We are already in February and if you have been too busy with your 2017 resolutions, you may have forgotten the RRSP season is about to end soon. February is the last month you can contribute to your Registered Retirement Savings Plan. This Canadian program has been created to help you build your retirement nest egg. You would be a fool not to take advantage of it.

I’ll start this article with a quick refresh of RRSP basics and then, I’ll share with you my favorite RRSP strategies.

What is a RRSP and why do we have a season for it?

An RRSP is a Canadian-only retirement investing account allowing you to invest money in a tax-sheltered account. This means that as long as your money is in your RRSP account, you will not be taxed on your profits nor revenues (capital gain, interest or dividend) generated in your account. There is more to it; each time you add more money to your RRSP account, this amount is also tax deductible. Therefore, you are paying less income tax when you contribute to your RRSP. On the other hand, each time you withdraw money from your RRSP account, this amount is being added to your revenue and becomes taxable. In other words, you are better off contributing to your RRSP when your tax bracket is high and withdrawing money when your tax bracket is low.

The interesting point with RRSPs is that you can invest in just about any kind of product. Think of your RRSP as a box protecting you from the Government collecting taxes from it. You can put anything you want in that box (stocks, etfs, bonds, mutual funds, Canadian or foreign investments, GICs… but don’t put GICs in there! hahaha!).

The reason why there is an “RRSP Season” is because it’s like the Holiday Season… for financial advisors! As most people are last minute when it comes down to their personal finances, investing money for their retirement is usually the last thing on their to do list. As Canadians have up to the end of April to file their taxes, the Government also gives them up to March 1st of the following year to contribute to their RRSP and use their contribution for a deduction in their tax report. For example, you have until March 1st 2017 to contribute to your RRSP and use this contribution to get a tax deduction on your taxes for 2016. If you contribute to your RRSP on March 2nd, the tax deduction can only be applied to 2017 and forward.

Here are a few important things to remember for this year:

RRSP 2016 Contribution Deadline: March 1st

RRSP 2016 maximum amount contribution: 18% of your declared income up to $25,370

Amount you need to reimburse on your HBP (Home Buyer Plan): the first 2 years after you withdraw are “free of reimbursement”. Then it’s 1/15 per year of the amount withdrawn.

Contribution Double Dip

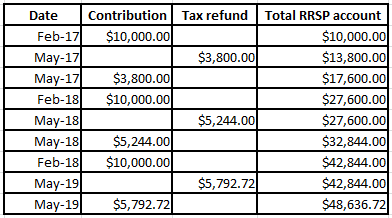

One of my favorite RRSP strategies is what I call the “double dip” strategy. Here’s how it works. This year, you invest $10,000 in your RRSP. Assuming you have a marginal tax rate of 38%, you will receive a nice cheque from the Government of $3,800 (your tax refund). By investing this very same amount to your RRSP account (again), you will receive another tax deduction the next year of $1,444.

Within the span of 12 months, you will have invested $13,800 in your RRSP and you would still have $1,444 in hand to do something else with it. If you are good enough to “triple dip” your contribution and add the $1,444 to your RRSP account, you will receive another cheque of $548 the following year. Here’s a table to show you the power of the double (or triple) dip strategy:

As you see, by contributing $10,000 per year and using your additional tax return to contribute again, you generate a total investment in your RRSP account of $48,363.72 while you only used $30,000 of your own money. Your total tax return for this period is not based on your tax bracket of 38% but rather 61.21%. And we are saying the Government only steals from our pockets?

Invest your RRSP contribution in U.S. Dividend Stocks

My second favorite RRSP strategy is even more simple than the first one: invest in U.S. dividend paying stocks. Why is that? Because the RRSP account is the only account offering a 100% tax shelter against U.S. dividend payments. There is a form to diminish the tax impact of a dividend paid in a TFSA (Tax Free Savings Account), but you will still end-up paying 15% taxes on it. The RRSP account is the only one offering you the possibility to invest in U.S. stocks and not pay any taxes.

Also, you have the possibility to invest your money in USD and never suffer from the currency exchange fees brokers charge to convert your USD dividend into CAD.

Questrade is offering the lowest transaction cost brokerage services and do offer a USD RRSP account.

RRSP or TFSA? Think RESP!

This is a question that comes back from time to time as the difference between both types of accounts is minimal. First, the RRSP gives you a tax deduction but your withdrawals will be taxed. When you invest in a TFSA account, you don’t get the tax deduction, but you are not taxed on your withdrawals in the future. The TFSA is also more flexible as you have the opportunity (not the obligation) to reinvest money that was withdrawn from your account at any time. Both accounts are tax-sheltered for all kind of investments. However, U.S. dividend payments are taxed at 30% in the TFSA (and then you can file a form to reduce it to 15%). I’ve ran multiple calculations and in the end, unless your tax brackets remain high when you retire (meaning you have a defined benefit pension plan or other type of taxable revenues), there isn’t much difference between contributing to the RRSP or the TFSA on the long run. I would still give a slight advantage to the TFSA for its flexibility and the fact that we don’t know what our future tax bracket will be when we retire.

However, there is another solution if you have kids and it is called the RESP (Registered Education Saving Plan). Believe it or not, the RESP is an even better investment for your buck than both the RRSP and the TFSA. The RESP entitles you to a tax-sheltered investment account and the Government gives 30% up to $2,500 in contribution subsidies per year. The best of all? At the time of withdrawals, only the subsidies and the profit generated in the account are subject to taxes as your contributions are tax free. Even better, the subsidies and profits will be taxed in the hand of your child… which would lead to a near 0% tax rate. All your kid needs to do is register for a post-secondary education… which is pretty flexible.

So, if you have kids, consider boosting your RESP contributions first.

RRSP Loan? Nah!

I will finish this quick refresh article with the famous RRSP loan that is sold widely across the financial advisor community. Why do they sell it? Because they get more money in their pockets faster. Think about it, what is better for the financial advisor:

- Selling you a $15,000 loan with a $15,000 RRSP contribution ($30,000 of immediate and commissionable business)

- Setting an systematic investment plan of $300/month (approximately what the $15K loan would cost you over 5 years) for a total of $3,600 of immediate and commissionable business

When you look at the calculation, your financial advisor may receive about 9 times the commission if he opts for plan A)… Can you really blame him?

However, if you decide to put the $300 per month in your RRSPs you will invest the sum of $18,000 over the next five years as opposed to the $15,000 offered through the RRSP loan. It is true that you will lack from the power of compounding interest as the first year, you will have $3,600 working for you instead of $15,000. However, assuming an 8% return rate (which is pretty strong), you would end-up with $22,039 with the loan option and $22,043 with the systematic investment plan. The best part? You will have created a very strong habit of savings instead of paying down a debt!