Subscribe: Spotify, Apple Podcasts, Google Podcasts

There are zillions of books, articles, and services about building your nest egg. However, there are not close to as many resources on creating a paycheck from your portfolio. This is often a cause of doubt and anxiety for the investors about to retire.

This is the intro of a series on How to Turn Your Portfolio into a Safe Money Making Machine at retirement.

You’ll Learn

- To what extent should an investor consider tax aspects in his investment strategy.

- How to set a budget for your retirement.

- How much cash should you keep in your account when retiring.

- Two ways a dividend investor can build its cash cushion and which one is Mike’s favorite.

- How does living on dividend payments alone translate on a monthly budget.

Related Content

The “dividend option” is the most classic way to generate income from your portfolio. It makes so much sense to do one simple calculation and then to think you are done. You need $30,000? Easy! Imagine you have $800,000 invested, you divide $30K by $800K and you make sure your portfolio averages 3.75% in dividend yield.

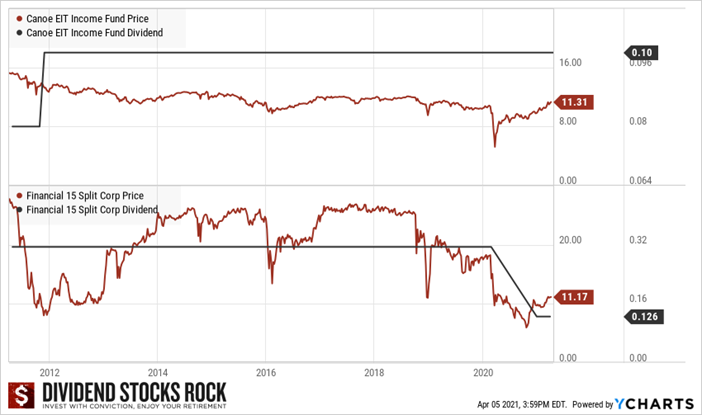

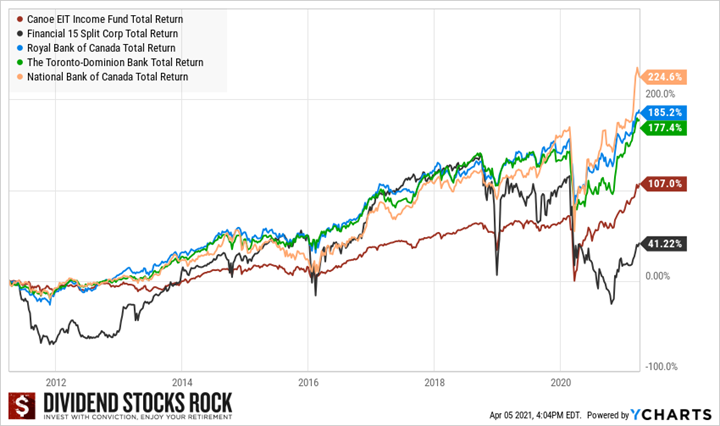

If your calculation leads to a portfolio yield of 3 to 4%, you won’t have to worry about much. In fact, you may be able to cut down your cash cushion to 1-year worth of your retirement budget and you’ll be just fine. Unfortunately, many retirees will face a situation where they need $50,000 per year while having $600,00 invested. Then, generating an 8.3% yield isn’t that easy. Sure, you might tell me that you have found some generous MLP’s or split share products generating 8%+ yield. But, when you look at their long-term returns, you may want to revise your strategy. Here’s a quick example of the Canoe Income Fund (EIT.UN.TO) and Financial 15 split Corp (FTN.TO):

The first case (Canoe) is the “most successful one”. Your dividend income is getting eaten up by inflation year after year while your asset (the stock price) is slowly, but surely going down in value. If you are unlucky and bought the Financial Split 15, then you have suffered from both a revenue loss (dividend was cut in 2020) and a loss of capital (stock price was above $20 and now struggles to stay over $11). This is not what I call a safe money printing machine.

It’s important to note that Quadravest will describe the Financial Split 15 as a “high quality portfolio consisting of 15 financial services companies made up of Canadian and U.S. issuers”. You could have saved yourself a lot of time and grief by buying your favorite top 3 Canadian banks and calling it a day.

I understand the 8% yield is easier to calculate and looks more stable. After all, if the company pays 8% each year, you don’t have many calculations to do. You cash your dividends and you move on. However, how many of those 8% yielders eventually cut their dividend and you wake up to a massive capital loss as well?

The answer? Enough of them to kill your retirement portfolio.

We will cover this topic more in depht in the next episode. Exceptionnally, we will do three small episodes in the same week, from May 17th to May 19th. If you want to get notified, please subscribe to our podcast through your favorite platform.

Spotify, Apple Podcasts, Google Podcasts

Follow Mike on:

- YouTube

The post Retirement Portfolio Series – Let’s Start With the Basics: Budget and Cash [Podcast] appeared first on The Dividend Guy Blog.