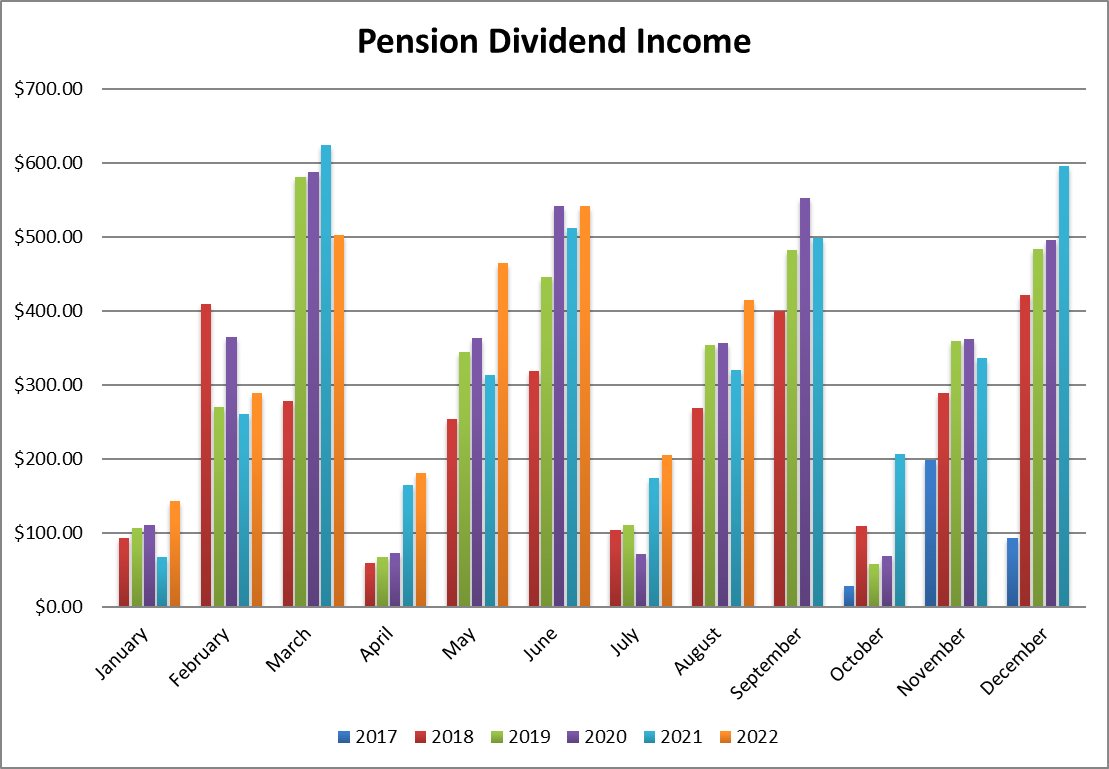

In September of 2017, I received slightly over $100K from my former employer, representing the commuted value of my pension plan. I decided to invest 100% of this money in dividend growth stocks.

Each month, I publish my results on those investments. I don’t do this to brag. I do this to show my readers that it is possible to build a lasting portfolio during all market conditions. Some months we might appear to underperform, but you must trust the process over the long term to evaluate our performance more accurately.

Performance in Review

Let’s start with the numbers as of September 2nd, 2022 (before the bell):

Original amount invested in September 2017 (no additional capital added): $108,760.02.

- Portfolio value: $202,761.78

- Dividends paid: $4,379.58 (TTM)

- Average yield: 2.16%

- 2021 performance: +16.78%

- SPY= 28.75%, XIU.TO = 28.05%

- Dividend growth: +3.14%

Total return since inception (Sep 2017- August 2022): 86.43%

Annualized return (since September 2017 – 60 months): 13.27%

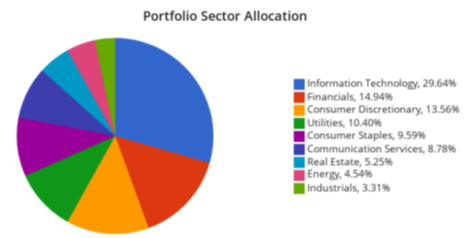

Sector allocation calculated by DSR PRO

Quitting My Job, And Investing My Pension Plan

Wow… time really does fly when we are having so much fun! 5 years ago, I returned from a one-year RV trip with no money and no job. To be fair, all my money was invested in my retirement account, and I didn’t have a safety net because I used all my resources to finance our trip. A decision, to this date, that appears to have been the best decision I ever made.

The second-best decision I made (besides marrying my wife, of course) was to quit my job upon my return from Central America and focus all my attention on Dividend Stocks Rock (DSR). In September of 2017, I made another important decision: I took the money I had in my former employer’s pension plan and decided to manage it myself. It was somewhat stressful since it was the bulk of my retirement nest egg. Plus, the market was trading at its all-time high, and most investors agreed the market was greatly overvalued at that time.

5 years later, I have done better than the pension plan managers (they have rules to follow, and I understand that). But most importantly, I can see the fruits of my labor. I’ve built and improved DSR as I managed my portfolio. I created tools for my members and used the same tools to ensure that I would retire stress-free. I’ve learned much during these past 5 years as an entrepreneur and investor.

Be true to yourself and help others

The creation of DSR was first prompted by my desire to help people with their investments. I’ve noticed that too many investors have unanswered questions or look for the support they can’t get from their advisor or their bank. My plan was to create a resource for each investor so they could feel empowered in making their investments. It’s fun to build a business and see it thrive, but it is even more meaningful when you see your members succeed. I thank everyone for their trust, and I pledge to continue to deliver on our promise of helping you invest with confidence and conviction.

Next week, on Thursday, September 22nd, I will host a webinar on investing during a crisis. I’ll address the delicate situation of being a retiree (or soon-to-be retired person) in this crazy market.

Save your spot now (limited to 500 live attendees).

We know nothing about valuation

When I received my pension check in early September of 2017, many readers suggested that I wait before investing the money. I took about 3 months to fully invest my money as my attention was split between building my business and investing my pension plan. Therefore, I bought at the market’s 5-year peak when everybody said the market was greatly overvalued. Interestingly, I never went below the original amount invested since then. Not even at the bottom of the 2018 bear market, nor at the bottom of the 2020 covid crash.

Time in the market beats market timing

I have made mistakes with this portfolio (Lassonde Industries and Andrew Peller for example), and I also made some great moves (like Alimentation Couche-Tard, Apple, and Microsoft). However, my portfolio still beat the market after 5 years and two bear markets (and soon 3) because I stayed invested the whole time. Selecting high-quality dividend growers will make you a winner over the long run. You must trust the process, stay focused, and stay in the market!

Dividend growth investing works during good times and bad times

If you are not a DSR member, you may not know, but my “veterans” know that my portfolio even ended 2018 on a positive note. While most investors were down 5% to 10% (the S&P 500 ended the year at -4.5% and the TSX at -7.8%, including dividends), my portfolio was up by a few points. What was the secret? A favorable currency shift and steady dividends are paid to minimize losses. I’m not in positive territory this year, but I’m doing much better than the market. Those steady payments continue to work their magic while I stay invested.

Take risks; life must be fun

This one is not about investing; it’s about life in general. To many folks, I took a huge risk by quitting a 6-figure job padded with a bullet-proof pension plan. But I decided to have fun instead. Quitting my job wasn’t so much about taking a risk. In fact, I felt it was a way to secure my future financial situation. Being in control and fully responsible for your finances are the keys to achieving a successful retirement. Today, I don’t think I’m employable anymore. I just love doing what I do and relish the freedom to choose what I do each day.

If you do what you love, you don’t have to work

This one seems obvious, but it takes everything you have to make it happen. You must go against social pressure about what is commonly accepted, but if you really do what you love, you won’t have to work a single day of your life.

Most of the time, I choose to stay at my computer to finish a newsletter or read a financial article. I just love doing what I do. I hope I have successfully transferred some of that passion to you when you read my newsletter, watch my webinars, or listen to my podcasts!

Smith Manoeuvre Update

So far, I’m breaking even with my strategy. I admit that I didn’t expect much from this portfolio over a few months. I still need to give it some time to perform (especially considering this crazy market).

I must initiate a pause in my SM contributions. In the coming months, I will maintain my investment update, but I will not add another $500 monthly for awhile. My trip to Africa got out of control and I must take a few months to recover financially. When you do a leveraged strategy, you should never invest the money you don’t have. I’m following my own advice. I’ll resume my monthly investments shortly, but I would rather play it safe in the meantime.

Here’s my portfolio as of September 2nd, 2022 (before the bell):

| Company Name | Ticker | Sector | Market Value |

| Canadian Net REIT | NET.UN. V | Real Estate | $422.22 |

| National Bank | NA.TO | Financials | $521.88 |

| Exchange Income | EIF.TO | Industrials | $503.91 |

| Brookfield Infrastructure | BIPC.TO | Utilities | $554.40 |

| Great-West Lifeco | GWO.TO | Financials | $521.05 |

| Cash (Margin) | -$24.00 | ||

| Total | $2,499.46 | ||

| Amount borrowed | -$2,500.00 |

Let’s look at my CDN portfolio. Numbers are as of September 2nd, 2022 (before the bell):

Canadian Portfolio (CAD)

| Company Name | Ticker | Sector | Market Value |

| Algonquin Power & Utilities | AQN.TO | Utilities | $7,531.02 |

| Alimentation Couche-Tard | ATD.B.TO | Cons. Staples | $21.098.43 |

| Brookfield Renewable | BEPC.TO | Utilities | $7,099.35 |

| CAE | CAE.TO | Industrials | $4,652.00 |

| Enbridge | ENB.TO | Energy | $8,676.29 |

| Fortis | FTS.TO | Utilities | $5,775.66 |

| Granite REIT | GRT.UN.TO | Real Estate | $9,382.40 |

| Magna International | MG.TO | Cons. Discre. | $5,247.90 |

| National Bank | NA.TO | Financials | $10,524.58 |

| Royal Bank | RY.TO | Financial | $7,313.40 |

| Sylogist | SYZ.TO | Inf. Technology | $2,793.90 |

| Cash | 584.44 | ||

| Total | $90,679.37 |

My account shows a variation of -$4,485.01 (-4.7%) since the last income report on August 4th. Ironically, I lost about the same amount of money I made the last month. All that to say that when tracking your portfolio monthly, don’t go crazy on short-term fluctuations (good or bad!)

There were several Canadian stocks reported in the past few weeks; here’s my review:

Algonquin Power & Utilities

Algonquin reported strong revenue growth of 18%, mostly driven by recent acquisitions. Adjusted EPS was up 7%. The utility company completed two projects recently. In April, the Blue Hill Wind Facility started generating power (175 MW) in Saskatchewan. In August, the Renewable Energy Group completed its acquisition of Sandhill Advanced Biofuels. Previous investments are starting to pay some serious cash flows!

Alimentation Couche-Tard is simply brilliant!

ATD beat analysts’ expectations with strong growth (Revenue up 37%, EPS up 20%). Results were driven by higher road transportation fuel margins, convenience stores’ organic growth and share buybacks. What’s not to love? Even better, the company announced it will provide 7,000 of its convenience stores (mostly Couche-Tard and Circle K) with AI-powered self-checkout cashiers. ATD will also create a reward program to know more about its customers (spending habits, amounts, time, type of purchases, etc.).

We have also discussed ATD among the Best News from Q3 in this recent podcast episode.

Quarterly Earnings Review: Best and Worst News [Podcast]

Brookfield Renewable keeps growing

Brookfield Renewable reported FFO of $294 million or $0.46 per Unit for the three months ended June 30, 2022, a 10% increase on a per Unit basis. Growth was driven by strong asset availability, higher power prices, and continued growth through development and acquisitions. The company continued advancing many projects and closed or agreed to invest $3 billion across various transactions and regions.

CAE got bombed!

CAE created a bomb with this quarter. While revenue jumped 24% (bolstered by acquisitions), CAE reported adjusted EPS of $0.06, down by 68% and lowered its outlook for the current year. CAE is facing major headwinds in the defense sector, namely supply chain pressures, labor shortages, and a slower defense contracting environment resulting in unfavorable contract profit adjustments in Defense. At least, Civil aviation reported revenue growth of 11% and Operating income growth of 26%. We believe CAE’s headwinds in the defense sector won’t last forever and the company will report stronger earnings in 2023.

Enbridge keeps flooding my account with dividends

Enbridge reported an okay quarter, but the market was disappointed by the lack of EPS growth. However, the distributable cash flow (DCF) was up from $2.5B to $2.7B. We are talking about an increase from $1.24 to $1.36 (+10%) on a per-share basis. A dividend of $0.86 brings the payout ratio for the quarter to 63.2%, in line with the company’s target. Management reaffirmed 2022 full-year guidance range for EBITDA of $15B to $15.6B and DCF per share of $5.20 to $5.50 (payout to be between 62.5% and 66%).

Fortis is boring and that’s what I like about it

Fortis reported Q2 2022 EPS of $0.57, a 3.6% increase compared to the same period last year, and missing estimates by $0.02. Revenue reported for the quarter was $1.94B, a 13% increase versus Q2 2021, and beating estimates by $166.80M. Growth in earnings was driven by rate base growth and higher earnings from the energy infrastructure segment. A higher U.S.-to-Canadian foreign exchange rate also favorably impacted results. Growth in earnings was partially offset by losses on investments that support retirement benefits at UNS Energy and ITC, reflecting market conditions. Fortis achieved a 20% reduction in Scope 1 emissions through 2021.

Granite REIT keeps ramping up AFFO double-digit

Granite REIT reported another solid quarter with FFO up 8% and revenue up 17%. The AFFO payout ratio was 75% for the second quarter of 2022 compared to 79% in the second quarter of 2021. Growth was fueled primarily by net acquisition activity beginning in the second quarter of 2021. Same property net operating growth was 3.6%, showing how rent increases can at least partially fight inflation. Granite also completed mass grading at its development site in Brantford, Ontario and after the quarters end signed an approximate 20-year lease agreement with a leading manufacturer of chocolate and cocoa products for 0.4 million square feet.

Magna International did better than expected

Magna International reported Q2 2022 EPS of $0.83, missing estimates by $0.09. Revenue reported for the quarter was $9.36B, representing a 4% increase when compared to Q2 2021, and beating estimates by $437.12M. Revenue growth was primarily driven by the increased production of light vehicles of 2%, largely driven by a 14% increase in North America. EBIT as a percentage of sales decreased to 3.8% compared to 6.2%, largely because of higher net production input costs, as well as operating inefficiencies and other costs at a facility in Europe. Finally, the company reported a dividend payment of $0.45, which was flat compared to the previous quarter.

National Bank is strong during the storm

National Bank reported flat EPS (net income down 2%), but revenue grew by 8%. Revenue grew across all segments, but higher PCLs for U.S. + Intl segment crashed the earnings party. Personal & Commercial income was up 11%, bolstered by loan volume growth and stronger net interest margin. Wealth Management was up 10%, mostly driven by growth in net interest income. Financial Markets was up 12% on stronger revenue. U.S. + Intl segment was down 22% due to higher PCLs (but revenue was up 10%). In other words, if PCLs aren’t realized, National Bank will make big money next year for the same quarter.

You can watch my complete Canadian Banks Q3 review here.

Royal Bank got burnt by Provisions for Credit Losses (PCLs)

Royal Bank reported a double-digit EPS decline of 15%. Results included a provision for credit loss of $340M (vs -$540M last year) as the economic landscape gets darker. Personal & Commercial Banking was down 4%, mostly due to PCLs. Results were partially offset by loan growth (+10%) and deposits (+9%). Wealth Management did well at +4%, fueled by strong volume growth. Insurance was down 21%, primarily due to the impact of new longevity reinsurance contracts in the prior year. Capital Market was down 58%, due to the impact from loan underwriting markdowns of $385M primarily in the U.S., largely driven by challenging market conditions.

Sylogist is doing something good (about time!)

Finally! Sylogist is putting a smile on investors’ faces as the company reported record revenue of $13.7M (up 44%) and an increase of 50% in EPS. We are not out of the woods yet, but it’s a step in the right direction. Most of the growth was driven by recent acquisitions, but the company still reported organic growth of 7%. Recurring revenues from subscriptions and maintenance were $9.0 million, compared to $7.9 million, an increase of 13%. In the past two quarters, we have seen strong revenue growth and now EPS is back with positive numbers. We expect another strong quarter this fall.

Here’s my US portfolio now. Numbers are as of September 2nd, 2022 (before the bell):

U.S. Portfolio (USD)

| Company Name | Ticker | Sector | Market Value |

| Activision Blizzard | ATVI | Communications | $9,111.80 |

| Apple | AAPL | Inf. Technology | $11,847.00 |

| BlackRock | BLK | Financials | $9,307.90 |

| Disney | DIS | Communications | $5,063.85 |

| Gentex | GNTX | Cons. Discret. | $6,356.75 |

| Microsoft | MSFT | Inf. Technology | $14,322.00 |

| Starbucks | SBUX | Cons. Discret. | $7,259.00 |

| Texas Instruments | TXN | Inf. Technology | $8,308.00 |

| VF Corporation | VFC | Cons. Discret. | $3,354.21 |

| Visa | V | Inf. Technology | $10,006.50 |

| Cash | $257.89 | ||

| Total | $85,194.90 |

The US total value account shows a variation of -$4,145.47 (-4.6%) since the last income report on August 4th. There was only Disney left to report their earnings in August. Disney is back in business baby! The company reported a strong quarter as Disney Parks revenue jumped 70% to $7.39B. Overall, EPS was up 36% while revenue jumped 26%. Another great piece of news is that DIS is now tied to the world largest streaming services in term of subscribers (hard to believe, right?). The company added 14.4M Disney+ subscribers, a 31% year-over-year jump that brought that service to 152.1M subscribers. If you combine all services (Disney+, Hulu, ESPN+), you get 221.1M subscribers vs 221.67M for Netflix.

My Entire Portfolio Updated for Q3 2022

Each quarter, we run an exclusive report for Dividend Stocks Rock (DSR) members who subscribe to our special additional service, DSR PRO. The PRO report includes a summary of each company’s earnings report for the period. We have been doing this for an entire year now and I wanted to share my own DSR PRO report for this portfolio. You can download the full PDF showing all the information about all my holdings. Results have been updated as of July 7th, 2022.

Download my portfolio Q3 2022 report.

Dividend Income: $414.77 CAD (+29.60% vs August 2021)

It was a great month in terms of dividend payments! In fact, this is where my focus is, especially during downturns! When I see that my portfolio generates more income year after year, I know the businesses I own are healthy. Therefore, the price of their shares isn’t relevant.

This month, my portfolio’s dividend was bolstered by additional shares of National Bank, new payments from Granite and several dividend increases over the past 12 months (Royal Bank, Starbucks, and Texas Instruments).

I received less in Apple dividends since I sold a few shares along the way while I had to kiss my Lazard share goodbye.

Finally, the USD is getting stronger as the market is weaker (+6%).

Here’s the detail of my dividend payments.

Dividend growth (over the past 12 months):

- Magna Intl: (paid in August 2021)

- Royal Bank: +18.5%

- Granite: new

- National Bank: +96% (added shares)

- Starbucks: +8.9%

- Texas Instruments: +12.74%

- Apple: -18% (sold shares)

- Currency factor: +6%

Canadian Holding payouts: $261.63 CAD

- Magna Intl: $40.45

- Royal Bank: $76.80

- Granite: $33.06

- National Bank: $111.32

U.S. Holding payouts: $116.40 USD

- Starbucks: $41.65

- Texas Instruments: $57.50

- Apple: $17.25

Total payouts: $414.77 CAD

*I used a USD/CAD conversion rate of 1.3156

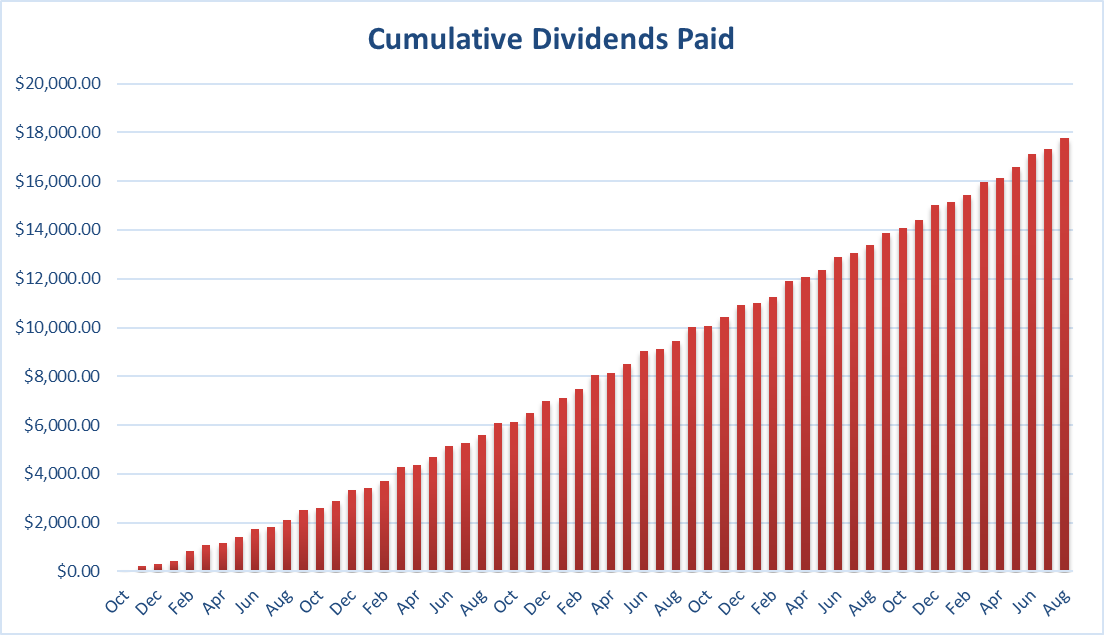

Since I started this portfolio in September 2017, I have received a total of $17,752.14 CAD in dividends. Remember that this is a “pure dividend growth portfolio” as no capital can be added to this account other than retained and/or reinvested dividends. Therefore, all dividend growth comes from the stocks and not from any additional capital added to the account.

Final Thoughts

I have noticed how the USD has gained power over the CAD over the past few weeks. This may be the perfect opportunity to sell some shares of Apple as I highlighted in my previous newsletter. I could cash a good gain on a few shares and then benefit from the strong USD to transfer money into CAD.

Cheers,

Mike.

The post Quitting My Job and Investing My Pension Plan – August Dividend Income Report appeared first on The Dividend Guy Blog.