Subscribe: Spotify, Apple Podcasts, Google Podcasts

In the last episode of this series, we’ll elaborate a simple, but effective, plan to make sure you always have enough money to enjoy your retirement.

How to withdraw money? Which stocks to sell? How many transactions per year? When should you wait before withdrawing?

On Thursday, May 20th, I’ll be hosting a free webinar on how to optimize your portfolio for retirement and withdraw money from it.

Click here now to register to the webinar

(Over 13,000 investors saw my webinars, make sure to secure your spot!)

After this webinar, you should be able to:

- Protect your capital at retirement

- Improve portfolio yield without increasing risk

- Create a safe a reliable income from your portfolio

Here are the complete details:

- The webinar is on Thursday, May 20th at 1pm ET.

- It is 100% free, no strings attached.

- The presentation is about 50 minutes.

- I’ll stay for one hour to answer all your questions.

- I’ll provide the handouts to all live attendees.

- There will be a free replay link sent to all registered attendees.

Register now and watch the webinar at your convenience.

Prepare your questions. This webinar is about 50 minutes long, and I will answer all your questions about stocks, strategies and the economy afterward.

You’ll Learn

- How to withdraw money without outliving your portfolio.

- How to prevent suffering from market events.

- When necessary, which stocks should you sell?

- How many transactions per year to do.

- Are bonds or fixed-income products good options for retirees?

- Summary in 3-step on how to optimize your portfolio before retiring.

Related Content

Here are a few points to consider when you look at fixed-income products.

Understand the Strategy

Many companies will use a mix of options strategies to create income. Therefore, it’s crucial to understand in what you are investing. This will require you to read several pages of boring stuff. If you take the Financial Split (FTN.TO), you can’t stop at the company’s fund description: “…is a high quality portfolio consisting of 15 financial companies made up of Canadian and U.S. issuers”. Considering a 13.5% yield, this sounds promising, right? Now let’s read a little bit further on page 6 and 7 of their 2021 annual information form:

“Up to 15% of the net asset value of the Company may be invested in equity securities of issuers other than the Portfolio Companies.”

And, also: “To supplement the dividends earned on the Portfolio and to reduce risk, the Company will from time to time write covered call options in respect of all or part of the Portfolio.”

And finally; “The Company may also write cash covered put options or purchase call options with the effect of closing out existing call options written by the Company and may also purchase put options in order to protect the Company from declines in the market prices of the securities in the Portfolio. The Company may enter trades to close out positions in such permitted derivatives. The Company may also use derivatives for hedging purposes or otherwise as permitted under National Instrument 81-102 Investment Funds (“NI 81-102”).”

Long story short, after you know that 15% of your money is invested in equities, and the rest is up to “option strategists” to work their magic. How did that dividend work for investors? The same monthly distribution of $0.1257/unit since 2008. Not bad? Oh! I also forgot to mention that FTN skipped 33 monthly payments between September 2008 and March 2021 (source). If you count on the monthly distribution to pay for dining out, you put yourself on a severe diet.

This specific product return will be linked to the results of a complex (and ongoing) options strategy. It may or may not work in the future. What we see is that the product works well when the market is up but finds itself in a difficult position when things get volatile. Based on my personal observations and a general feeling that is not backed by a study or a scientific approach, these are not products your hard-earned savings should be exposed to at all. However, also please note that the fund skipped payments in 2009, 2011, 2012 (18 months in a row), and 2020.

Understand the benchmark (are you leaving money on the table?)

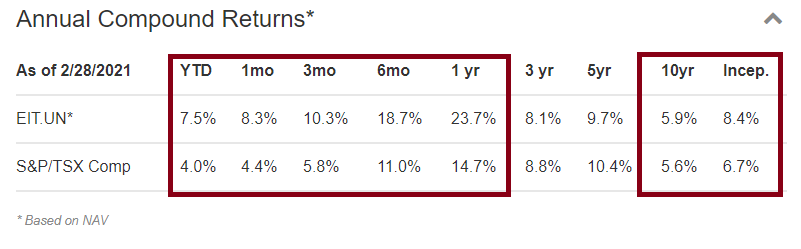

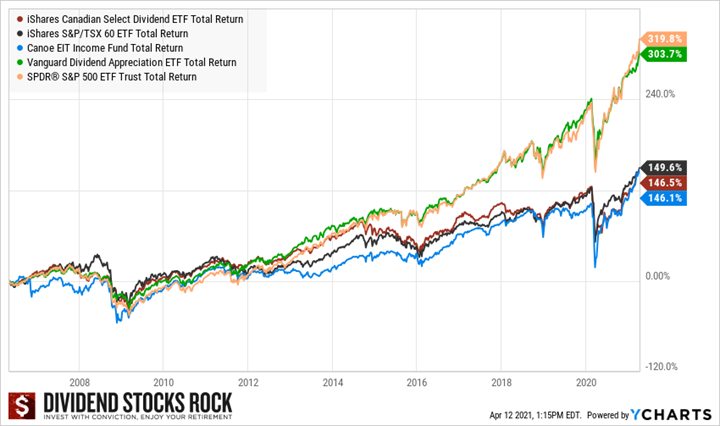

While I understand the focus is on income during retirement, let’s not forget about total returns. Imagine if I were to tell you that you could invest in the new High Income DSR fund? The HI-DSR fund would require a minimum investment of 100K and we will start with a distribution yield of 8%. Over time, you realize that while you get your 8% yield, your 100K isn’t keeping up in value. Your total return (capital gain + dividend) is still positive, but you don’t make that much money if you compared to a classic index ETF. How would you react? In my opinion, the money you receive monthly is as important as the value of your portfolio. Therefore, considering total return must not be forgotten. Then, you also must compare apples with apples. Let’s take Canoe EIT income fund (EIT.UN.TO) returns for example:

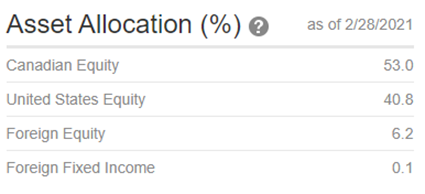

As you can see, I’ve highlighted that for most periods, Canoe beat the TSX index. Considering that EIT offers a yield over 10% and beat its benchmark, this looks like the perfect pick for any retiree, right? Think again! If you look at the EIT fund profile, you will notice that it enjoys a well diversified portfolio including 41% of its money invested in U.S. equities:

If you consider all investing options (index investing, dividend ETFs, high yield products and DSR portfolios), you notice how much you have left on the table in the name of income stability.

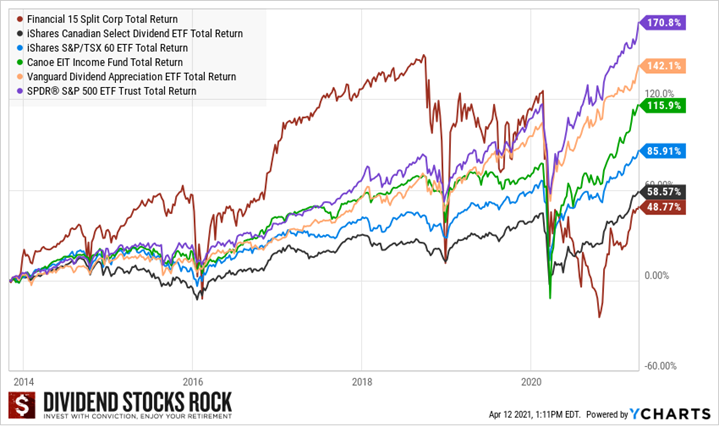

Between October 31st 2013 and April 12th, the 100K DSR CAD portfolio (50% CAD, 50% USD) generated at total return of 128.90% (vs 128.30% for SPY and XIU.TO average) and the 100K DSR US portfolio (100% USD) generate a total return of 186.93% (vs 170.8% for the SPY). EIT shows an honest performance at 115.9%, but the Financial Split 15 is way behind at 48.77%. If you consider EIT since 2006 to include both 2008 and 2020 crisis, the fund is right on target with the Canadian market, but so far from the SP 500:

Overall, not all high-income products are terrible. In fact, Canoe isn’t that bad of a product when you look at its overall performance. Nonetheless, the price to get an income product in your portfolio is very steep when you consider how much you could have made through dividend growth investing or index investing. Next time you look at a high-income product, consider the real price to pay!

The post Retirement Portfolio Series – Withdrawal Mechanics to Enjoy Retirement [Podcast] appeared first on The Dividend Guy Blog.