I’ve been thinking about it for a while, but now my mind is made up; I’m selling my shares of Wal-Mart (WMT). This is not a decision to be taken lightly. After all, Wal-Mart has continuously shown a strong dividend payment profile with 41 consecutive years with a dividend increase.

Wal-Mart is present all over the world, it is the leader in the goods store industry, it has built a model generating continuous free cash flow and it has built a solid base of customers coming back week after week. Even their dividend policy is flawless:

Source: ycharts

While the dividend payment never ceased increasing, both payout and cash payout ratio has remained under very low standard. WMT definitely have lots of room to continue increasing their dividend payment for several years. Unfortunately, this is where the great story ends.

When I purchased shares of a company, I based my analysis on the 7 dividend investing principles. These principles have been elaborated based on academic studies and provide a strong guideline as not only to which company to buy, but at what price and when it is the right time to sell them. I systematically follow each of my holdings and make sure they continue to meet the 7 investing principles. Most importantly, I review my investment thesis year after year to make sure management is following the path to growth. Because if there isn’t growth, sooner or later the dividend payment will pale. Speaking of which, the lack of growth factors for Wal-Mart is probably its biggest weakness at the moment.

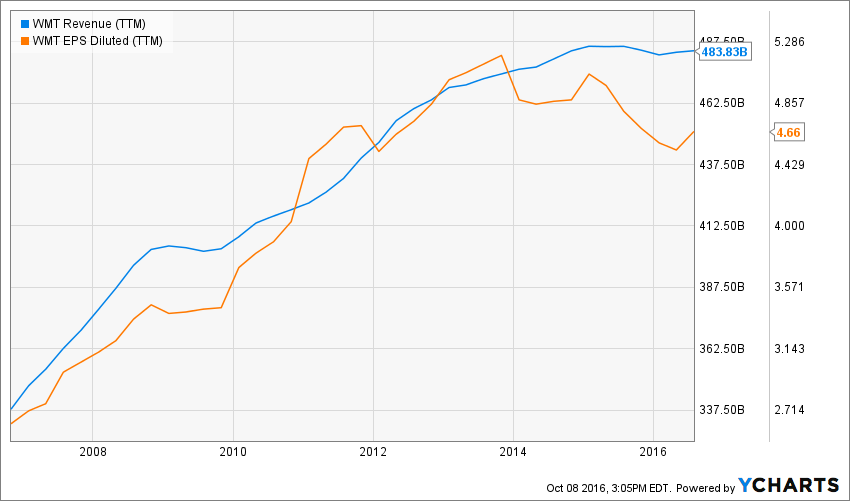

Stagnating Revenues & Struggling EPS

Since 2013, Wal-Mart hasn’t been a growing company by much:

Source: Ycharts

A 2-3 years revenue stagnation is nothing for a giant like Wal-Mart. In fact, it happens all the time as the economy slows down for a while or other factors such as a very strong USD will hurt temporarily profitability. However, when you start to think further and ask yourself why Wal-Mart is having a hard time to show growth, this is where it starts to get ugly.

Not so long ago, management announced another year of stagnation in 2018 compared to 2017 expectations. Last year, management also announced the closing of underperforming stores and the opening of new ones that should perform better. Such news tells use one thing; the fact is traditional stores can’t grow anymore. The game has gone online and Wal-Mart isn’t a leader in this playground… far from it.

According to The Economist, WMT internet sales in 2015 were only $12 billion compared to $100.5 billion for Amazon (AMZN). While The Economist Report highlighted that Wal-Mart is a more interesting investment than Amazon, I respectfully disagree with their thesis. I actually think that WMT will have to invest lots of money in its ecommerce platform to simply compete with Amazon while the latest will continue to look forward and innovate. In the online business, the second in line is never growing as fast as the first. The reason being is quite simple: while the second tries to imitate the leader in its business model, the leader is already working on the evolution of its model.

Wal-Mart is Late to the Online Game and This Means Massive Cash Flow Exiting Their Pocket

Management has long time thought that the world will always need brick & mortar stores. I can’t argue with this premise. There will always be people going to a store to buy their goods. However, this category of people isn’t growing. Each year, we have more internet customers preferring to buy their gifts online and avoid spending their time and energy going into stores, finding parking and rushing through traffic to get back home.

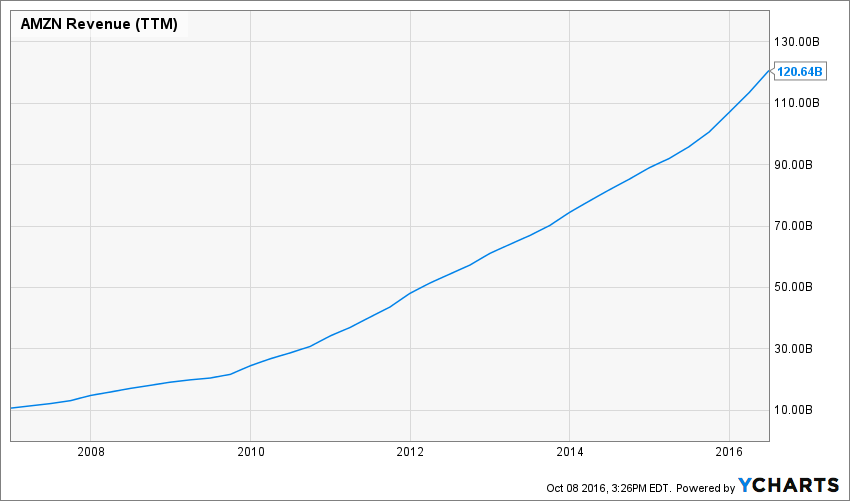

WMT has renewed their focus towards its eCommerce business lately but they couldn’t keep up. For this reason, they have spent 3.3 billion in buying Jet.com, a direct competitor to Amazon. While Jet.com has created great hype recently as it offers a similar system than Amazon but at a cheaper price, investors tend to forget that Amazon’s sales growth didn’t slow by a penny after the apparition of Jet.com:

Source: Ycharts

If you want to make it more obvious versus Wal-Mart, here’s both normalized (%) growth over the past 10 years:

Source: Ycharts

I’m afraid Wal-Mart will have to spend lots of its cash flow to build an eCommerce platform able to compete with Amazon. During this time, Amazon will continue to look forward and work on the evolution of its business model to remain the leader in the online shopping experience. In the meantime, Jet.com’s low margin business model will also hurt WMT margins.

WMT or AMZN?

Well, this is the question everybody asks when you discuss both companies. My point is not to say that Amazon is a buy and Wal-Mart is a sell. In fact, I have little interest in Amazon as a dividend growth investor. Their business model doesn’t leave room for any dividend payment as they continue to focus on growing their customer base. However, I can clearly see that the only interesting growth vector for Wal-Mart is the online business and that they will be hurt by another giant who knows the game a lot better.

For this reason, I’m selling WMT and I’m not buying AMZN.