This last segment about my retirement planning series (you can read Part I, Part II, Part III and Part IV) is probably the most difficult part to discuss. Retirement is a case by case story. Nobody has the same portfolio, age, retirement plans and capacity. This is why it is so difficult to write something that will reach most of you. However, I’m giving a try today as I know the following question tickles more than one:

How do I manage my portfolio at retirement?

The biggest change happening to your portfolio at retirement is in your mind. In theory, chances are that you will have to manage your portfolio for the next 25 to 35 years depending on when you retire and how old you live. Therefore, your portfolio should remain aimed at a long-term horizon. I even met many clients in my previous life that kept the same strategy until they pass away. As the remaining of their money was going to their heirs and they wanted their money to grow for the next generation in the meantime.

Retirement is often synonym of not receiving an active income anymore. You either live on various pension, rental income or passive income such as dividend payments. Therefore, you want to make sure your asset producing your income are in very good shape. Volatility and variability are two concepts that you want to keep away from your retirement income source. With this in mind, choosing dividend growth investing seems the logical choice to manage your portfolio (if you haven’t already adopted this method years ago!).

Asset allocation

Even if you pick dividend growth stocks, your portfolio will fluctuate. Selecting strong companies doesn’t protect you from short term fluctuation. However, if you build a group of diversified companies across different industries, chances are you will outperform greatly the stock market during crashes… even if you are 100% invested in stocks.

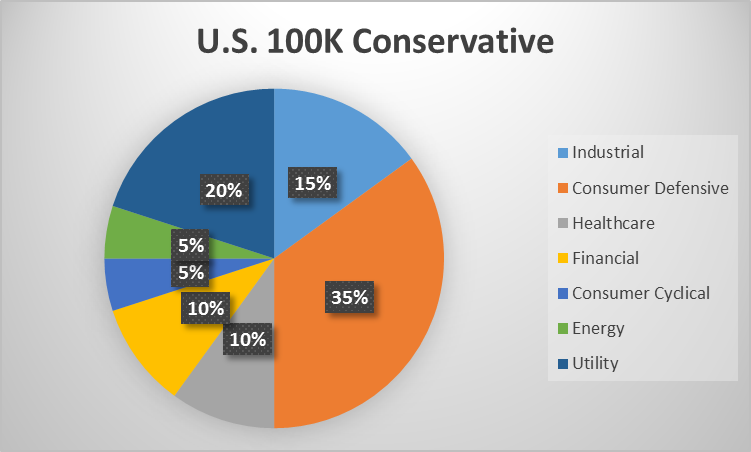

In order to illustrate how a retirement portfolio could be invested, I’ve selected our 100K Conservative Portfolio model at DSR. This portfolio is outperforming its benchmark by 13.42% total return over the past 3.5 years (click here to see our returns).

For a conservative portfolio, it is important to have a solid base of consumer defensive stocks. These companies will generally grow at a slower pace, but will provoke less waves than other sectors. You can select other sectors that will continue to support this portfolio such as utilities, industrial, healthcare and financial. This is a portfolio built to go through any kind of storm on the market.

I know it is very tempting to focus on higher yield stocks or to pick many companies among a bullish industry, but sooner or later, this is the kind of choices that will come back and bite you. While you pick various industries, you shelter your capital from any massive drop.

Consider Taxes

Another “easy” way to improve your return is to perform a tax optimization strategy on your portfolios. At retirement, you will have money invested in various type of account. Some will be tax sheltered and some others won’t. Depending on where you live and how your money is distributed, you can make shift in your portfolio. The idea is to pick the highly taxed investment assets such as bonds in your tax-sheltered account while leaving the growth oriented vehicles (such as stocks) in taxable accounts (as the capital gain is taxed only when you sell you asset).

Many investors make the mistake to avoid tax optimization as it creates distortion in your asset allocation by account. Here’s an example:

Let’s assume you have $1,000,000 invested in 2 accounts; a taxable account and a tax-sheltered account. Imagine you have $500K invested in each and that you have a balanced investor profile (50% invested in equity and 50% in fixed income). Most investors would probably show the following asset allocation:

Such asset allocation makes it very easy to manage your portfolio. You basically manage each portfolio in a similar manner and they will show similar returns. However, if you perform a tax optimization strategy, your asset allocation should look like the following:

When you hold fixed income in your portfolio, you are paying taxed on the interest or dividend generated from your assets regardless if you are withdrawing them or not. This is why it is so important to shift all your fixed income assets into a tax-sheltered account. On the other side, capital gain tax is triggered only upon the sell of an asset. If you keep your stock in a taxable account, you will pay virtually no taxes unless you sell something.

Assume both asset classes generate 5% return (5% taxable income from the fixed income and 5% capital gains from equities) and your tax rate is 25%. Your million dollars would generate $50,000 per year. If you didn’t sell any equity, only half of your taxable account will be subject to taxes (the $250K invested in fixed income). This part would generate $12,500 in taxable income ($250K * 5% return), and you would pay $3,125 in taxes (25% of $12,500). This is $3,125 of taxes you would not have to pay if you have 100% of your fixed income invested in a tax-sheltered account. Do you think you could use an extra $3K at retirement? I think so!

*Please note that this kind of strategy must be reviewed by a tax expert to make sure it is done properly according to your own financial situation. Many other factors (such as other type of income, residency and age) could affect your situation.

Now that you have selected a solid asset allocation and you have optimized it, how do you live from your portfolio? Let’s look at two different withdrawal strategy.

Live on your portfolio yield

In an ideal world, you would never have to withdraw capital from your portfolio. Living on your dividend payouts would be the perfect case scenario. A year prior to retire, you would stop reinvesting your dividend payments and let them accumulate in your cash account. This technique would avoid cash flow gap created by the fact that all companies don’t pay their distribution at the same time.

Imagine that you receive $50,000 in dividend per year, this would make roughly $12,500 received quarterly. Then, imagine that in January you receive $500, in February $8,000 and in March $4,000. This would make budgeting a little bit difficult. However, if you already have $50,000 in cash on year #1 of your retirement, you can easily withdraw enough money each month to pay your bills. Plus, you also have room for some extra expenses (that are most likely to happen during your first years of retirement).

Another advantage of living on your yield on top of not touching your capital is that strategy may also protect you from inflation. Technically, you should consider a 2% inflation rate in your plan. Most dividend growth portfolio will show a dividend growth rate over the inflation. Therefore, you have nothing to do but keep receiving your ever increasing dividend payment year after year and you will lack of nothing!

Unfortunately, the biggest problem we will all run into is that our portfolio doesn’t generate enough in dividend yield to allow us to retire. Let’s look at the other option…

What happen if you can’t

I really wish you build a 1M$ portfolio generating 5% yield, but you need a plan B just in case. Imagine that you need $50,000 per year and you retire with $1,000,000 generating… 3.75%… bummer! Each year, you will need an extra $12,500 that cannot come form dividend payments.

Even if you stop reinvesting your dividend one year prior to your retirement, you will only generate a buffer of $37,500 that would last 3 years. This is not a good option. If you have to withdraw a part of capital from your investment each year, you will need to carefully plan it. Here are a few options:

Option #1: Sell a part of your largest holdings. We all have our “favorite” or our “very good move” that makes our portfolio a little bit off balance. If all your holdings weight about 5% of your portfolio, but you have one showing 10%, this is the one you should hit first. This will help you balance your portfolio and reduce volatility. Plus, you avoid doubting which company to pick (and fear of making the bad decision).

Option #2: Sell a little bit of everything. Another “easy” solution is to sell a few shares of each of your holdings to compensate. This method also has the advantage of avoiding getting stuck in a perpetual dilemma of “Eenie, Meenie, Miney, Mo”. However, this will generate a lot more transaction fees. If you are going for this option, I’d suggest to do it only once a year.

Options #3: Get rid of one position at a time. This option refers of picking one company each year and sell your position (or a good part of it). It will be less costly in term of transaction fees, but you might pay a larger price if you are making the wrong decision.

Final thoughts

I’m still working on building my dividend portfolio and I haven’t thought much about how I will withdraw my money once I retire. After writing this article, I think I would ahead with option #2 and sell a little bit of everything. There is a reason why I will have XYZ asset allocation at retirement and I want to keep it intact. Plus, paying a little bit more in transaction fee is a small price to pay to make an automatic decision that cannot hurt my portfolio.

I guess the key is to keep a buffer no matter what your situation is. If you have the equivalent of 1 year of retirement in cash before you stop working, it will be easier to make your financial moves in the future. Do not let liquidity dictate your action!