Should I sell now?

That is probably the most difficult question to answer, right? Would you sell now? What would you sell? How would you do it? Which holdings should you keep? Your winners or your losers? I bought this blog back in 2010 and have written over 850 articles since then. Most of them are about my buy strategy. But one thing that keeps coming back when I ask my readers about their #1 investing struggle is the total opposite:

“I’ve never made any money from this listing and I’m in the negative almost $10K. If I cut my losses, I can’t get a tax break. Do I hang in there or cut my losses now?”

“What do you do with winners? If you still like the company? Let them ride? Trim and redeploy to diversify?”

“#1 investing struggle is that a big correction is in the horizon, but do I sell my holdings?”

I’ve covered the selling part a few times on this blog. I’ve shared some of my strategies and told you how it went for me. One of my most recent articles was about dividend cutters and the reason a dividend cut was an automatic sell for me. While those kinds of articles are great for guidelines and general strategies, I realized they had one flaw; they were missing something. We need a strong driver to pull the trigger and sell. As investors, we usually understand why we should or shouldn’t sell a stock. But doing it is a completely different thing. In this article, I’ll explain the three reasons why I sell and, most importantly, the emotional and rational driver behind the decision through real-life examples. But first, let me share a little bit more about my story.

Going back in 2003

I’ve once had these questions coming into my mind when I started investing. My first step into the jungle was at the age of 22, back in 2003 when money was easy to make. Back then, I was mostly buying and selling stocks on a hunch. I was making lots of trades and spent lots of time watching the market. I thought I was playing at the big table (with pennies in hands). I made more good moves than bad ones, but that wasn’t investing.

I made a hefty profit and bought a house with it. This transaction probably saved my “investing career” as I was comfortably looking at the 2008 crash with very little in my investment account (about $30K or $40K from what I can remember).

I didn’t know when or what to sell back then. I was just cashing profits here and there and jumping from one stock to another like a kid in a playground. Watching my portfolio going into smoke (I ended 2008 at -27% for a 100% equity portfolio, not too bad, but still!), I realized I need a real investing structure. 4 years of research and personal experience led to my 7 dividend investing growth principles. Principle #6 reads as follow: The Rationale Used to Buy is Also Used to Sell.

But Why it is so hard to sell stocks?

I realize the irony in using the word “rationale” in my principle nomenclature. After all, investors have often more emotions behind a trade than anything else. Even when I try to act rationale, my emotions create bias that let me think I’m in control of my emotions. This is why it is so hard to sell stocks you first bought. Each time I sell shares, I must admit to myself a cold hard truth:

I sell, therefore I’ve failed as an investor

You don’t sell your losers, because you think you will be eventually right and they will come back.

You don’t sell your winners, because you can show that you were right and you surf on past paper profit.

And let’s admit it, the fear of selling and then looking at the stock going up a few months later to prove you wrong (a second time) is always in the back of your mind. Being wrong once is already hard; being wrong twice is just pure torture for the investor’s mind. As long as you hold onto your shares, you can always tell yourself it’s only paper loss and you can make it back later. LIE.

Stop Lying to yourself, It’s your money after all!

After struggling to sell my stocks for several years, I’ve concluded I must find ways to trigger those transactions without second guessing. It was time for me to find ways to protect my money against myself. Some do it through the help of an advisor (as he should do the hard job to make sure you keep him!), I decided to do it myself. Chances are you are in the same boat if you are reading this article, right?

Working in the financial industry as a financial planner and then a private broker for over a decade taught me something very important: plans work as long as you follow them. I know, lots of people will come out with catchy lines such as “plans work until they don’t”, but that’s just an excuse for those who fail an can’t take accountability. If you have a solid plan and it keeps evolving according to your situation, it will continue to work. This is how great companies like Disney (DIS) and 3M (MMM) continue to find new ways to thrive 90+ years after they were created.

They follow the plan.

They make sure the plan evolves.

They stick to the plan.

We should be ruthless toward companies we invest in. After all, they are the lucky winners across thousands of potential investments. If you decide to invest your money in a few dozens of businesses, they should reward you, worship you, not the other way around. Here’s how I design my 3 sell triggers for all stocks. They are not perfect, sometimes I sell and I shouldn’t have, but overall, they get the job done and help make sure I reach my investing goals.

Now, more than ever, is time to clean your portfolio and sell some stocks

Why should you do it NOW? Because the market has well recovered from the latest drop, optimism is back in business, and you can probably get rid of some losers at a very good price. If we hit a real bear market, then it will be too late and you will get suffer from paralysis by analysis once more. I recently asked you how your beach money was. We just came back from a long holiday season of 10 years of a bull market, it’s time to cut off some fat.

Instead of looking at what you should do with your company, let me translate my 3 sell triggers into real-life examples that I’m sure you would not accept. Therefore, you shouldn’t accept those situations in your portfolio either.

You fail to pay me, you’re out!

Imagine a moment that you are the proud owner of a 20-plex rental property with carefully handpicked tenants. You have spent many years to make sure your property was well in order and that each year your tenants would pay a higher rent. This is the work of a lifetime and this money ensures a comfortable retirement.

On the first of the month, you knock on each door to collect your due. This month, 3 tenants offer you to pay $500 instead of the $900 they owe you. They tell you they face unexpected challenges in their life and that by cutting down their rent payment it will give them additional financial flexibility and things will get better later on. By keeping those three tenants, you now lose $1,200 per month in rent and your rental property loses value too as it generates a lesser income. Do you keep those tenants?

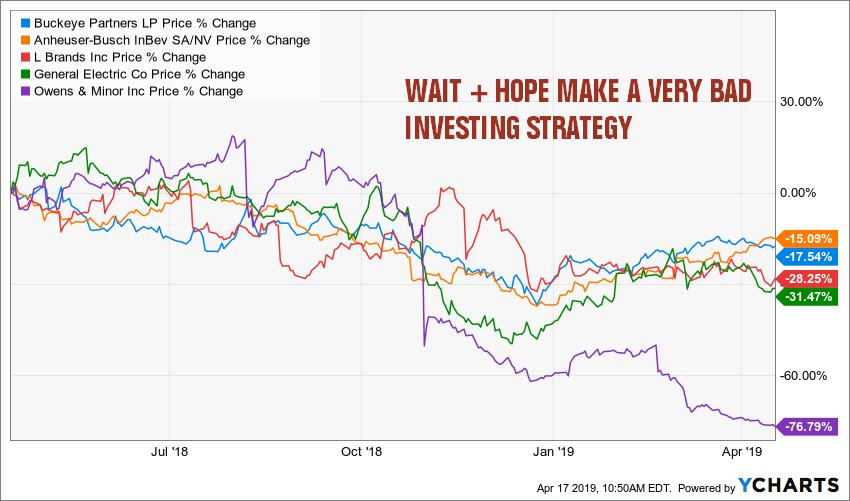

Each time a company cuts its dividend, I just get rid of that bad tenant and replace it with another. Companies like General Electric (GE), Owen & Minors (OMI), Buckeye Partners (BPL), L Brands (LB), Anheuser-Busch InBev (BUD) all cut their dividend in 2018. How many years will you have to wait to recover both your dividend and share price loss if you hold on to them?

Source: Ycharts

While you may think that -15% isn’t too bad for BUD, just think that the S&P 500 rose by nearly 9% (+8.57% as of April 17th) during the same period. Therefore, even the “best of the dividend cutters” underperformed the market by 23.5%… Enough said.

Keeping dividend cutters in your portfolio not only effects your current portfolio value, but also your ability to generate future income from it. In some occasions, you may wait and get your money back, but think about the time you must wait and the opportunity cost. After you suffer the dividend cut, it’s already too late; you were wrong and it’s time to admit it. It hurts, but you better treat the wound now and not wait until it infects your entire portfolio.

Would you work for the same salary for the next 10 years?

Now imagine that you are very good at your day job (nah… don’t imagine that, I know you are!). You have lots of experience and you can easily get another job elsewhere with great conditions. In fact, you even receive offers from head hunters from time to time. But you are comfortable where you are at and enjoy your routine. You kind of “fell in love” with the place. Tell me how much you would still be in love if your boss tells you that you will not have a pay raise for the next 5, maybe 10 years?

You work hard, you would get a raise anywhere else on the market and you can do the move whenever you want. Do you keep that job with no pay raise? Of course you wouldn’t!

The whole point you work all your life and make sacrifices to save money is to have your money work for you at retirement. You want to substitute your job by a passive income coming from your portfolio. How will a company not raising its dividend help you reaching this objective? Keep in mind that an absence of dividend growth is also the first step before a dividend cut. This is one of the three red flags I’ve identified to trigger a sell (you read about other red flags here).

For this reason, I put any of my stocks in the “sell bin” after 2 years without a dividend increase. I don’t automatically sell them after this period, but I go through the business model and their financial statements to make sure my dividend is safe. Then, I assess the possibility of seeing a dividend increase in the next 12 months. There are so many great companies raising their payouts each year, why should I bother keeping companies that can’t do that?

To what extent can you love someone?

You’ve been with your spouse for over 10 years. You had some difficult years, but overall, it has been a great love story. You have founded a family, you are happy, you can see how your love grew overtime. But in the past few years, your spouse isn’t the same anymore. You don’t have the same taste for food, not doing the same activities, and barely talk to each other. When you do, it’s because you enter into an argument. You are not happy anymore and your spouse would obviously agree on that single point. You went through couple therapy and it didn’t work. What was magical 10 years ago is not there anymore. Do you keep-up with a broken relationship just because it was great a long time ago? This sounds like a miserable way to end your days, isn’t it?

You guessed it. This sell trigger is about your winners. When do you sell a winner? When it reaches 50% profit? 100% more? Less? None of the above.

As is the case with personal relationships, when it’s not what it is used to be (read it’s gone sour), it’s time to move on. This May, I’ll celebrate 22 years with my wife (15 being married). The reason why I’m still in love today, is because we have evolved together and we can still find the magic between us.

When you open a position in your portfolio for a stock, you are opening the “heart” of your wallet. This is usually because you see something special about this company. In more conventional terms, we say that you have “an investment thesis.” Each quarter, I revise my investment thesis (but not with my wife, haha!). If a company doesn’t show the reason why I bought it in the first place, then I truly consider selling my shares.

Sell now, upgrade your portfolio and enjoy the ride

I’ve discussed many times on this blog that predicting the market is useless. Some investors are lucky enough to get it right once or twice, but most of us will get it wrong 9 times out of 10. Unless… unless you keep your money invested in strong dividend growth companies.

I believe taking care of my portfolio is like taking care of my body. It requires simple actions that are difficult to maintain over the long run. I’ve recently discussed some basic principles to get your portfolio in shape in “How’s Your Beach Money?” I wanted to go a little bit deeper with another article and describe a step by step methodology I use to make sure my portfolio is always in top shape. If you don’t know where to start to sell your stocks, I’d suggest you start with this article:

Portfolio Fitness:Tricks to Train Your Money To Work Harder

Enjoy!

The post Sell Now – It’s About Time Someone Tell You This appeared first on The Dividend Guy Blog.