Subscribe: Spotify, Apple Podcasts, Google Podcasts

Should you live on your dividend payments alone at retirement? Or should you sell some shares? What if you do a bit of both? Learn the pros and cons of both options and see how you can create your income at retirement.

You can listen to the introduction of this series here.

On Thursday, May 20th, I’ll be hosting a free webinar on how to optimize your portfolio for retirement and withdraw money from it.

Click here now to register to the webinar

(Over 13,000 investors saw my webinars, make sure to secure your spot!)

After this webinar, you should be able to:

- Protect your capital at retirement

- Improve portfolio yield without increasing risk

- Create a safe a reliable income from your portfolio

Here are the complete details:

- The webinar is on Thursday, May 20th at 1pm ET.

- It is 100% free, no strings attached.

- The presentation is about 50 minutes.

- I’ll stay for one hour to answer all your questions.

- I’ll provide the handouts to all live attendees.

- There will be a free replay link sent to all registered attendees.

Register now and watch the webinar at your convenience.

Prepare your questions. This webinar is about 50 minutes long, and I will answer all your questions about stocks, strategies and the economy afterward.

You’ll Learn

- What does it mean to create a “safe” income.

- What is the dividend option for retirees.

- The pros and cons of living from dividend payments alone.

- How you can create your own dividend using total returns.

- The pros and cons of selling shares at retirement.

- Why dividend growth is still important when you retire.

Related Content

Here are a few more words about the “Create you Own Dividend Option” discussed in the episode. It will surely help you put images on the concept.

I had a great conversation with a DSR member recently. She was comparing Canadian Utilities (CU.TO) and Alimentation Couche-Tard (ATD.B.TO) from a retirement perspective. She was trying to determine which stock would be a better fit to generate income.

On one side, you have a utility with limited growth potential, but an impressive dividend growth history (49 years!). With a yield of 5%, it looks like a no brainer. I agree.

On the other side, you have a growth-oriented company with an impressive dividend growth rate (24% CAGR over the past 5 years), but with a mediocre yield (0.80%).

How much time it will take Couche-Tard (0.80% yield) to reach Canadian Utilities’ yield? Short answer: forever.

Verdict? Pick Canadian Utilities and ignore Couche-Tard!

Not So Fast.

Let me remind you of the concept of total returns ?. As I mentioned earlier, dividends aren’t guaranteed and let alone magical. Couche-Tard offers a low yield because the company is heavily focused on growth. It pays a small yield but uses most of its money to grow the business and create added value for shareholders.

Finance 101: if a company finds opportunities to generate value for shareholders, it must use its cash flow. If it can’t, then the dividend appears to allow shareholders to allocate capital in a more optimal way.

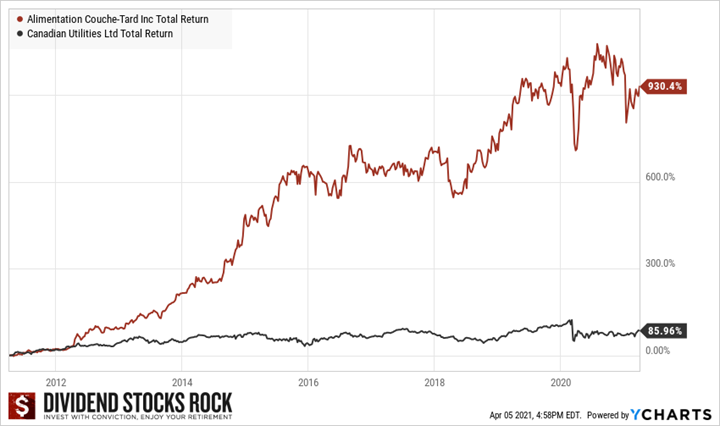

Now, instead of wondering how much time Couche-Tard will take before it generates an interesting revenue coming from its dividend alone, you should wonder how Couche-Tard’s stock price could rise faster than Canadian Utilities. The answer? Quite shocking if you look at the past 10 years.

That’s right, over the past 10 years, ATD surged by almost 1,000% while Canadian Utilities didn’t even hit 100%. If I had invested 100K in ATD in 2011, I would have nearly $1M to fund my retirement today. With CU? Less than 200K. Which amount will generate the most income? At this point, it’s a rhetorical question.

The solution is not to invest in all the Couche-Tard’s of this world and ignore the Canadian Utilities. If you are retired, you want some “sure shots” like CU in your portfolio. This type of company brings stability and a decent expectation you will generate good income year after year.

I used this extreme example because I wasn’t cherry-picking as it originated from a real-life example from a member. Also, it shows that a balance between low yield, high growth stocks and classic “retirement stocks” such as utilities and REITs could create the perfect blended retirement portfolio.

Dividends aren’t magical. Therefore, instead of getting a high yield from Couche-Tard, you get high growth. Once retired, you can easily take your “one-million-dollar investment” and generate your own dividend by selling a few shares on occasion.

Remember this: the value is either in the dividend or it’s the share value. It’s the exact same thing. If you focus on building a portfolio filled with amazing dividend growers, you won’t have to worry about your average dividend yield.

The post Retirement Portfolio Series – Two Dividend Options to Create Your Paycheck [Podcast] appeared first on The Dividend Guy Blog.