Last Thursday, Telus (T.TO or TU), beat the analysts’ estimates once again with net income rising by 7.6% and EPS by 8.5% compared to last year’s quarter. Overall, here’s what Telus did in the past quarter:

– Strong new customer growth (135,000 connections, 118,000 post paid mobile, 28,000 Telus TV and 22,000 high speed internet).

– Leading customer loyalty

– Mobile based clientele up by 3.8% to 8,1 million customers

– $1.5 billion returned to shareholders through shares buybacks and dividends paid

– Aim for more growth (2015 revenue growth guidance at 5%)

The stock is up 170% for the past 5 years and I don’t even count the dividend yield. Besides the short drop during the summer of 2013 due to the potential entry of telecom giant Verizon (VZ) in the Canadian market, the stock has barely ever suffered during this period. Now that the threat of seeing Verizon selling mobile phones to Canadian is gone, Telus keeps breaking records. A quick look at its profile will convince you it’s a strong blue chip to add to your portfolio:

But how Telus can keep up its growth? Most importantly, how Telus can keep a 10% dividend growth rate in the future? Is is time to sell Telus and cash out your profit or is there still lots of battery power to keep talking on the phone?

This Canadian Dividend Aristocrats started paying a dividend in 1999 and has never stopped increasing since 2001 (after a dividend cut between 2000 and 2001). The dividend paid quarterly in 2001 was $0.075 per share and is now at $0.40 per share.

Business Model

Telus has been providing communication services for over 100 years. The business has evolved greatly over the past 20 years. We can now divide the Telus business model into two segments:

Wireless services

This is now the bread and butter of the company. Telus is known for keeping its clients and shows a high profit margin per customer. With a growing client base (up 3.8% to 8.1 million), Telus wireless services assure an interesting growth for the future. They also cover all Canada’s important part:

Wireline Segment:

Telus not only provides wireline phone services but also internet connectivity and TV cable services. While the wireline phone business is slowing down, Telus compensates by adding other wireline services to its wireless customers. That explain why the internet and TV services are growing this fast.

Now let’s go delve further into the numbers. Following the first 4 Dividend Stocks Rock Investing Principles, I’ll take a look at Telus and share a full dividend analysis.

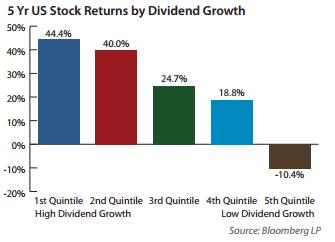

Principle #1 High Dividend Yield Doesn’t Equal High Returns

Did you know that the highest dividend yield stocks underperform more “reasonable” yielding stocks? The Hartford Mutual Funds company wrote:

The study found that stocks offering the highest level of dividend payouts have not performed as well as those that pay high, but not the very highest, levels of dividends.”

Read more about this research here.

Therefore, the point is to pick companies with a good dividend yield, but not aim for something way above the market. Telus’ dividend yield is currently around 3.70%. This yield is not only more than inflation rate but also above the prime borrowing rate. You can then even buy this stock on margin and pay the interest with only the dividend payout. This places the company above the average dividend yield but not in the first quartile of the highest dividend payer either. In other words; Telus’ dividend yield is in the perfect spot to provide both a great sources of revenue and higher than average capital appreciation.

Principle #2: If There is One Metric; It’s Called Dividend Growth

If I had to go blindfolded to pick a stock and have only one metric to look at, I would pick dividend growth. This is the most important metric to me as it is a clear sign of the company’s financial health and its ability to pay me for years to come. Here’s an interesting quote from Saturna Capital:

“Indeed, dividend growth has been a much larger determinant of equity returns in this new era of low benchmark rates and higher levels of uncertainty.”

You can get the full detail here.

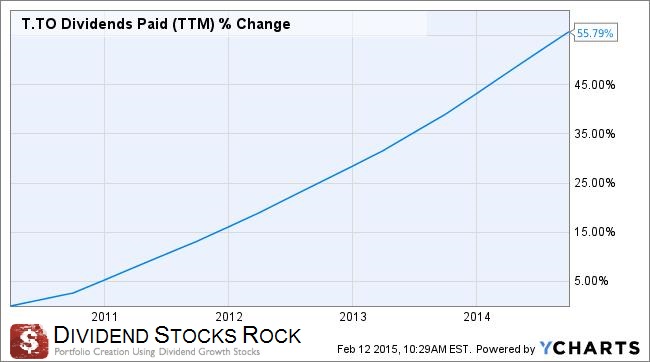

In term of dividend growth, Telus is hard to beat over the past few years. Management aims at a 10% dividend growth rate since 2011. They intend to increase their dividend twice a year which is, once again, above the average on the market. They want to achieve this growth by maintaining a payout ratio in the range of 65%-75%. So far, Telus has kept its promises:

As both revenues and earnings are going up at about the same pace, Telus should be in a good position to continue according to plan until 2016. No dividend growth rate indications are shared with investors after this period. We can assume the growth rate will continue but maybe not at this pace.

Principle #3: A Dividend Payment Today is Good, A Dividend Guaranteed For the Next 10 Years is Better

I think it’s very important to cross the payout ratio with the dividends paid over at least 5 years to see where the company is going with its dividend policy. It’s a key indicator to know if the payout will continue to increase or if it will reach a plateau at one point in time.

Telus’ payout ratio went from 40% to 65% within three years. However, while the dividend payout has never stopped increasing, the payout ratio is now stable between 60% and 66%. This is in line with management’s target and shows earnings started to increase faster than the dividend. With a strong client base, we can expect Telus to keep generating sufficient cash flow for years to come.

Principle #4: The Foundation of Dividend Growth Stocks Lies in its Business Model

A company that doesn’t have a sound business model won’t be able to sustain consecutive dividend increases over the long haul. On the other hand, businesses which pay dividends and increase them will outperform other stocks:

Source: Edward D. Jones – Dividend Stocks Rock

Now how can you find these marvels? This is why you need other financial metrics to identify companies that will be able to sustain and increase their dividend for the next 10 years. At DSR, we look at the 3 and 5 year metrics for Sales and Earnings per Share (EPS) growth. We only select companies showing positive growth over both the 3 and 5 year periods. Since an economic cycle lasts between 5 and 8 years, a strong company should be able to post increasing sales and earnings over these periods. I’m using both EPS and Revenue data from Ycharts:

DSR STOCK METRICS

3 year revenues = 5.00% Pass

5 year revenues = 3.27% Pass

3 year EPS growth = 7.13% Pass

5 year EPS growth = 2.75% Pass

Telus shows a perfect score with a 4 on 4 test score. The earnings growth over the past 3 years is also in line with the most recent numbers (EPS growth of 8.5%). This leads me to think the company will continue to benefit from its high profitability per client competitive advantage for the future.

Is Telus’ Growth Done Yet? Should you buy more or sell and smile?

So far, I’ve painted a pretty pink portrait of this company. I actually think Telus is still a good investment right now for both Canadians and Americans investors (the stock trades under TU on NYSE).

On the other hand, we know the Canadian Government is insisting on increasing the number of competitors in the mobile business. Right now, Telus (T.TO), Bell (BCE.TO), and Rogers (RCI.B.TO) are almost alone to share the market. The Govt thinks it will better for customers if bigger players (such as Verizon a few years) enter the market and “democratilize” prices. If this ever happens, Telus’ growth perspective will fall to zero for a while… Also, the Canadian market comes close to saturation; therefore, there are not many new customers to acquire if it’s not from the competition. This usually leads to lower margin and a difficult clientele acquisition process.

Overall, the company doesn’t trade at a super high PE ratio (19) and shows great growth perspective for the future. While there are always a few clouds over the mobile industry in Canada, I think Telus is still a good company to add to any dividend growth investor’s portfolio.

Disclaimer: I hold personally T.TO shares at the moment of writing this article. Also, T.TO is held in some Dividend Stocks Rock Portfolios.