Many retirees make costly investing mistakes based on common beliefs or make bad investment decisions based on fear. I think the biggest concern retirees have regarding their portfolio is probably the fear of losing money. The emotional charge linked with managing your portfolio may lead you to make fatal investing mistakes. The feeling that comes with withdrawing money from your portfolio when you’ve spent your entire life adding to it creates big shock.

It’s impossible to have a flawless investing strategy and avoid all mistakes. Even smart and experienced investors fall into investing trap sometimes. By avoiding fatal mistakes, you will immediately improve your chances of living a comfortable and stress-free retirement. Here are the top mistakes retirees make with their money and how to avoid them.

#1 Using a rule of thumb as an investing strategy

There is an investing rule of thumb that could hurt greatly your portfolio and this is the 100 Rule. This is a simple rule to determine your asset allocation. You take the number “100” and subtract your age. This should give you the proportion of equity or “stocks” (riskier assets) in your portfolio.

For example, if you are turning 65 this year, you should only have 35% of your portfolio (100-65) in equities. In other words, the older you get, the lower your exposure to stocks should be. This sounds right when you first read it, huh?

The retirement mistake

The problem with this rule of thumb is that it came from another era where life expectancy wasn’t that high and bonds and other fixed income products were more generous. There was a time you could invest in safe bonds and earn 5-6%. This is not true anymore. On top of that, your life expectancy keeps increasing. This means you will live longer, and bonds don’t generate enough income to support your lifestyle.

If you live in North America, chances are you will need money to cover your expenses until the age of 85… read 90. If you follow the 100 Rule, you will probably outlive your portfolio.

What to do instead

Your age should not determine your asset allocation. You should rather consider your risk tolerance. There is also a balance between which kind of temporary loss you can stomach and the investing return you must achieve to finance your retirement.

For example, if you run the calculation (you can find great retirement calculators at Calulator.net) and you realize that you need to achieve a 6% portfolio return to have enough money until you turn 85-90. You won’t be able to generate a 6% annualized rate of return with a portfolio with 65-70% in bonds. Not with today’s interest rates.

Therefore, having a larger portion of your capital invested in stocks will help you reach your retirement goals. At the end of this article, I will provide you with a complete guide on how to invest at retirement.

#2 Chasing yield thinking it’s safe revenue

Another common mistake made by retirees is to chase yield when considering various investment options. Thinking you can invest your $500K at 9% and live off $45,000 in dividends sounds like the perfect plan. But chasing yield could literally obliterate your capital.

The retirement mistake

The problem with high yielding stocks or bonds lies within the sustainability of their distributions. We currently live in a world of low interest rates. Why would a company pay a 6%+ yield to its shareholders or issue bonds paying 8%? Keep in mind there is no free lunch in finance. If the yield is higher, the risks is higher too.

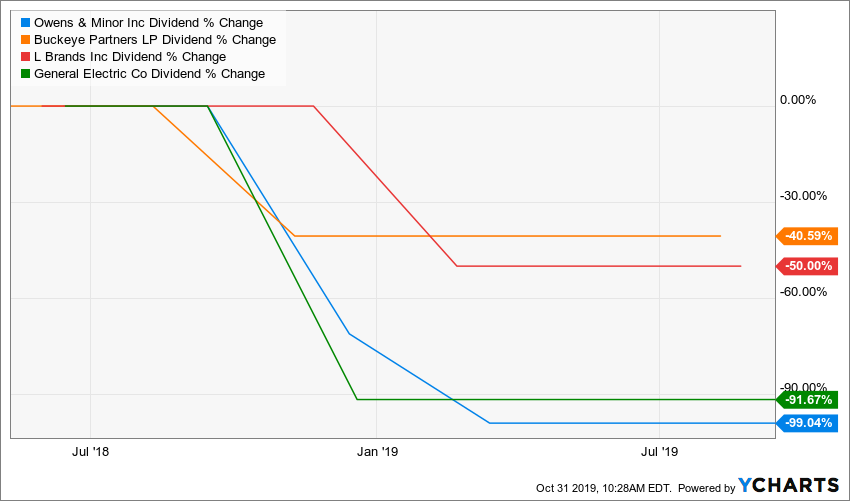

In an ideal world, we would all find those generous stocks paying high yields and live off dividend distributions without touching our capital. But in the real world, your retirement income may look like this:

Source: Ycharts

What to do instead

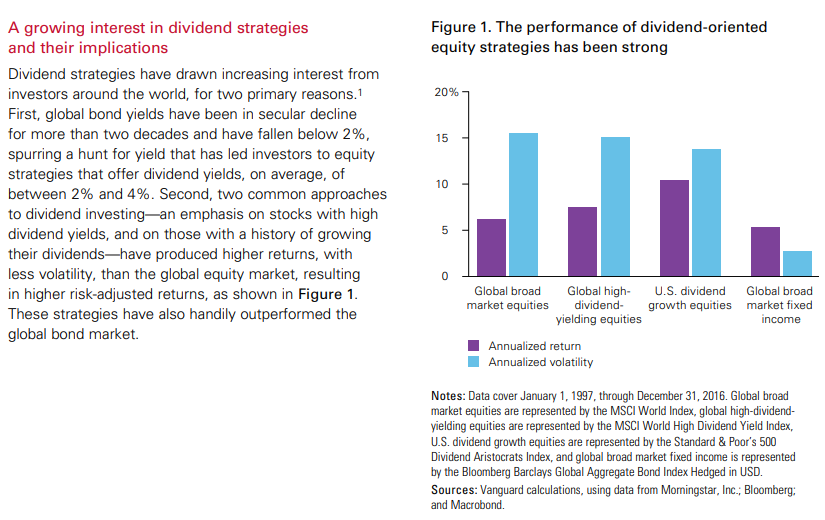

Instead of only looking at high yielding stocks, you should also consider other metrics. It is usually worth it to consider dividend growth over dividend yield. Many researchers prove that dividend growers will not only outperform the market, but will also do it with less volatility. More money, fewer fluctuations, this is what you want, right?

Source: Vanguard

During this 10-year period, dividend growth stocks not only beat the market, but they did it with less volatility.

#3 Withdrawing from your portfolio periodically

The third investing mistake is easily avoidable. At retirement, many seniors like to withdraw the same amount of money periodically. They make their budget and they simply shift from having a pay check from their employer to a “pay check” coming from their portfolio. This makes money management easy, but is also a very big mistake.

The retirement mistake

The timing of your withdrawal has a huge impact on your portfolio. Withdrawing money during a market crash accelerates the value drop. For example, withdrawing each month during 2008-2009 would have prevented you from enjoying a strong come back on the market only a few months later.

For the sake of having a monthly budget, you are making the mistake of withdrawing thousands of dollars at the worst possible time.

What to do instead

Here’s an easy one: plan ahead! If you need $48,000 a year from your portfolio, don’t withdraw $4K per month. Instead, plan before retirement to have over $48K in cash ready to be withdrawn. In an ideal world, you would have a reserve good for 18 to 24 months in cash. This would allow you to withdraw money without caring about the stock market fluctuations. When the market goes up, continue to sell some shares (or cash the dividend) to keep your cash reserve high. When the market goes through a correction, let your portfolio ride and withdraw from your reserve. Easy, right?

#4 Thinking inflation rate is below 2%

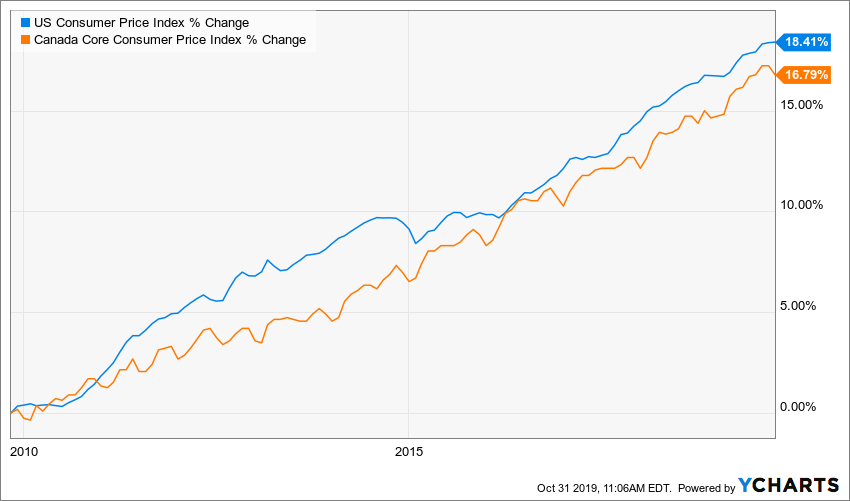

The last, but not the least fatal mistake you can do as a retiree is thinking the inflation rate is below 2%. When you look at the past 10 years, you could wrongly assume inflation in North America is below 2% on annualized rate:

Source: Ycharts

The retirement mistake

The mistake retirees make is to consider the country’s inflation and think it applies to their own budget. When a country calculates their inflation, they considering a large basket of goods. Things like electronics and automobiles will definitely bring this number down, but you won’t necessarily replace your car every 3 years once retired.

On the other hand, foods, the price of healthcare services and recreational activities will likely grow faster than the announced inflation. This is where you put your focus as it will hurt your budget over the long haul.

What inflation rate really is

Your personal inflation rate will vary depending on your budget. If you don’t want to bother calculating it, I guess a 3% inflation rate in your retirement plan would cover pretty much all scenarios. Better plan conservatively and enjoy a comfy retirement, right?

If you manage to avoid these 4 mistakes with the solutions I’ve provided, you will increase your chance of building the retirement of your dream.

The post Retirees Make These Fatal Investing Mistakes appeared first on The Dividend Guy Blog.