Back in April 2015 I made a bold move in my portfolio; I sold ScotiaBank (BNS.TO) to buy SNC Lavalin (SNC.TO). Many readers weren’t too sure about this move, but I’ve proven that I was right 2 years after the trade:

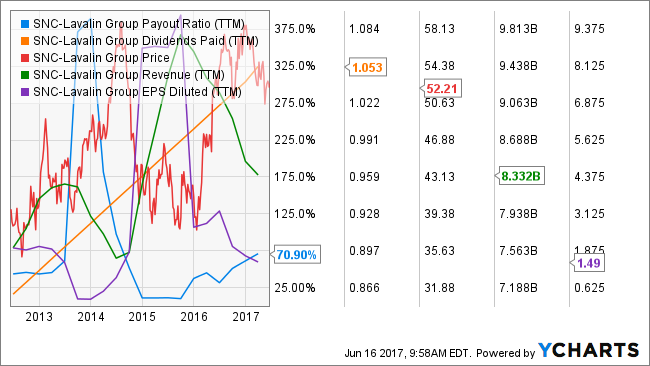

Source: Ycharts

While SNC outperformed BNS all the way, it is clear on this graph I should have sold SNC a year ago and a few weeks ago. But the investment thesis behind my purchase was still valid a year ago:

“I believe the moment charges will be settled, investors will look at the SNC $12B order book and forget about the past. After all, even with the current shadow over its head, the company continues to win contracts around the world. Their expertise is among the most solid in the world in their field. The problem came from greedy management looking to cut corners. This must be punished, but there are solid engineers working at SNC and the company should survive this storm.”

The RCMP legal pursuits threats are fading away and the company has nicely recover. However, I’m selling SNC for two reasons:

#1 The macro economic context has changed

The oil recovery is nowhere close to happening and SNC has important participation in this industry. The company shows an additional risk in the event of any market correction. I know SNC is not solid enough to convince investors during a market crash. Therefore, my chances of losing most of my profit are obvious. After all, my goal with SNC was to hold it for a short period of time and realise an interesting profit. With over 35% total return on the trade in 2 years, I think this goal has been achieved.

#2 I found a better investment

It has been harder than usual to get excited with buying opportunities lately. The market is highly priced and most great companies are following the parade. The easy money is off the table.

A few months ago, I spent lots of time analyzing the retail industry. This analysis incited me to sell Walmart (WMT) in November 2016. The main reason why I sold WMT is I believed they will not be able to compete against Amazon (AMZN) and other retail techno. On June 16th 2017, AMZN just announced the acquisition of Whole Food (WFM) for $13.7 billion. Here’s the immediate reaction on the stock market on that day of opening:

So here is my theory… AMZN, through many different ways is trying to get customers to order food online. Bezos made that clear a few years ago and now it becomes one of AMZN main focus with this recent purchase. The starting point is stuff like cereals and other easy shipped products. Those products are usually held by all brick & mortar grocery stores with tiny margins already. Imagine now that AMZN can sell them for even less?

Amazon business model is about acquiring loyal clients that will make AMZN their main purchase point for most of their day to day purchase. This is happening in various retail line and now AMZN is aiming at selling good and fresh food to their customers. I must admit that I’m already seduced by the idea of sending my grocery order online and have it picked up at my doorstep if it contains mostly bio and organic stuff… at a more than reasonable price.

Why buying a non-paying dividend stock?

The main reason why I waited to long to buy AMZN was that the company is very far away from paying a dividend. The techno is focused on growing its business at a rapid pace and will not reward shareholders through dividend payment any time soon. However, after a long time thinking about this industry, I believe AMZN represent the future of retail and will eventually pay a solid dividend. This will most likely happen in 10 years from now, but in the meantime, I’m convinced my share price will rise a lot faster than WMT, TGT and COST!

I’m not going to make an habit of looking at non-dividend paying stocks. In fact, I will not buy any others. But I think Amazon deserves to be the exception in my investing strategy, don’t you think?