Not too long ago, I told you that you should run away from Walmart (WMT) as I did. This transaction left me with a healthy profit and additional cash in my portfolio. This was the perfect time to go hunting! As part of a Dividend Stocks Rock project, I’ve reviewed the 18 Dividend Kings. This gave me a few ideas for potential buy and I decided to use my money to buy 57 shares of LOW.

What I Like so Much about Lowe’s Business Model

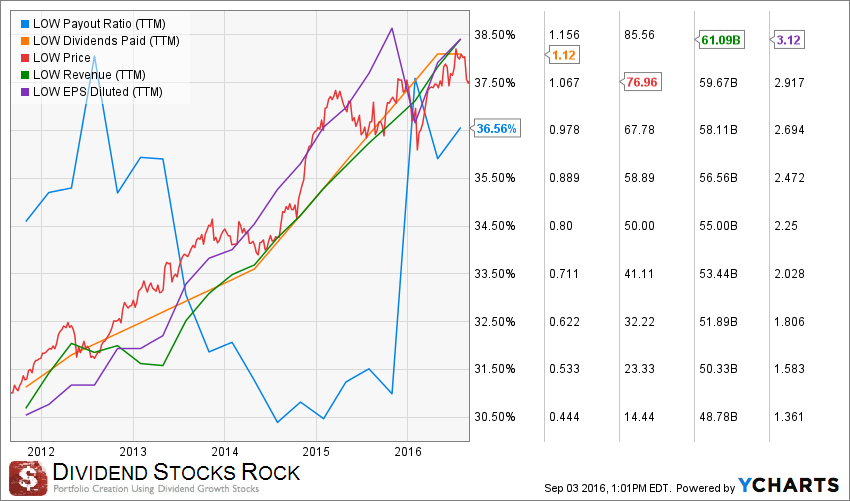

Source: Ycharts

LOW is the 2nd largest home-improvement retailer in the world showing $61 billion in revenue over the past 12 months. Lowe’s use its strong position in the U.S. to generate sufficient cash flow to find growth opportunities across the world. This is how they purchased Rona (RON) in 2016. Once this acquisition is fully integrated within its business model, LOW is more likely to continue with its appetite for other players.

Speaking of its business model, this is what seduced me about Lowe’s. Lowe’s doesn’t only focus on selling you home renovation and improvement products, it also uses its experienced sales-force to provide you with additional advice. This good advice builds a stronger bond between the customer and the company, and it also leads to several cross-selling opportunities. The company has also successfully built a solution-based segment within its stores.

The solution-based segment offers a variety of package for customers or entrepreneurs who want to renovate their kitchen, bathroom, build a patio, etc. This model offers great margins and also brings more contractors on board with them. By offering a complete solution from start to finish, Lowe’s make sure to “capture” the customer for its entire project purchases.

LOW’s Dividend Perspective

As I clearly demonstrated in my Walmart analysis (if you have missed this, you can read that Target (TGT) is in the same boat too!), WMT’s earnings are stagnating which will eventually limit management’s ability to increase their payouts. However, this is definitely not the case with Lowe’s:

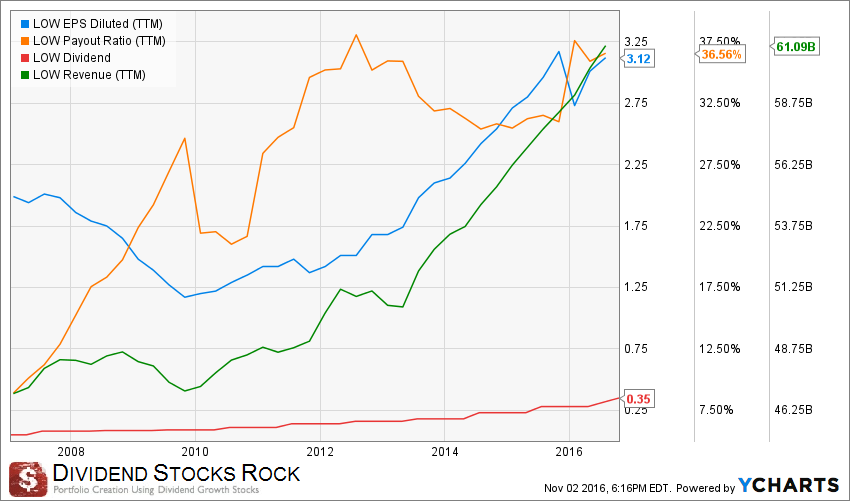

Source: Ycharts

As you can see, the blue line and the green line represent LOW earnings and revenue over the past 10 years. They clearly follow the same trend while the dividend payment is carefully increased but with a lower trend. The company’s payout ratio is very low at 36.56% while management has all the room they want to please shareholders with future dividend increases.

I bought LOW during their most recent drop (paid $68/share) which gives me a starting dividend yield of 2.05%. This is not much for now, but considering the stock price jumped by 209% over the past 5 years, it’s only normal the dividend yield is not that high. As I previously mentioned, Lowe’s is a Dividend King and currently show 53 consecutive years with a dividend increase. Considering the latest fundamentals, LOW clearly demonstrate they will continue to honor their dividend king reputation for several years.

LOW Vs My 7 Investing Principles

When I purchased shares of a company, I based my analysis on the 7 dividend investing principles. These principles have been elaborated based on academic studies and provide a strong guideline as not only to which company to buy, but at what price and when it is the right time to sell them. I’ve recently conducted my diligence on LOW and the company meets my 7 investing principles (read the full analysis here). In this analysis, I also show that LOW fair value from a dividend growth investing perspective is $96.79. Therefore, $68 seems like a great deal, don’t you think?