, as the company said the game had “the highest-opening sell-through” in the history of the franchise.

Disney to pay a dividend again!

Bob Iger is back, and it shows! The company will undergo many changes in 2023, including a restructuring plan. The company expects to lay off 7,000 employees and save up to $5.5B through its cost-saving plan. The company will also divide its business activities into three segments: Disney Entertainment, led by Alan Bergman and Dana Walden; ESPN, still led by Jimmy Pitaro; and Disney Parks, Experiences and Products, still led by Josh D ‘Amaro. With ESPN split off from the former Disney Media, Entertainment and Distribution, it will encapsulate ESPN Networks, ESPN+ and ESPN International. There are rumors about the possible sale or spin-off of ESPN, but it’s “not in the plan” for now.

Home Depot builds dividends.

Home Depot reported a mixed quarter as revenue remained flat, but EPS was up 3% and slightly beat analysts’ expectations. However, management also announced a dividend increase of 10%! The market was, however, disappointed by the lack of growth in their 2023 guidance. The company expects sales growth and comparable sales growth to be approximately flat with an operating margin of 14%, reflecting higher costs and EPS to decline to mid-single-digit levels. The operating margin will be affected by HD’s plan to spend $1B more in annualized compensation for frontline, hourly associates. We think it’s a smart move to focus on their employees during challenging times.

Find below the most complete earnings review for this quarter so far:

Earnings Season Review: Best Opportunities and Worst News [Podcast]

My Entire Portfolio Updated for Q4 2022

Each quarter we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our special additional service, DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF showing all the information about all my holdings. Results have been updated as of January 2nd, 2023.

Download my portfolio Q4 2022 report.

Dividend Income: $399.97 CAD (+39.28% vs February 2022)

I received more in dividends this month vs. last year. In the last 12 months, I added more shares of one of my favorite companies, National Bank, explaining why its dividend is up 69%. I also enjoyed several dividend increases from Royal Bank (+10%), Starbucks (+8.2%), Texas Instruments (+7.8%), and a small one from Apple (+4.55%).

The currency exchange rate is also quite different (1.27 last year vs 1.36 this year!).

Here are the detail of my dividend payments.

Dividend growth (over the past 12 months):

- National Bank: +69% (added more shares)

- Royal Bank: +10%

- Texas Instruments: +7.8%

- Apple: +4.55%

- Starbucks: +8.16%

- Granite: new

- Currency factor: +8.50%

Canadian Holding payouts: $230.71 CAD.

- National Bank: $117.37

- Granite: $34.14

- Royal Bank: $79.20

U.S. Holding payouts: $124.30 USD.

- Texas Instruments: $62.00

- Apple: $17.25

- Starbucks: $45.05

Total payouts: $399.97 CAD.

*I used a USD/CAD conversion rate of 1.3617

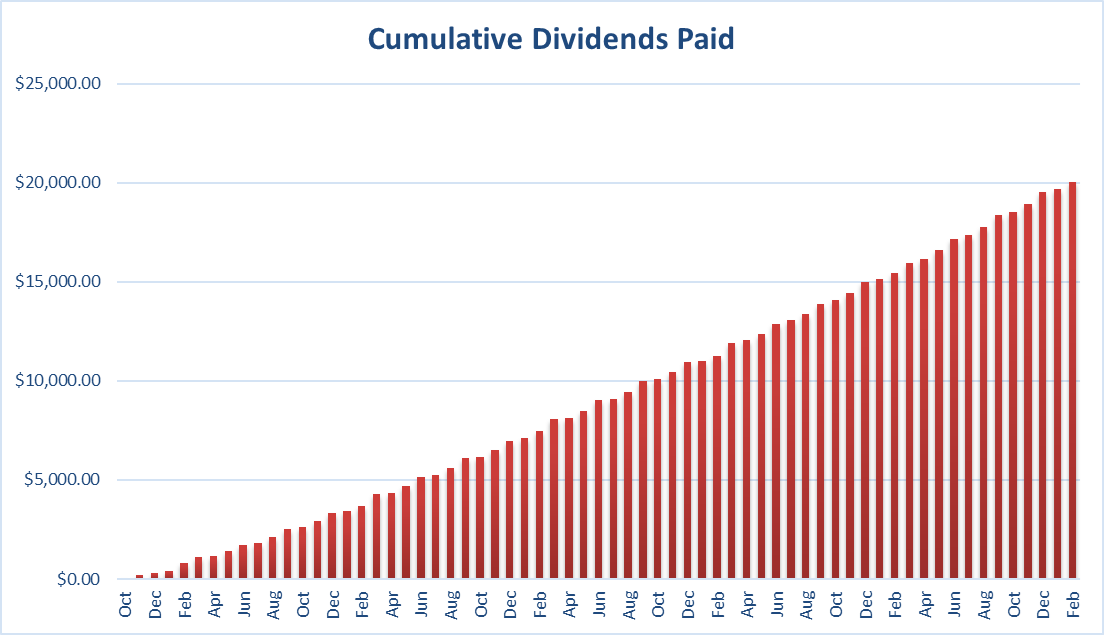

Since I started this portfolio in September 2017, I have received a total of $20,056.12 CAD in dividends. Remember that this is a “pure dividend growth portfolio,” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth comes from the stocks and not from any additional capital added to the account.

Final Thoughts

I’m glad to start investing more money in my Smith Manoeuvre as I feel 2023 will be a great year to add quality companies at a good price. As you know, I’m not a fan of stock valuation and following prices. However, when the market goes sideways (and in some cases, stocks are going down), it feels good to add dividend growers!

I’ll keep an eye on each of my holdings to ensure all the companies manage their businesses effectively through this challenging time.

Cheers,

Mike.

The post Spring Clean-Up and Smith Manoeuvre is Back! – February Dividend Income Report appeared first on The Dividend Guy Blog.