Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas.

With more earnings reports coming in, we have seen a few winners emerging from the buy list. Last time, we covered two growth stocks. We also found new ideas for income seeking investors.

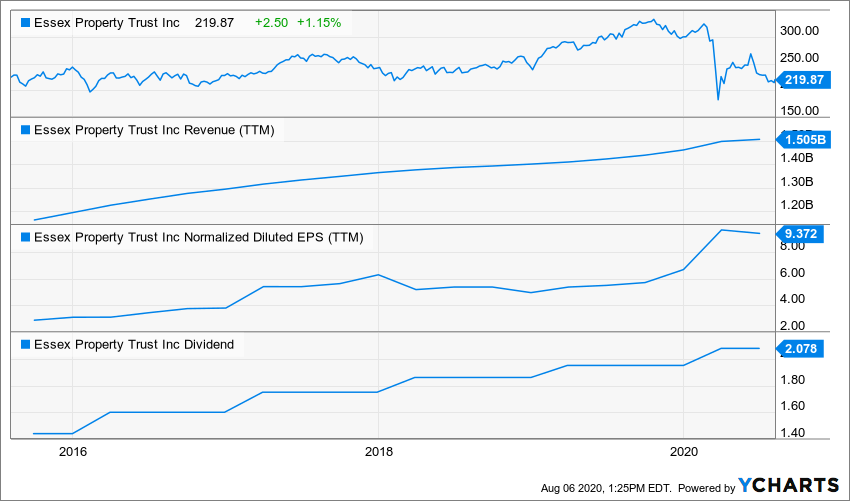

Essex Property Trust (ESS)

What’s the story?

ESS is a good example of an “educated guess”. The REIT is going through a difficult year since demand for apartments is in freefall due to the recession. This was a bad quarter for Essex as the REIT missed on both FFO and revenue growth expectations. Q2 same-property gross revenue declined by 3.8% and same-property net operating income fell by 7.4% as ESS recorded an additional $9.7M of delinquencies in Q2 2020 vs. the year-ago period. Excluding those delinquencies, same-property revenue would have declined 0.9% and NOI would have fallen 3.5%. Management is confident in the coming months as employment trends in their regions are improving. This should boost demand for apartments going forward.

Keep in mind ESS owns apartments spread across Southern California (40% of NOI), Northern CA (43%), and Seattle (17%). Those regions should benefit from the tech industry explosion. Tech companies will employ more people (Amazon hired 175,000 new workers since March) and the need for quality apartments should remain solid going forward.

Business Model

Essex Property Trust owns a portfolio of 250 apartment communities with over 60,000 units and is developing seven additional properties with 1,960 units. The company focuses on owning large, high-quality properties on the West Coast in the urban and suburban submarkets of Southern California, Northern California, and Seattle.

Investment Thesis

Essex Property Trust is everything a REIT should be: a dominating position in a rich market, a decent yield, and a stellar dividend growth history. Most income seeking investors are looking at REITs with poor growth vectors and high dividend yield. If you are willing to go under the 4% yield level, you will find this beauty. Your income will be safe and protected against inflation. Plus, you will likely enjoy some value appreciation over the long haul. During the recession of 2008, ESS kept increasing its dividend while maintaining a strong FFO per share. The REIT positioned itself during the recession to make sure it thrives once the economy was ready to roll again. ESS regularly acquires multiple family REITs and successfully integrates them in their business model. Finally, Essex is well-established in rich and growing markets with the state of California and the city of Seattle. This REIT should ride on strong demographic and job growth tailwinds in the upcoming years.

Potential Risks

If you read the investment thesis, I think we made it clear that we like ESS. Its narrow market concentration is at the center of its success. In the past, we also saw similar growth stories ending in nightmares. While it seems unlikely to see California becoming a poor state, an important economic slowdown would greatly hurt ESS’s business model. ESS is clearly making a play on the tech sector by focusing on tech hub such as San Francisco and Seattle. The REIT usually offer short leases opening the door for more revenue volatility. Demand for apartments come and go. Building too many properties could end-up with oversupply in the event of a severe recession.

Dividend Growth Perspective

This REIT has successfully increased its dividend yearly since 1995. This means Essex has never missed a dividend increase since its IPO in 1994! ESS is generating strong funds from operations (FFO) quarter after quarter. During their latest earnings report (ending March 31, 2020), the REIT posted core FFO per share of $3.48 while paying a $2.078/share dividend. We are talking about a 55% payout ratio. Shareholders can sleep well with a ~3.5% yield and a dividend increasing by 5-6% year after year.

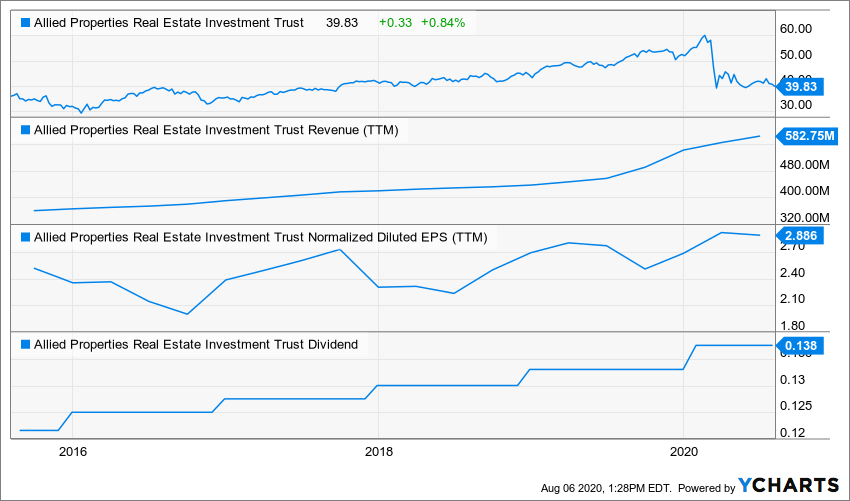

Allied Properties REIT (AP.UN.TO)

What’s the story?

Allied possesses one of the strongest balance sheets among REITs. It has raised much of their capital at low costs and is now paying down higher interest debt at the same time as they are investing in new projects. The company has developed a unique expertise in managing and developing prime spots with historic heritage which will continue to be in high demand in the coming years. The REIT also counts on many tech clients which should do well during the pandemic. You will not find many REITs that are able to systematically grow both their assets and dividend at the same time.

The company currently shows an Adjusted Funds from Operations (AFFO) payout ratio of 83% (June 2020) leaving more than adequate room for future dividend increases. Considering the pandemic, Allied updated its FFO and AFFO guidance for 2020. It now expects flat-to-mid-single-digit percentage growth in each of same-asset NOI (Net Operating Income), FFO per unit and AFFO per unit. Not bad for what many people call “the worst recession since the Great Depression”.

Business Model

Allied Properties Real Estate Investment Trust is a real estate investment trust engaged in the development, management, and ownership of primarily urban office environments across Canada’s major cities. Most of the total square footage in the company’s real estate portfolio is located in Toronto and Montreal. Allied Properties derives nearly all of its income from rental revenue from tenants in its properties. The majority of this revenue comes from its assets located in Central Canada. Allied Properties’ major tenants include IT, banking, government, marketing, and telecommunications firms. The company also controls a number of telecommunications/IT and retail properties within its real estate portfolio.

Investment Thesis

Allied shows one of the strongest balance sheets among REITs. It has raised lots of capital at low cost and is now paying down higher interest debt at the same time as investing in new projects. The company has developed a unique expertise in managing and developing prime spots with historic heritage which will continue to be in high demand in the upcoming years. The REIT also counts on many tech clients which should do well during the pandemic. You will not find many REITs that are able to systematically grow both their assets and dividend at the same time.

Potential Risks

Ah! Here’s the classic question. “Mike, why would you talk about a stock showing a DDM value so low?!?” There is “no value” in buying AP at a price around $40. In fact, what you buy with AP is not upside potential, but rather a strong REIT that is evolving in a robust niche market. AP will have a difficult 2020 (and possibly 2021) because 70% of its income is derived from office properties. Nonetheless, the REIT is not at risk with a collection rate of 90% for April 2020. Management hasn’t touched its dividend either.

Dividend Growth Perspective

When we look at a REIT, all we hope is that the dividend increase will match inflation. This is the case with AP. The company has posted a 2.45% dividend CAGR over the past 5 years and shows strong FFO and AFFO growth lately. Therefore, you can expect a 2-3% dividend growth going forward. As of Q4 2019, the REIT shows an AFFO payout ratio of 83.3%. Considering the pandemic, don’t get your hopes up for a raise in 2021, but the dividend remains safe so far.

More Ideas in The 2020 Dividend Achievers List

As the two stocks discussed today are REITs, you might want to consider your sector allocation and don’t buy both! If you’re looking for more diversification, I’ve built a strong and free Dividend Achievers List for you to download.

With the right combination of metrics, this list is probably the best starting point for building your own dividend growth portfolio or to at least find your next addition to that portfolio.

The post REITS: Two New Ideas for Your Retirement Portfolio appeared first on The Dividend Guy Blog.